|

|

|

|

|||||

|

|

|

TSMC's growth trajectory so far in 2025 suggests that it is on track to exceed its guidance.

The company could deliver stronger-than-expected earnings growth thanks to its robust pricing power.

TSMC trades at an attractive valuation despite running up impressively in the past few months.

The world's largest semiconductor foundry, Taiwan Semiconductor Manufacturing (NYSE: TSM), fabricates chips for the leading chip designers across the globe. It also happens to be one of the hottest stocks on the market over the past six months.

Share prices of the company have shot up a remarkable 93% during this period. The stock's stunning rally is all set to get a major boost when it releases its third-quarter results on Oct. 16. Let's look at the reasons why this semiconductor stock can fly higher following its upcoming quarterly report.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: TSMC.

TSMC's growth has been outstanding in the past couple of years thanks to the artificial intelligence (AI) chip boom. The Taiwan-based company is the world's largest contract chipmaker with an estimated market share of 70%, according to market research firm TrendForce.

TSMC manufactures chips for not just AMD, Nvidia, and Broadcom, but also for the likes of Apple (NASDAQ: AAPL), Qualcomm, and MediaTek. This diverse customer base gives TSMC the ability to benefit from the booming demand for AI chips not just in data centers, but also in smartphones and computers. It is easy to see why TSMC's growth has been ahead of its projections so far this year.

The company recently reported its revenue for September, the last month of Q3. Its top line jumped by 31% from the year-ago period during the month, bringing its total quarterly revenue to $32.5 billion. That's slightly higher than the midpoint of its guidance range, and also more than what Wall Street was looking for.

The company's total revenue in the first nine months of the year has jumped by over 36%. This puts TSMC well on course to exceed its 2025 revenue guidance of 30%. Importantly, TSMC's earnings for the third quarter are likely to grow at a solid pace as well. That's because the company has reportedly increased the price of its popular 3-nanometer (nm) process node by around 20%.

Chips manufactured using a 3nm process node are in hot demand because of their deployment in smartphones. TSMC reported that 27% of its revenue came from the smartphone segment in the second quarter of 2025, and the 3nm process node accounted for 24% of its top line. Given that Apple is manufacturing its latest iPhone processors on TSMC's 3nm node, and its latest smartphones are seeing stronger-than-expected demand, TSMC is likely to benefit from a combination of higher volumes and pricing toward the end of the year.

According to Morgan Stanley, Apple may increase its iPhone production to more than 90 million units from the earlier build forecast of 84 million to 86 million units. Apple reportedly accounts for 20% of TSMC's top line, so a potential increase in iPhone production, as well as the reported increase in prices, could help the chipmaker issue better-than-expected guidance for Q4.

TSMC is going to further improve its chip manufacturing process in 2026 by moving to a 2nm node. By shrinking the size of its chips, TSMC will be able to pack in more computing power and reduce power consumption. Apple, Nvidia, AMD, and MediaTek are reportedly going to be the first customers of the company's 2nm chip node next year.

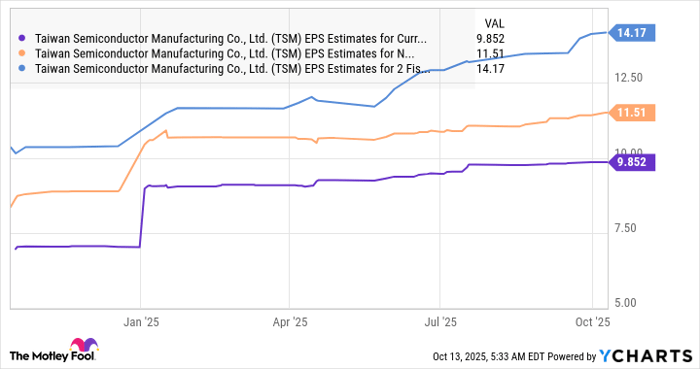

With the 2nm chips expected to carry a premium of 10% to 20% over the 3nm process node, don't be surprised to see TSMC's earnings growth to be faster than consensus estimates in 2026. The company is expected to clock a 40% increase in its bottom line this year. Analysts expect that growth rate to slow down to 17% in 2026.

However, the reported price increases of the existing 3nm process node, as well as the higher pricing of the next-generation 2nm process node, are the reasons why TSMC's earnings growth could be higher than expected. As such, its earnings expectations could likely move higher.

Data by YCharts.

TSMC's ability to continue outperforming expectations and maintain a healthy pace of growth, thanks to the AI-powered secular opportunity in the semiconductor market, should be a tailwind for this growth stock. That's why it would make sense to buy TSMC stock while it is trading at an attractive 25 times forward earnings.

It is currently trading at a nice discount to the tech-heavy Nasdaq-100 index's earnings multiple of 33 (using the index as a proxy for tech stocks). However, a solid set of results on Oct. 16 could send TSMC stock higher and inflate the valuation, so it may be a good idea to buy shares before that happens.

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $657,979!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,122,746!*

Now, it’s worth noting Stock Advisor’s total average return is 1,060% — a market-crushing outperformance compared to 187% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of October 13, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Nvidia, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 |

Apple To Hold Product Event On March 4. Cheaper iPhone Seen But No AI Siri

AAPL

Investor's Business Daily

|

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite