|

|

|

|

|||||

|

|

|

Last week, Tilray Brands TLRY reported its first-quarter results for fiscal 2026 (year ending May 2026). Both earnings and sales not only beat our expectations, but also increased from the year-ago quarter.

The Canada-based cannabis operator surprised investors by swinging back to profitability during the quarter. Tilray posted net income of $1.5 million, a significant turnaround to the year-ago period when it posted a loss of $34.7 million. The company’s top-line rose 5% year over year to $209.5 million, primarily driven by the encouraging performance of its cannabis business. The company’s cash flow also improved significantly during the quarter, underscoring its strong financial discipline.

However, long-term investors typically focus beyond a single quarter’s numbers and assess broader fundamentals. Let’s explore Tilray’s key strengths and challenges to better understand how to play the stock after its latest results.

While Tilray’s roots lie in cannabis, a saturated domestic market and uncertainty around U.S. federal legalization have encouraged the company to broaden its business base. Over the past few years, Tilray has diversified across beverages, distribution, and wellness, with these non-cannabis segments now contributing more than two-thirds of total revenues.

Tilray has steadily expanded its presence in the beverage space through multiple acquisitions — including brands from Anheuser-Busch and Molson Coors — establishing itself among the largest craft brewers in the United States. Despite SKU rationalization efforts under its Project 420 integration plan, beverage sales held steady at $60 million, underscoring the segment’s stability amid restructuring.

The distribution segment remained the largest contributor to overall revenues, growing 9% year over year to $74 million. This growth was driven by stronger demand across Tilray’s European and international logistics networks.

Looking ahead, we expect Tilray to reap the benefits of Project 420 in the second half of fiscal 2026. The company’s focus on enhancing its global supply chain and increasing cultivation footprint is likely to meet the growing demand across all marketed territories.

Tilray’s cannabis business spans both recreational and medical markets, and Q1 results indicate encouraging progress in both areas. Cannabis revenues rose 5% year over year to $64.5 million, supported by double-digit growth in Canadian adult-use and international medical cannabis sales.

In Canada, adult-use revenues climbed 12%, reaffirming Tilray’s position as the country’s largest legal cannabis producer by revenues. Meanwhile, international sales increased 10%, led by strong growth in Germany and Italy, where the company benefits from its CC Pharma distribution platform.

Tilray is also broadening its European presence and preparing for potential regulatory tailwinds amid renewed optimism surrounding U.S. cannabis reform. This international momentum could help offset domestic pricing pressure and bolster the company’s long-term growth trajectory.

Tilray continues to operate in a crowded field, facing cut-throat competition from Aurora Cannabis ACB, Canopy Growth CGC and Curaleaf Holdings CURLF. Each of these players is pursuing aggressive international expansion and cost-optimization efforts, making it difficult to sustain outsized market share gains.

As TLRY gains ground in international markets, competitive responses from Aurora, Canopy and Curaleaf are more than likely to intensify, particularly in Europe — a key growth region for all major players in the industry.

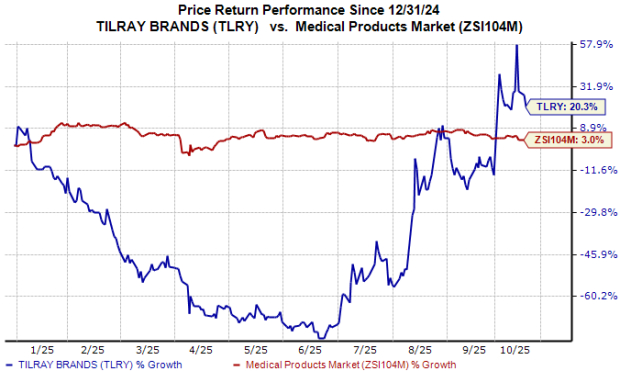

Shares of Tilray Brands have gained 20% year to date compared with the industry’s 3% growth, as seen in the chart below.

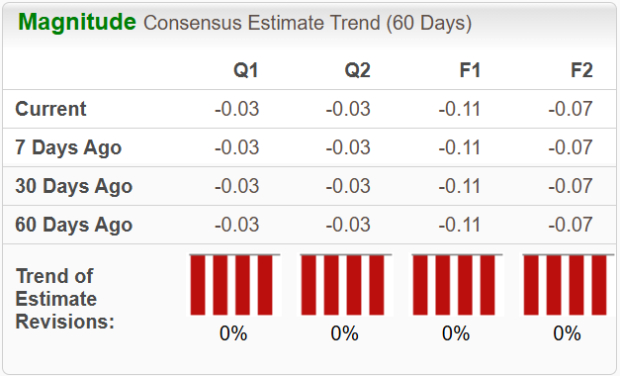

Estimates for TLRY’s loss per share for fiscal 2026 and 2027 have remained consistent in the last 30 days.

Tilray’s return to profitability, improved cash flow, and diversified revenue base signal a credible turnaround story. Its strategic expansion into craft beverages, distribution and THC-based wellness products provides resilience, while rising cannabis sales and expanding global reach offer renewed growth potential.

Although competitive pressures persist, Tilray’s leaner cost structure and stronger balance sheet give it an advantage over peers. With a Zacks Rank #2 (Buy), TLRY appears well-positioned to benefit from both improving operational efficiency and policy-driven optimism surrounding cannabis reform under the Trump administration.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 14 hours | |

| 15 hours | |

| 15 hours | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-15 | |

| Jul-15 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite