|

|

|

|

|||||

|

|

|

Major cloud computing companies are sitting on huge revenue backlogs as customers are rushing to train and deploy AI models using their infrastructure.

This has led to a sharp increase in the demand for AI servers.

Healthy double-digit earnings growth combined with an attractive valuation suggests that this underrated name could become a multibagger.

The demand for artificial intelligence (AI) compute infrastructure has been growing at a breathtaking pace as organizations and governments across the world are looking to build, customize, train, and deploy AI models to enhance productivity.

According to PwC, industries with higher exposure to AI are witnessing a 3x increase in revenue per employee as compared to industries with the least exposure. A whopping $6.7 trillion is expected to be spent on data centers through 2030, with three-fourths of that going toward AI-capable data centers, according to McKinsey.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Not surprisingly, companies are getting their hands on whatever AI computing capacity is available. This has led to a remarkable increase in the growth rates and revenue backlogs of cloud infrastructure providers such as Oracle, CoreWeave, Amazon, and Microsoft. These companies are spending big money to set up more AI data centers.

There are multiple ways investors can capitalize on the lucrative AI infrastructure opportunity. However, there's one company that's right in the middle of this boom but hasn't received much love on the stock market. Let's take a closer look at that name and see why it has the potential to become a multibagger.

Image source: Getty Images.

Dell Technologies (NYSE: DELL) is famous for its personal computers, workstations, and peripherals, but the company is also in the business of cloud computing infrastructure. Specifically, Dell's infrastructure solutions group (ISG) segment includes sales of storage, server, and networking equipment deployed in data centers.

This business has been gaining impressive traction thanks to the rapidly growing demand for AI servers. Dell's ISG revenue segment jumped by an impressive 30% year over year in the first six months of fiscal 2026 (ended on Aug. 1) to $27.1 billion. Sales of servers and networking equipment accounted for 71% of ISG revenue in the first half of FY26, with revenue increasing by 47% from the year-ago period.

At this pace, Dell's revenue from servers and networking equipment would hit $40 billion in the ongoing fiscal year (considering that it generated $20 billion from this segment in the first half). That would translate into a 48% increase from the previous year. However, there is a good chance that Dell could end up doing better than that.

That's because the orders for Dell's AI servers are flowing in at a healthy clip. The company has shipped more AI servers in the first half of fiscal 2026 than in the entirety of fiscal 2025. It received $5.6 billion worth of new AI server orders last quarter, which brought its AI server order backlog to $11.7 billion.

The company is now confident in selling more than $20 billion worth of AI servers in the current year, which would be more than double the revenue it generated from this segment last year. Dell management's belief in the health of its AI server business can be attributed to the expansion of its customer base, as well as the hunger for AI servers capable of running powerful chips.

For instance, Dell is now shipping server racks capable of running Nvidia's top-of-the-line AI chip systems to CoreWeave. Looking ahead, Dell's partnership with CoreWeave could turn out to be a major tailwind as CoreWeave has been winning new contracts for its AI compute capacity at a terrific pace.

CoreWeave had a revenue backlog of more than $30 billion at the end of Q2, up by 86% from the year-ago period. It has recently won multibillion-dollar contracts from OpenAI, Meta Platforms, and Nvidia, which have taken its AI revenue backlog well past the $50 billion mark. This should encourage CoreWeave to invest in more AI capacity, which is exactly what the company has been doing.

In all, sales of servers equipped with AI accelerators are forecast to jump from $144 billion last year to $427 billion next year. That would translate into a compound annual growth rate of 24%. Dell is growing at a faster pace than the market right now, suggesting that its share of this space is improving. So Dell's revenue can get a massive long-term boost thanks to the huge opportunity in AI servers, and that could send its shares flying.

Though Dell's AI business has been growing at a nice clip and the company has an additional AI-related opportunity in the form of generative AI PCs, it trades at just 21 times earnings. That's quite cheap considering that it reported a healthy year-over-year increase of 18% in its adjusted earnings in the first half of the year to $3.86 per share.

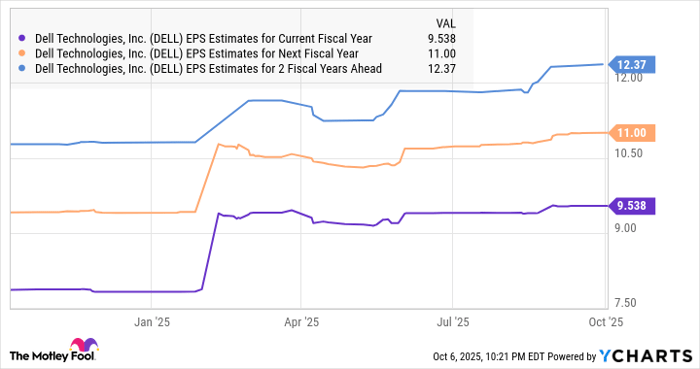

Analysts are projecting Dell's double-digit earnings growth to continue over the next couple of years as well, though don't be surprised to see it outpace their expectations.

DELL EPS Estimates for Current Fiscal Year data by YCharts

Assuming Dell manages to hit Wall Street's expectations of $12.37 per share in earnings after a couple of years and trades at 27 times earnings at that time (in line with the tech-heavy Nasdaq-100 index's forward earnings multiple), its stock price could hit $334. That would be almost 2.3 times Dell's current stock price, though there is a good chance that it could become a bigger multibagger on account of potentially faster earnings growth, which could lead the market to reward it with a premium valuation.

Before you buy stock in Dell Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Dell Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $663,905!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,180,428!*

Now, it’s worth noting Stock Advisor’s total average return is 1,091% — a market-crushing outperformance compared to 192% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of October 7, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Meta Platforms, Microsoft, Nvidia, and Oracle. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 |

A Memory-Chip Shortage Is Squeezing Consumer Techand Its Set to Get Worse

DELL -9.13%

The Wall Street Journal

|

| Feb-12 |

Cisco Memory Chip Warning Sends Down Dell, HPE, Arista, NetApp Shares

DELL -9.13%

Investor's Business Daily

|

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Cisco Profit Margin Outlook Sends Down Dell, HPE, Arista, NetApp Shares

DELL -9.13%

Investor's Business Daily

|

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite