|

|

|

|

|||||

|

|

|

Shake Shack Inc. SHAK continues to benefit from its strategic initiatives, menu innovation and global store expansion, all while maintaining a strong focus on enhancing profitability. The company remains optimistic about its licensing segment, supported by robust global partner relationships and ample growth opportunities. Furthermore, Shake Shack is investing in data and guest recognition tools to deliver more personalized marketing strategies, aiming to boost customer engagement and traffic growth.

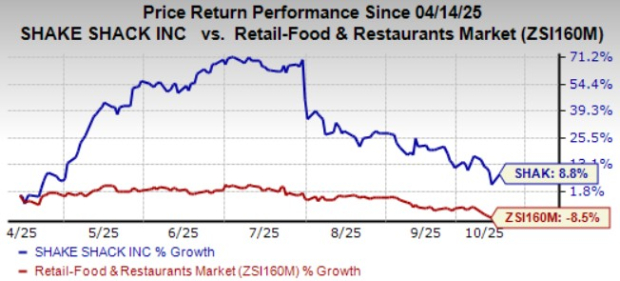

Shares of this Zacks Rank #3 (Hold) fast food hamburger restaurant chain have risen 8.8% over the past six months, outperforming the Zacks Retail - Restaurants industry’s 8.5% decline. Its earnings per share (EPS) topped the Zacks Consensus Estimate in three of the trailing four quarters, missing on only one occasion, the average surprise being 8.9%.

Currently, SHAK’s fiscal 2025 EPS estimate has been revised downward to $1.38 from $1.40 over the past 60 days. While the company continues to face elevated costs and macroeconomic uncertainties, its ongoing expansion initiatives and 360-degree approach to marketing are expected to support long-term growth momentum.

Let’s delve deeper and see what may bring the stock back on track.

Brand Awareness: Shake Shack aims to drive sales growth while strengthening its brand image and customer loyalty. As one of the fastest-growing franchise networks in the United States, the company expanded into Canada, Israel and Malaysia in 2024. The second quarter marks 18 consecutive quarters of positive same-store sales growth, alongside year-over-year improvements in restaurant-level and adjusted EBITDA margins, and double-digit adjusted EBITDA growth. While the company continues to make strong progress, management remains focused on further differentiating Shake Shack from traditional fast-food chains and reinforcing its unique brand identity across global markets.

While the company has underinvested in advertising compared to larger peers, relying mainly on word-of-mouth and targeted marketing, it plans to enhance these efforts with broader advertising campaigns that bring the brand to life and maximize its growth potential.

Expansion Efforts & Licensing Partners: Shake Shack continues to advance its global growth strategy through robust new store openings and strategic licensing collaborations. During the second quarter of 2025, the company opened 13 new domestic company-operated Shacks, bringing the first-half total to 17. Shake Shack remains on track to open 45 to 50 company-operated Shacks in 2025, marking the largest development class in the company’s history.

The licensing segment also delivered a solid performance in the second quarter, with nine new openings and strong results across regions. Additionally, the company announced two new licensing partnerships, one with PENN Entertainment to open 10 licensed Shake Shack locations across U.S. casinos, and another with Grupo Attie, Multifood Enterprises to establish 12 Shacks in Panama, beginning with the first opening next year. Shake Shack has also expanded its reach by serving on Delta Air Lines flights across 13 domestic airports, receiving highly positive guest feedback.

Focus on Menu Innovation: Management emphasized that “culinary innovation is part of our DNA at Shake Shack.” The company takes great pride in offering fresh, high-quality food made with premium ingredients, ensuring an exceptional guest experience. Recent introductions such as the limited-time summer barbecue platform, the Dubai Chocolate Pistachio Shake and the new fried pickles side have generated strong buzz among new customers while also driving higher visit frequency.

Another key focus area has been the introduction of combo or bundled meal options, which the company views as essential for drive-thru success. Additionally, Shake Shack launched its first company-operated Shack featuring a full lineup of signature cocktails, including the Frozen Around the Rocks Patrón Shaquerita, along with boozy shakes, premium cocktails, spirits, beer and wine. Encouraged by strong customer feedback, management expects this initiative to serve as a long-term driver of sales mix and customer retention.

Paid Media & Marketing Push: For the first time, Shake Shack has expanded its marketing approach beyond traditional advertising methods. The company launched a paid media campaign highlighting two key initiatives, the Dubai Shake and the Dollar Soda promotion, which were aimed at boosting Shake Shack app adoption and engagement.

Developing this product-focused marketing capacity is a key component of the business' plan to promote steady, long-term traffic growth. Shake Shack hopes to increase sales by combining creative goods with focused marketing, which will increase operating leverage and restaurant margins.

Competitive Threat: The fast-casual dining sector in the United States is intensely competitive, with a wide variety of food chains offering convenient and readily accessible options. Maintaining a leading position in this landscape is increasingly challenging. While Shake Shack enjoys a strong presence in the Middle East, its global footprint remains relatively limited. Success in this market requires continuous digital innovation, personalized product offerings and the delivery of a seamless consumer experience. As a result, Shake Shack faces ongoing pressure to adapt its strategies in line with evolving consumer preferences. Despite significant investments in labor, real estate and operational enhancements, the brand continues to contend with formidable competition from other fast-casual players.

High Costs Hurt: Inflationary pressure is likely to hurt the company’s performance. Continued challenges with rising beef costs and general inflation are affecting cost structures. In the second quarter, food and paper costs rose to 28.2% of Shack sales, up 40 bps year over year, driven by mid-single-digit beef cost increases. Management expects beef inflation to continue into the low-to-mid single digits for 2025, with food & paper costs guided up low single digits.

Some better-ranked stocks from the Zacks Retail-Wholesale sector are Red Robin Gourmet Burgers, Inc. RRGB, Groupon, Inc. GRPN and Levi Strauss & Co. LEVI.

Red Robin Gourmet Burger presently sports a Zacks Rank #1 (Strong Buy). The company delivered a trailing four-quarter earnings surprise of 58.3%, on average. RRGB’s stock has jumped 23.8% year to date. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for RRGB’s 2025 sales indicates a 3% decline, while the estimate for EPS suggests 82% growth from the prior-year levels.

Groupon sports a Zacks Rank of 1 at present. The company delivered a trailing four-quarter earnings surprise of 230.5%, on average. Groupon's stock has surged 69.9% year to date.

The Zacks Consensus Estimate for Groupon’s 2025 sales and EPS indicates growth of 2.4% and 153%, respectively, from the prior-year levels.

Levi Strauss carries a Zacks Rank of 2 (Buy) at present. The company delivered a trailing four-quarter earnings surprise of 26.7%, on average. Levi Strauss stock has gained 25.3% year to date.

The Zacks Consensus Estimate for LEVI’s 2025 sales indicates a 3.4% decline, while the estimate for EPS suggests 4.8% growth from the prior-year levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-23 | |

| Jul-22 | |

| Jul-20 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-13 | |

| Jul-10 | |

| Jul-09 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite