|

|

|

|

|||||

|

|

|

What a time it’s been for Carlyle. In the past six months alone, the company’s stock price has increased by a massive 58.5%, reaching $58 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now still a good time to buy CG? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free for active Edge members.

Founded in 1987 with just $5 million in capital and named after the iconic New York hotel where the founders first met, The Carlyle Group (NASDAQ:CG) is a global investment firm that raises, manages, and deploys capital across private equity, credit, and investment solutions.

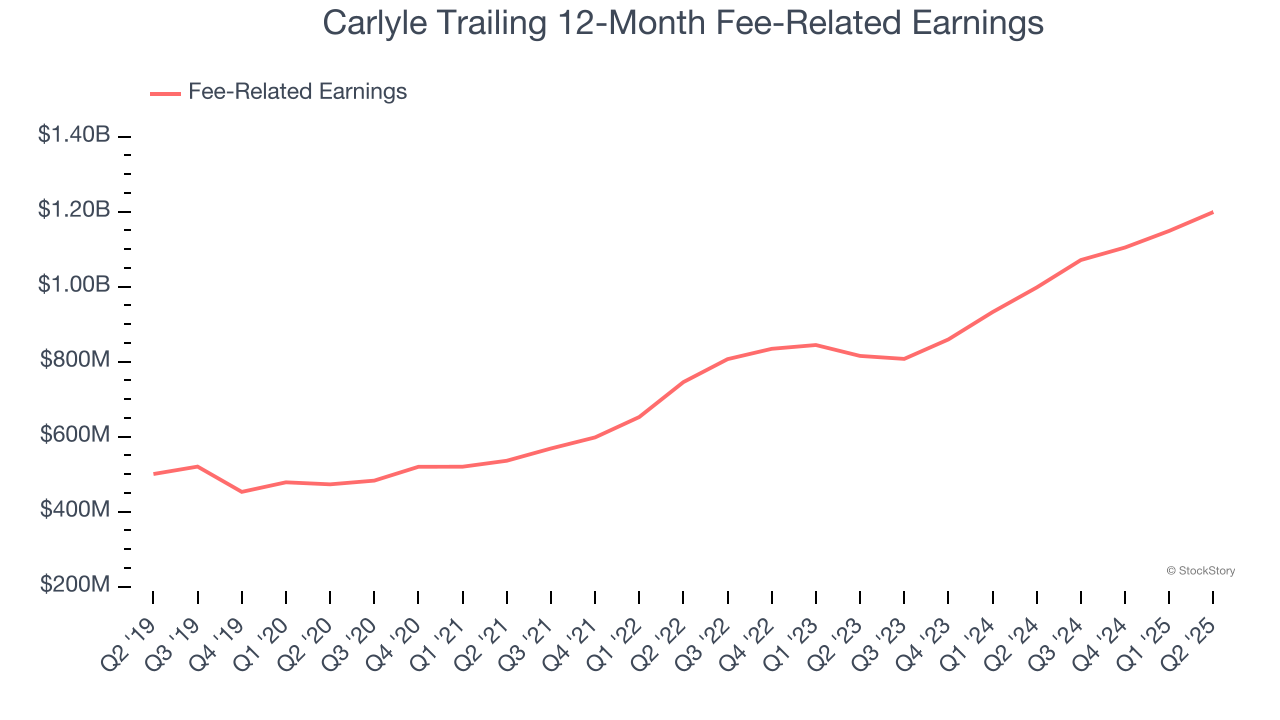

While revenue growth captures attention, the quality of that growth is what truly drives shareholder value. For asset management firms, fee-related earnings represent the stable, predictable profits from their core fee-based services, excluding the more unpredictable elements like performance fees and investment returns. This metric reveals the sustainable earnings power of the business.

Carlyle’s annual fee-related earnings growth over the last five years was 20.5%, a solid result.

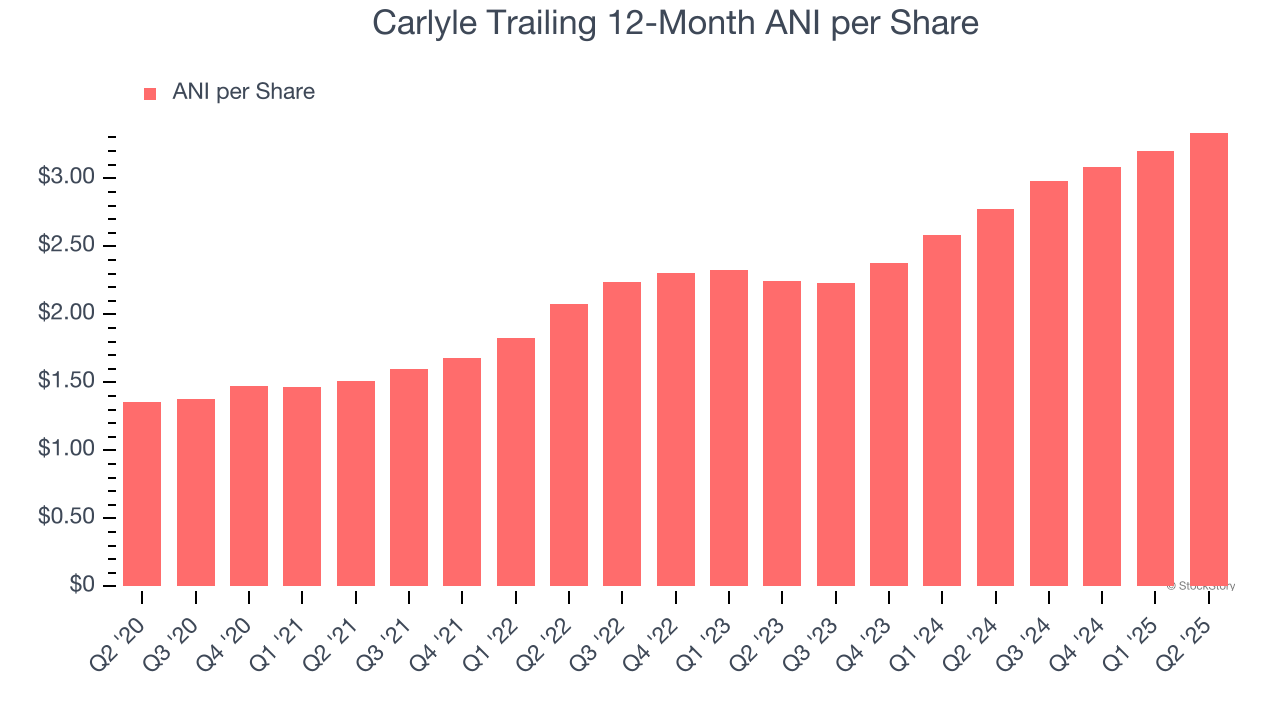

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Carlyle’s EPS grew at a remarkable 19.8% compounded annual growth rate over the last five years, higher than its 11.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

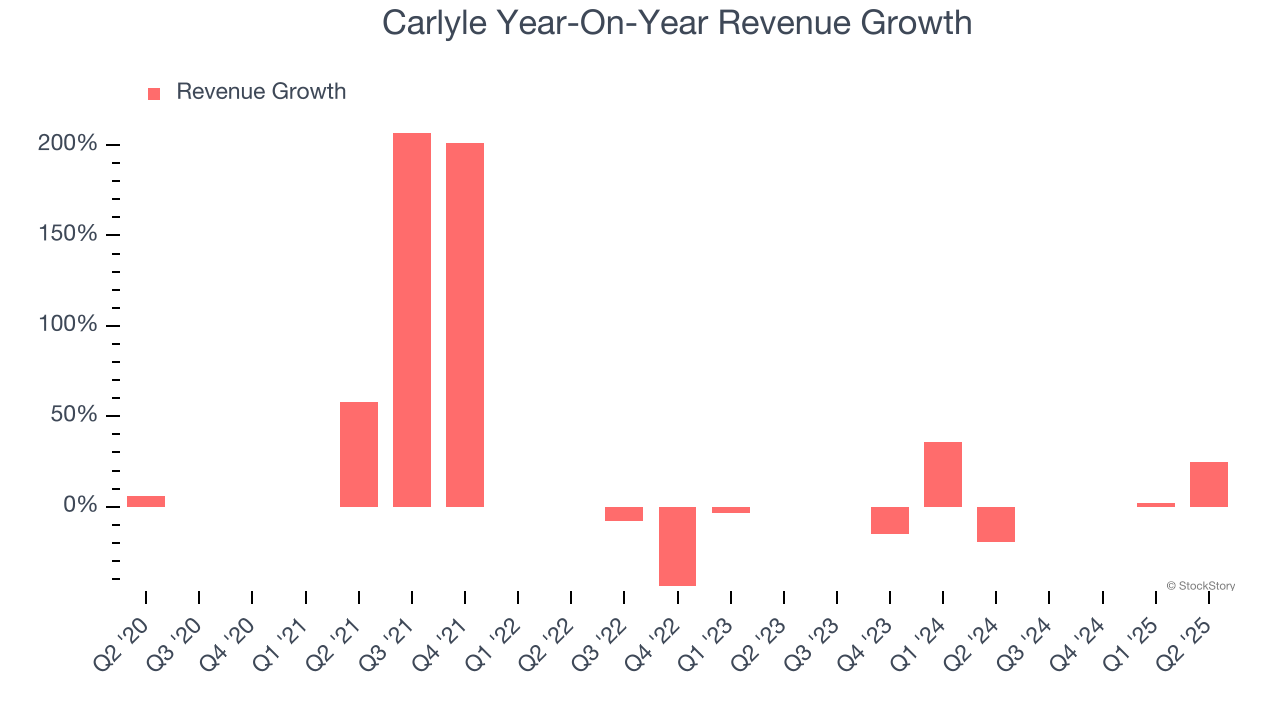

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Carlyle’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 3.9% over the last two years.

Carlyle’s positive characteristics outweigh the negatives, and after the recent rally, the stock trades at 13.3× forward P/E (or $58 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free for active Edge members .

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-26 | |

| Mar-23 | |

| Mar-20 | |

| Mar-20 | |

| Mar-17 | |

| Mar-11 | |

| Mar-06 | |

| Mar-04 | |

| Mar-03 | |

| Feb-28 | |

| Feb-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite