|

|

|

|

|||||

|

|

|

Kenvue's business lacks some of the advantages pharmaceutical companies enjoy.

The consumer health leader's business and financial results don't look strong right now.

Despite its Dividend King status, Kenvue isn't an attractive income stock to buy.

In today's uncertain economic environment, investing in robust dividend stocks can be a great hedge. Companies that can consistently issue growing payouts tend to have strong underlying businesses capable of surviving economic conditions that keep changing. It's even better to scoop up shares of companies that fit that profile while they trade at a significant discount.

Take Kenvue (NYSE: KVUE), for example. It's a relatively new company, but it also happens to claim title to being a Dividend King -- companies that have raised their dividend payouts annually for at least 50 consecutive years. The company has encountered some adversity, and as a result, Kenvue's shares have dipped 25% this year.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Can the stock bounce back? Let's dig deeper into what's going on with this healthcare specialist to figure out whether it is one of those reliable dividend payers investors want to own in times like these.

Kenvue became a publicly traded company in August 2023, when it was spun off from its parent company, Johnson & Johnson (NYSE: JNJ). Its former ties to J&J are what give it Dividend King status.

The split brought with it important implications for Kenvue's prospects. Kenvue is no longer in the business of developing novel pharmaceutical products like its former parent entity. Instead, it took over management of most of the well-branded over-the-counter (OTC) health products across several categories, including self-care, skin and beauty, and essential health. This includes brands like Tylenol, Motrin, Zyrtec, Benadryl, Neutragena, Band-Aid, Listerine, Visine, and Aveeno.

While pharmaceutical drugs often benefit from significant pricing power due to years of strong patent exclusivity, Kenvue's OTC items face a highly competitive environment with plenty of competitors, which limits the company's pricing power. Furthermore, many of Kenvue's products don't treat severe or life-threatening illnesses in the same manner as some of Johnson & Johnson's approved pharma therapies.

Even when Kenvue's products like Tylenol treat conditions that can disrupt people's day-to-day lives, there are, once again, plenty of generic alternatives that tend to be cheaper. Its big advantage is that many of Kenvue's brands are well-known and respected household names.

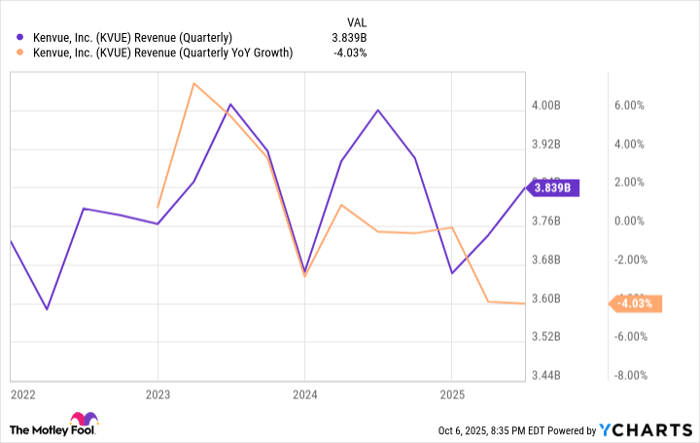

But this appeal alone hasn't helped the company improve its financial results. In the second quarter, Kenvue's net sales declined by 4% year over year to $3.8 billion. The company's adjusted earnings per share came in at $0.29, lower than the $0.32 reported in the prior-year quarter. Importantly, all three of Kenvue's business segments reported declining sales during the period.

It's worth pointing out why Johnson & Johnson decided to split with Kenvue in the first place. The pharmaceutical giant's consumer health division (which eventually became Kenvue) was posting slow and inconsistent revenue growth (at best) and was not performing as well as the rest of the business. Kenvue has not managed to reverse that trend since going public.

Data by YCharts.

The company is working through some other issues as well. It had a change in leadership when its CEO, Thibaut Mongon, stepped down in July. Kenvue appointed Kirk Perry, a member of its board of directors, as interim CEO. While Perry does have significant experience in the consumer-packaged goods field, Kenvue is still seeking a permanent CEO. The move was part of Kenvue's "broad strategic review," aimed at boosting growth and improving the company's performance.

These efforts are ongoing and under the purview of Kenvue's Strategic Review Committee. The company is also looking to decrease its expenses. Last year, the healthcare specialist reduced its workforce by 4% in an effort to achieve $350 million in cost savings by 2026, which could help boost the bottom line. That's all well and good, but while Kenvue's efforts might eventually bear fruit, it's hard to bet on that right now given the state of its business.

Finally, the Health and Human Services arm of the Trump administration last month came out and publicly alleged that Tylenol was linked to increased autism in children (an allegation that has been strongly disputed by healthcare advocates and the company itself). How much effect this will have on sales is yet to be seen. Roughly half of the stock's 13% price drop in the past month is likely attributable to the announcement.

Kenvue's prospects look far too uncertain right now. So, even though it is a Dividend King thanks to its legacy as a former division of Johnson & Johnson, Kenvue's underlying operations don't look like the sturdy, reliable kind that dividend investors typically want and which many Dividend Kings possess. The dividend payout ratio is currently at 112% based on earnings (and 97% based on free cash flow). That high a rate can be managed over short timeframes, but is not sustainable for more than a couple of quarters. A ratio closer to 50%-70% is sustainable and indicates a healthy dividend.

Those investors in the market for excellent dividend-paying income stocks might want to instead opt for Kenvue's former parent entity, Johnson & Johnson.

Before you buy stock in Kenvue, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Kenvue wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $654,835!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,159,218!*

Now, it’s worth noting Stock Advisor’s total average return is 1,081% — a market-crushing outperformance compared to 192% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of October 7, 2025

Prosper Junior Bakiny has positions in Johnson & Johnson. The Motley Fool has positions in and recommends Kenvue. The Motley Fool recommends Johnson & Johnson and recommends the following options: long January 2026 $13 calls on Kenvue. The Motley Fool has a disclosure policy.

| 10 hours | |

| Feb-15 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite