|

|

|

|

|||||

|

|

|

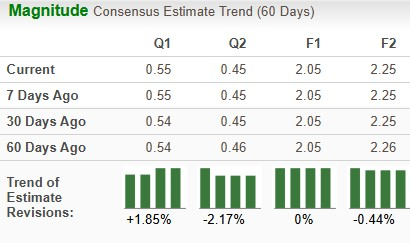

AT&T Inc. T is scheduled to report third-quarter 2025 earnings on Oct. 22, before the opening bell. The Zacks Consensus Estimate for revenues and earnings is pegged at $30.96 billion and 55 cents per share, respectively. The earnings estimate for AT&T for 2025 has remained unchanged at $2.05 per share over the past 60 days, while the same for 2026 has decreased marginally to $2.25 from $2.26.

The communications service provider delivered a four-quarter earnings surprise of 4.54%, on average.

Our proven model does predict an earnings beat for AT&T for the third quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is exactly the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

AT&T currently has an ESP of +0.92% and a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

During the quarter, AT&T formed a collaboration with Cisco Systems to roll out a leading-edge cloud-delivered networking and security solution, the AT&T SASE (Secure Access Service Edge). By combining Cisco Secure Access Technology and AT&T’s network expertise, the collaboration has developed a single vendor SASE service solution that effectively addresses some key pain points in the enterprise network security environment.

In the to-be-reported quarter, the company inked an agreement with PRIME FiBER, an open-access fiber infrastructure provider, to offer wholesale fiber broadband services in Arizona. It is focusing more on fiber densification, courtesy of the One Big Beautiful Bill Act that Congress recently passed. The bill is likely to spur investment and boost economic development by unlocking significant mid- and low-band spectrum, which is critical to expanding 5G capacity and coverage, particularly in rural and suburban areas.

In the quarter under review, T completed the divestiture of its remaining 70% stake in DIRECTV. The divestiture of the media business will allow AT&T to focus more on its primary growth engine, which is 5G and fiber expansion. The cash infusion is set to lower the debt burden and improve liquidity.

T also inked a definitive agreement to acquire wireless spectrum licenses from EchoStar. The deal, valued at $23 billion, is set to add approximately 20 MHz of nationwide 600 MHz low-band spectrum and about 30 MHz of nationwide 3.45 GHz mid-band spectrum to AT&T’s spectrum portfolio. In a highly saturated U.S. wireless market, greater network capacity, coverage and performance drive retention and growth in average revenue per user. This will significantly bolster the company’s 5G capabilities and close the competitive gap with T-Mobile US, Inc. (TMUS) and Verizon Communications, Inc. (VZ).

The company is also working with a leading-edge AI tool called AT&T Digital Receptionist. The tool, powered by several large language models, helps in processing incoming speech and creating responses and is also designed to block spam calls.

However, the company is affected by growing competition from other industry leaders across multiple domains. Verizon and Lumen are major players in the network security space, where AT&T is trying to gain ground in collaboration with Cisco. TMUS and VZ are also steadily expanding their 5G and fiber infrastructure. This could pose a challenge to AT&T’s network expansion initiative.

The Zacks Consensus Estimate for revenues from the Communications segment, which accounts for the lion’s share of total revenues, is pegged at $30.03 billion, while our model projects revenues of $30.66 billion.

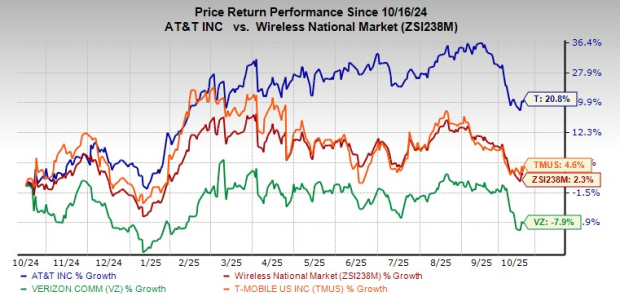

Over the past year, AT&T has gained 20.8% compared with the industry’s growth of 2.3%, outperforming peers like Verizon Communications Inc. VZ and T-Mobile US, Inc. TMUS.

From a valuation standpoint, AT&T appears to be trading relatively cheaper than the industry and below its mean. Going by the price/earnings ratio, the company shares currently trade at 11.8 forward earnings, lower than 12.53 for the industry and the stock’s mean of 12.56.

AT&T is benefiting from solid demand trends in the Communication segment. The growth is primarily driven by healthy traction in the Consumer Wireline and Mobility business. Solid uptick in the fiber broadband domain is driving growth in the Consumer Wireline. The company has been steadily expanding its fiber footprint nationwide with infrastructure investment and strategic acquisitions. Its Mobility business is benefiting from strong subscriber and postpaid average revenue per user gains.

Strategic collaboration with other industry leaders and a focus on AI integration to improve customer service are positive. However, the company is affected by weakness in the business wireline due to lower demand for legacy voice and data services as customers shifted to more advanced IP-based offerings.

In a highly saturated telecom market, growing competition from major players such as T-Mobile, Verizon and Comcast is weighing on margins. Verizon is also aggressively expanding its fiber footprint, as evidenced by its acquisition of Frontier Communications. This can challenge AT&T’s fiber expansion efforts. The company had a current ratio of 0.81 and a cash ratio of 0.22. It indicates the company may face challenges in meeting short-term debt obligations.

With a Zacks Rank #3, AT&T appears to be treading in the middle of the road, and new investors could be better off if they trade with caution. AT&T is witnessing solid momentum in the wireless business. In the face of growing competition, the company is expanding its portfolio and venturing into new domains to open up new avenues of revenue generation. However, fierce competition is a major headwind. The effort to optimize the portfolio with strategic divestiture is a positive factor. Its 5G and fiber expansion initiatives bode well for long-term growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 24 min | |

| 24 min | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Elon Musk Wants Starlink To Take On T-Mobile, Verizon, AT&THere's Why That's Easier Said Than Done

TMUS T VZ

Benzinga Prediction Markets

|

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite