|

|

|

|

|||||

|

|

|

Palo Alto Networks operates three cybersecurity platforms that combine to protect its clients' entire enterprises.

It is weaving artificial intelligence (AI) into its products to automate workflows and ease the burden on human cybersecurity managers.

The stock trades today at a steep discount to one of its key rivals.

Two years ago, the world's largest cybersecurity company, Palo Alto Networks (NASDAQ: PANW), warned that 93% of organizations were unprepared to deal with the growing volume of modern digital threats, because their security operations still relied on human-led processes. As a result, 23% of cybersecurity alerts were slipping through the cracks, creating unacceptable vulnerabilities.

Since then, Palo Alto has launched a series of new cybersecurity products powered by artificial intelligence (AI) that help organizations automate everything from threat detection to incident response. Management believes these products will contribute to a substantial long-term growth phase for the company.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Palo Alto is trading near a record high, but investors can still scoop up a single share for under $220 (at the time of this writing). Here's why it might be a great long-term buy.

Image source: Getty Images.

Palo Alto operates three cybersecurity platforms: cloud security, network security, and security operations. These combine to protect its customers' enterprises from top to bottom. Through these platforms, it offers dozens of individual products that increasingly use AI to deliver the most advanced protection.

The Cortex XSIAM solution, for example, uses AI to automate the security operations center, which reduces an organization's reliance on inefficient human-led processes. By autonomously neutralizing threats, XSIAM reduces the number of incidents requiring a human investigation by 75%, which in turn lowers the probability of a successful breach.

But the company is also protecting the growing number of businesses that are using AI in their day-to-day operations. Many of them are plugging their sensitive internal data into AI models from third-party developers like OpenAI, which creates a new attack surface for hackers to exploit. Palo Alto's new AI Access Security platform gives managers full visibility over how, where, and why AI software is being deployed across the enterprise, so they can quickly identify vulnerabilities.

AI Access Security has also assessed the safety of over 4,000 AI software applications available in the market today, and it allows cybersecurity managers to turn off specific applications with the click of a button if they are deemed too risky.

Palo Alto generated $2.5 billion in revenue during its fiscal 2025 fourth quarter, which ended July 30. That was a 16% increase from the prior-year period, and it was the second consecutive quarter in which its growth rate accelerated -- a reflection of the company's momentum.

That strong result was driven by Palo Alto's next-generation security segment, which is home to many of the company's innovative new AI products. Its annual recurring revenue (ARR) soared by 32% during its fiscal Q4 to a record high of $5.6 billion.

For the last couple of years, Palo Alto has been incentivizing a growing number of its customers to abandon other cybersecurity vendors and consolidate onto its three platforms instead. Among the customers that have done so, its churn rate is almost zero: Once clients fully commit to Palo Alto for their cybersecurity needs, they tend to stick around. Plus, these "fully platformed" customers had a net revenue retention rate of 120% during the fiscal fourth quarter, meaning they were spending 20% more money with Palo Alto than they had in the prior-year period.

For those reasons, Palo Alto believes "platformization" will help drive its next-generation security ARR to $15 billion by fiscal 2030. That would be a staggering 167% increase from its current level.

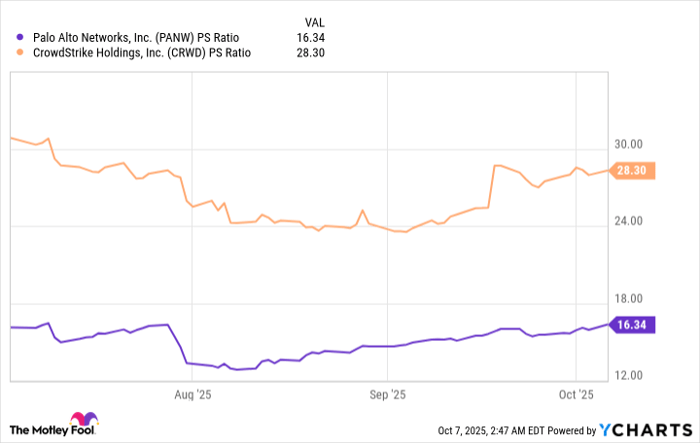

Palo Alto stock is trading at a price-to-sales (P/S) ratio of 16.3 as I write this, which is a 42% discount to the valuation of its chief rival in the AI cybersecurity space, CrowdStrike:

PANW PS Ratio data by YCharts.

CrowdStrike is growing slightly faster than Palo Alto -- its revenue grew by 21% during its most recent quarter. From that perspective, CrowdStrike's valuation might deserve a slight premium relative to Palo Alto. However, I would argue the valuation gap is far too wide considering Palo Alto's next-generation security ARR alone is greater than CrowdStrike's total ARR -- not to mention, it grew by a whopping 32% in the fiscal fourth quarter.

Palo Alto is also thinking several steps ahead of its competitors. In August, it launched a new product called PAN-OS 12.1 Orion that will help enterprises prepare for the quantum computing revolution. Eventually, these powerful new computing systems will make existing encryption methods obsolete, leaving businesses exposed to cyber threats. Palo Alto has an opportunity to build a massive head start over other cybersecurity vendors in this emerging market.

As a result, Palo Alto stock could be a great buy right now for long-term investors.

Before you buy stock in Palo Alto Networks, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palo Alto Networks wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $654,835!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,159,218!*

Now, it’s worth noting Stock Advisor’s total average return is 1,081% — a market-crushing outperformance compared to 192% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of October 7, 2025

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CrowdStrike. The Motley Fool recommends Palo Alto Networks. The Motley Fool has a disclosure policy.

| 7 hours | |

| 8 hours | |

| 10 hours | |

| 12 hours | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite