|

|

|

|

|||||

|

|

|

OppFi Inc. OPFI shares have skyrocketed 104.2% in a year. This remarkable growth exceeds the 5.8% rise of its industry and the 18.1% rally of the Zacks S&P 500 Composite.

However, the recent performance paints a different picture. OPFI shares have declined 3% over the past month compared with the industry’s 6.6% fall and against the Zacks S&P 500 Composite 3.6% rise. It highlights that the stock is going through a correction phase.

OPFI’s price rise over the past year may be appealing to investors. However, making a hasty move may end up in losses. Whether investors should buy, hold or sell the stock should be addressed first. Let us delve deeper to find out the appropriate move to be made.

OppFi targets the underbanked population facing challenges of securing credit from traditional banks. OPFI has deployed AI and machine learning (ML)-based models to scrutinize the credit profile of customers, allowing the company to serve them swiftly.

In the second quarter of 2025, the company witnessed the loan auto approval rate to be 80%, increasing from the year-ago quarter’s 76%. A Net Promoter Score of 79 reflects strong customer satisfaction, highlighting OPFI’s successful customer-centric strategy.

OPFI’s ability to serve the subprime or the non-prime customer depends on its risk-mitigation strategy. Over the past few quarters, the company’s Net Charge-Off (NCO) rate has dropped. In the fourth quarter of 2024, NCO was 42%, a decline of 400 basis points (bps) from the year-ago quarter. Similarly, the metric declined by 700 bps in the March-end quarter of this year and 300 bps during the recently reported quarter.

This trend highlights the company’s robust credit risk management strategy, essential for catering to the rising demand of customers while minimizing the risks of credit default.

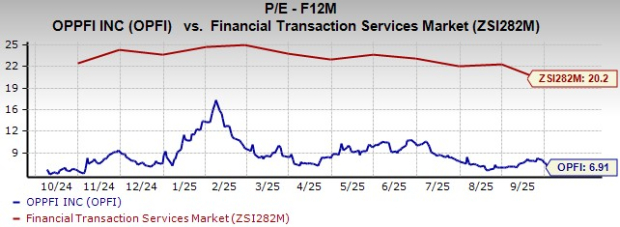

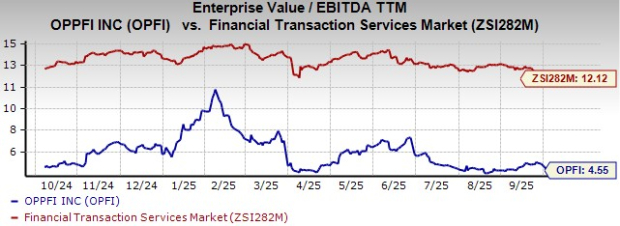

OppFi’s is priced at 6.91 times forward 12-month earnings per share, significantly lower than the industry’s average of 20.2 times. The stock looks fairly discounted in terms of the trailing 12-month EV-to-EBITDA ratio, with OPFI trading at 4.55 times, below the industry’s average of 12.12 times. At this valuation, OppFi appears to be a stock that has growth potential, thus attracting investors.

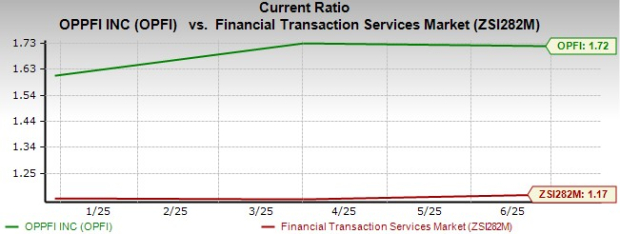

In terms of liquidity, OppFi’s current ratio in the second quarter of 2025 was 1.72, improving from the year-ago quarter’s 1.57, facilitated by an increase in accounts receivable. It is also impressive that OPFI’s current ratio beats the industry average of 1.17. We expect the company to cover its short-term obligations efficiently as the metric exceeds 1.

The Zacks Consensus Estimate for OPFI’s 2025 revenues is $588.9 million, hinting at 12% year-over-year growth. For 2026, the top line is expected to rise 7%. The consensus estimate for OPFI’s 2025 earnings per share stands at $1.42, implying 49.5% year-over-year growth. For 2026, the estimate is pinned at 4.2% growth.

OppFi’s core business model revolves around lending to subprime borrowers, drawing on the inherent risks of credit default. Per Experian, 28% of consumers with credit scores within 580-669 are likely to become seriously delinquent in the future. Since the company caters to individuals with scores even below the aforementioned range, the risk of credit default is particularly pronounced.

The fintech market is fiercely competitive, and in the case of OPFI, threats are felt from companies like SoFi SOFI and Dave DAVE.

Dave’s low-cost model can attract customers away from OppFi’s higher-interest products. DAVE’s subscription-based model enables it to expand its user base rapidly, growing its market share faster than OPFI.

Then again, SoFi, which is a much larger and diversified company, can continue to move down the credit spectrum. If SoFi starts to provide lower-cost banking services to the underserved, OPFI will lose a significant chunk of its market share due to the customer reliability SoFi enjoys from securing a national bank charter in 2022.

OPFI’s customer-centric strategy focuses on providing fast-paced services relying on AI and ML to reduce its credit risk. In doing so, the company succeeds in catering to the rising demand of customers while managing risks. By assessing valuation metrics, we have found OppFi to be at a discount compared with its industry, making it a particularly appealing stock.

On the liquidity front, a current ratio exceeding 1 ensures effective short-term debt coverage capabilities. Strong top and bottom-line prospects raise our optimism over this stock.

Having said that, we cannot ignore the fact that, having served sub-prime or non-prime customers, the company draws in substantial credit risks. In addition to that, rising competition within the fintech market is concerning.

Looking at the stock’s recent performance, we can conclude that OPFI has been riding through a correction phase. Hence, we recommend investors adopt a cautious approach and refrain from adding this stock to their portfolio now. Potential buyers are urged to hold off on investing and watch for further share price adjustments before buying.

OPFI has a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-02 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite