|

|

|

|

|||||

|

|

|

About the Industry

The electronic gadgets we use to accurately read our commands -- and record, store, retrieve and process the information we throw at them -- run on semiconductor technology, whether analog (enabling the recording and measurement of real-world information), digital (processing information available in machine-readable language) or mixed signal (enabling conversion of analog signals to digital or digital to analog among other things). Most electronic gadgets use a combination of these components, whether in consumer, industrial, auto, medical, communications, or IoT and other markets.

The industry is cyclical and prices are elastic. Players usually serve multiple markets that offset their individual seasonality, or focus on certain core markets for which they have highly differentiated technology and relationships.

Growth Prospects Strong Despite Macro and Geopolitics

Gartner estimates that this year, PC market growth will be facilitated by on-device AI (AI PCs will represent 31% of all PC shipments, up from 17% in 2024, but slower than expected earlier because of tariff concerns). By 2026-end, 55% of PCs will be AI PCs, and by 2029 they will be the norm. Tariffs are leading to PC inventory buildup in the US, which will be worked down through the rest of the year. A Windows 11 refresh is expected to drive demand in the rest of the world. IDC expects the Windows refresh will be a big factor, driving the 4.1% increase in sales this year, with tariffs also being a significant factor.

Smartphone shipment growth is expected to increase 1% globally in 2025, with GenAI smartphones making up a 30% share. Premiumization, including slimmer designs, GenAI, foldable form factors and camera features will contribute to a 5% increase in average selling prices.

The auto market, while a smaller consumer of chips, is sluggish at the moment because of U.S. tariff-related uncertainty. Earlier, TechInsights forecasted automotive chip demand growth of 12% in 2025. This story remains because of ongoing trends toward increasing content per vehicle, fueled by electrification, ADAS/autonomy, infotainment, vehicle connectivity, and a move toward the use of domain controllers and zonal architectures, as well as centralized processing. Between 2024 and 2029, we are likely to see auto chip demand CAAGR of 10.8% (including semiconductor-based sensors).

Despite ongoing tariff-related uncertainty, U.S. manufacturing remained strong in September, with the S&P Global PMI (aggregated by Trading Economics) moving to 52 during the month, supporting the theory that the industrial end-market is returning to strength. The rate cut in September should have a positive impact.

IoT, cloud, defense, digital health, EVs and other innovative transportation, and sustainability considerations are secular drivers.

Zacks Industry Rank Indicates Strengthening Prospects

The Zacks Semiconductor – Analog and Mixed industry is housed within the broader Zacks Computer and Technology sector. It carries a Zacks Industry Rank of #42, which places it in the top 17% of the nearly 250 Zacks-classified industries. The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates improving near-term prospects.

Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1. The industry’s positioning in the top 50% of Zacks-ranked industries is based on the earnings outlook of the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions over the past year, we see that although the outlook appears weak for both 2025 and 2026, there is a stabilization and reversal of negative trends since April this year. Overall, the 2025 estimate has dropped 22.3% over the past year, while the 2026 estimate has dropped 26.1%.

Before we present a few stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

Stock Market Performance Continues to Lag

The Semiconductor – Analog and Mixed industry currently trades at a discount to both the broader Zacks Computer and Technology sector and the S&P 500.

Overall, the industry lost 6.7% of its value over the past year while the broader sector gained 26.1% and the S&P 500 gained 15.7%.

One-Year Price Performance

Industry's Current Valuation

On the basis of forward 12-month price-to-earnings (P/E) ratio, the industry is trading at a 27.68X multiple, which is its median value over the past year. Although at a discount to the broader computer and technology sector’s 28.43X, this is a premium to the S&P 500’s 23.29X.

The industry has traded between the 24.51X and 29.65X multiples over the past year.

Forward 12 Month Price-to-Earnings (P/E) Ratio

3 Stocks Worth Buying

Given the growing macro uncertainty, opportunities in the sector are limited. The following stocks are worth a closer look:

Analog Devices, Inc. (ADI): Norwood, Massachusetts-based Analog Devices is an original equipment manufacturer of analog, mixed signal and digital signal processing (DSP) integrated circuits, including amplifies, converters, CODECs, embedded processing products, DSPs, MEMS and temperature sensors, thermal management products, RF/IF components, filters and processors. It has direct sales offices, sales representatives and distributors in more than 50 countries worldwide.

The company is well positioned for the long term with its innovative product development, strong business model, customer engagement, hybrid manufacturing capacity and balance sheet strength. Although economic and geopolitical factors will continue to impact market dynamics, the above-expectation results in the last quarter including the order momentum across all industrial markets (auto impacted by pull-ins in China) and across all regions are evidence of the ongoing cyclical recovery. The strategy of maintaining lean distributor inventories while boosting internal inventories appears to be solid because it is likely to improve visibility into the channel as macro conditions, geopolitics, wars and tariffs have introduced a high level of unpredictability into the operating environment.

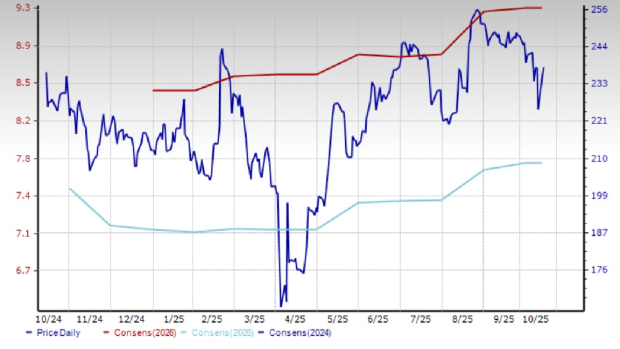

Analog Devices beat earnings estimates by 6.2% in the fiscal third quarter, with fiscal 2025 (ending October) estimates increasing 35 cents (4.7%) and 2026 estimates increasing 46 cents (5.2%) in the last 60 days. While revenue and earnings for 2025 are expected to increase a respective 15.9% and 21.5%, they’re expected to grow 11.8% and 19.4% in the following year.

ADI shares, ranked #1 (Strong Buy), have appreciated 0.7% in the past year.

Price and Consensus: ADI

ON Semiconductor Corp. (ON): ON Semiconductor offers intelligent sensing and power management products for automotive, industrial, computing and mobile applications. It caters to several megatrends including vehicle electrification and safety, sustainable energy grids, industrial automation, and 5G and cloud infrastructure.

The company is benefiting from the volatility in energy markets, which is leading to supply chain disruptions but more importantly, accelerating the adoption of electric vehicles, alternative energy and industrial automation. Its focus markets of auto and industrial were extremely strong in the last quarter, with demand outpacing supply. These two markets generated 66% of its quarterly revenue, growing 9% sequentially and 38% year over year.

The strength came from its intelligent power and sensing solutions. Its long-term service agreements (LTSAs) are a competitive moat, with customers continually expanding their scope to include even more products and, in some cases, increasing their duration up to 2029. LTSAs currently cover around 200 parts across its portfolio. Management noted signs of stabilization in non-core markets as well. Robust demand is leading some customers to co-invest in onsemi capacity expansion to secure their supply.

onsemi has made several structural changes in the last 18 months to rationalize the product portfolio and optimize the cost structure. It has also redeployed capital to higher-margin, high growth areas, such as Silicon Carbide. These initiatives have helped to stabilize its performance even in the face of a rapidly changing business environment.

ON reported June quarter earnings that missed the Zacks Consensus Estimate by 1.9%. Analysts currently expect its current-year revenue and earnings to decline a respective 15.9% and 41.7%. In 2026 however, they’re expected to increase 6.6% and 28%, respectively. The 2025 estimate has not changed in the last 60 days, while the 2026 estimate increased by a penny.

Shares of this Zacks Rank #2 (Buy) company have lost 30.4% of their value over the past year.

Price and Consensus: ON

NXP Semiconductor N.V. (NXPI): Headquartered in Eindhoven, the Netherlands, NXP offers semiconductor products like microcontrollers, application processors, communication processors, wireless connectivity solutions, analog and interface devices, radio frequency power amplifiers, security controllers, as well as a range of semiconductor-based environmental and inertial sensors for automotive, industrial, IoT, mobile and communication infrastructure applications. Products are sold to OEMs, contract manufacturers and distributors in China, the Netherlands, the U.S., Singapore, Germany, Japan, South Korea and Taiwan.

NXP is the largest semiconductor supplier into the automotive market and is poised to benefit from the proliferation of software-defined vehicles (SDVs). Its technology leadership allows it to stay ahead of its peers in this market, from which it generates nearly 60% of revenues. The company has a hybrid manufacturing model wherein it forms JVs with external foundries (such as the one with Vanguard Semiconductor last year) that enable it to expand its geographic footprint and make better use of capital. This strategy also makes sense given that advanced processes are more profitable and incentivized, while the auto market primarily requires chips from more mature processes, which therefore requires better planning to avoid supply-demand imbalance.

The ongoing softness in the industrial/IoT segment is a concern because it is driven by broader market softness and customer decisions to contain spending. Its exposure to the consumer mobile market (given to demand fluctuations and consequent volatility in prices) is also something to watch given the macro headwinds.

NXP’s last quarterly earnings represented a positive surprise of 2.3%. The Zacks Consensus Estimates for 2025 and 2026 have increased by a penny each in the last 60 days. Analysts are currently looking for a 3.9% revenue decline and 10.5% earnings decline this year, followed by 9.1% revenue growth and 18.4% earnings growth in 2026.

Shares of this Zacks Rank #3 (Hold) company have lost 9.9% of their value over the past year.

Price and Consensus: NXPI

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 |

ON Semiconductor Reports Higher Profit, Revenue on Growing AI Data Center Business

ON

The Wall Street Journal

|

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite