|

|

|

|

|||||

|

|

|

Novo Nordisk NVO and Omeros Corporation OMER have announced the signing of a definitive asset purchase and license agreement for zaltenibart (formerly OMS906), a clinical-stage candidate targeting rare blood and kidney disorders.

Under the agreement, Novo Nordisk will receive exclusive worldwide rights to develop and commercialize zaltenibart across all indications. Omeros will receive approximately $340 million in upfront and near-term milestone payments, with the total deal value reaching up to $2.1 billion, contingent on the achievement of certain development and commercial milestones. The agreement also includes tiered royalty payments to Omeros based on potential future net sales of the drug. Shares of OMER skyrocketed 154.2% on Wednesday following the news.

Zaltenibart is an investigational monoclonal antibody designed to inhibit MASP-3, a key upstream activator of the complement system’s alternative pathway and a critical component of innate immunity. Dysregulation of this pathway plays a critical role in several rare diseases, making MASP-3 an attractive therapeutic target. By acting at this early stage of the pathway, zaltenibart has the potential to offer significant advantages over existing treatments that target downstream components, such as C3 or C5.

Omeros has already reported encouraging phase II results for zaltenibart in paroxysmal nocturnal hemoglobinuria (PNH), a rare blood disorder characterized by immune-mediated destruction of red blood cells. The therapy has demonstrated strong efficacy, good tolerability and a favorable safety profile, differentiating it from other alternative pathway inhibitors currently in development or on the market.

Novo Nordisk plans to build on this clinical foundation by launching a global phase III program of zaltenibart to treat PNH. NVO also expects to later expand into additional rare blood and kidney disorders indications for this candidate, including immunoglobulin A nephropathy, C3 glomerulopathy and atypical hemolytic uremic syndrome, and other immune and complement-driven disorders. The company sees zaltenibart as a strategic fit to strengthen its leadership in the rare disease segment and drive long-term portfolio growth.

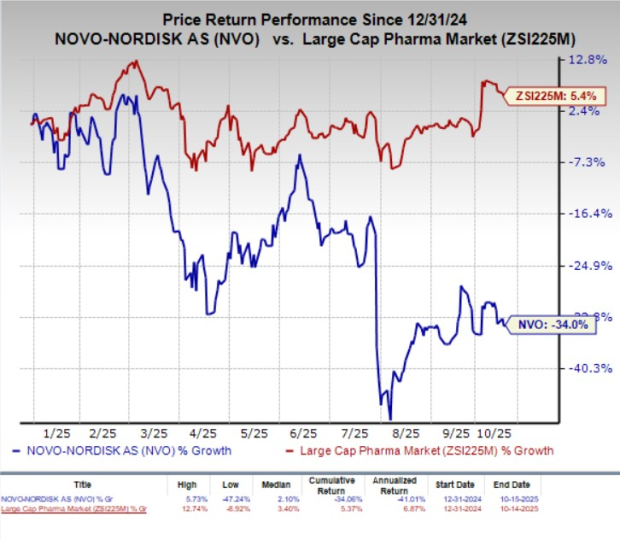

Year to date, NVO shares have plunged 34% against the industry’s 5.4% growth.

Through this deal, Omeros seeks to leverage NVO’s vast resources, global reach and extensive expertise in the rare disease segment to further advance its zaltenibart program. OMER will, however, retain rights to its preclinical MASP-3 programs outside zaltenibart, enabling further development of small-molecule MASP-3 inhibitors for select indications. The transaction remains subject to customary closing conditions, including regulatory approvals, and is expected to close in the fourth quarter of 2025.

If successfully developed and commercialized, zaltenibart could emerge as a differentiated, potentially best-in-class therapy for multiple complement-mediated disorders, offering a new treatment approach while preserving critical immune functions tied to vaccine responses and infection defense.

Novo Nordisk A/S price-consensus-chart | Novo Nordisk A/S Quote

Novo Nordisk has achieved tremendous commercial success with its blockbuster semaglutide (GLP-1) products, Wegovy (obesity) and Ozempic (diabetes). However, the company’s growth trajectory has suffered recently.

In July 2025, NVO revised its sales and profit outlook for the year, reflecting slower-than-expected uptake for Wegovy and Ozempic, due to intensifying competition from arch-rival Eli Lilly LLY and compounded semaglutide alternatives in its largest obesity market, the United States. Eli Lilly’s tirzepatide-based drugs, Mounjaro (diabetes) and Zepbound (obesity), have captured rapid demand and market share, pressuring NVO’s position in both obesity and diabetes markets. Despite being on the market for less than three years, both drugs have become LLY’s key top-line drivers. In the first half of 2025, they generated combined sales of $14.7 billion, accounting for 52% of Eli Lilly’s total revenues.

Several other companies, like Viking Therapeutics VKTX, are also making rapid progress in the development of GLP-1-based candidates in their clinical pipeline. Viking Therapeutics’ dual GIPR/GLP-1 RA, VK2735, is being developed both as oral and subcutaneous formulations for the treatment of obesity. In August 2025, VKTX announced mixed top-line results from a mid-stage study evaluating the safety and efficacy of the oral formulation of VK2735, which caused the stock to drop significantly. Phase III obesity studies with the subcutaneous formulation of VK2735 have also been initiated.

Given these challenges, Novo Nordisk has been working to lessen its reliance on GLP-1 drugs as its primary revenue driver through a diversified pipeline of rare disease treatment candidates. The latest asset purchase and license agreement with Omeros furthers this agenda.

Novo Nordisk currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite