|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

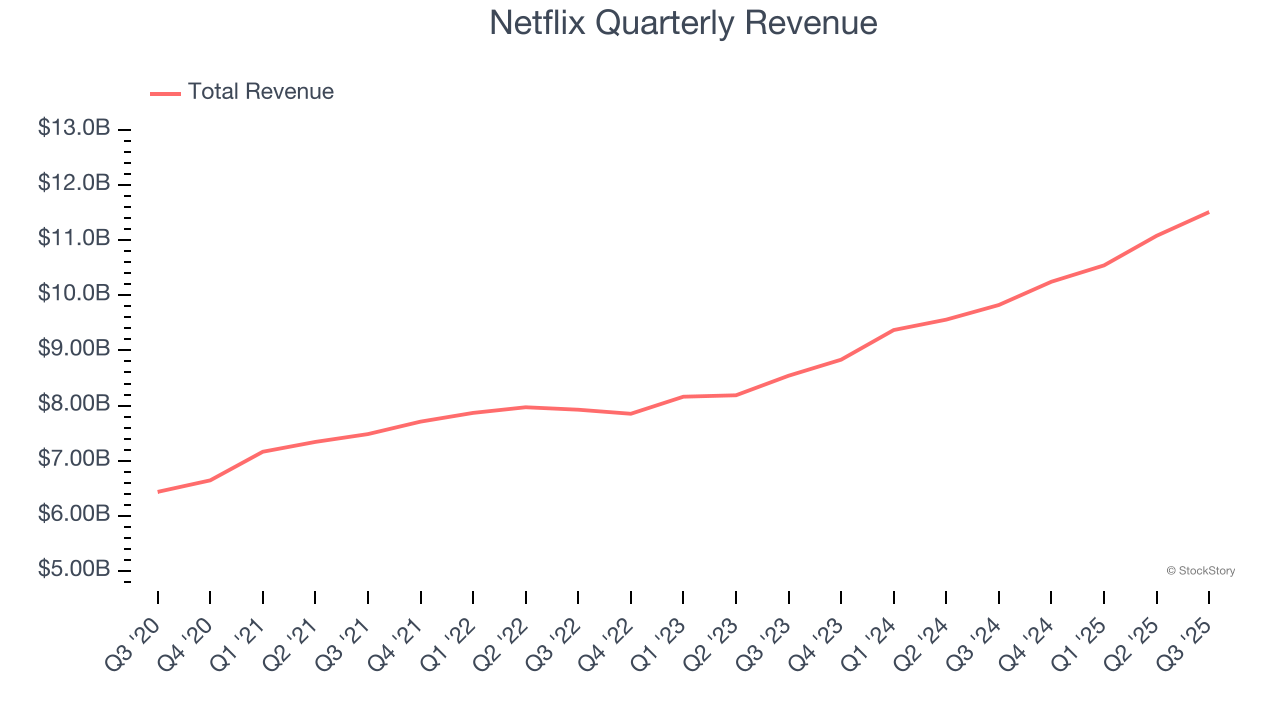

Streaming video giant Netflix (NASDAQ: NFLX) met Wall Street’s revenue expectations in Q3 CY2025, with sales up 17.2% year on year to $11.51 billion. The company expects next quarter’s revenue to be around $11.96 billion, close to analysts’ estimates. Its GAAP profit of $5.87 per share was 15.8% below analysts’ consensus estimates.

Is now the time to buy Netflix? Find out by accessing our full research report, it’s free for active Edge members.

Launched by Reed Hastings as a DVD mail rental company until its famous pivot to streaming in 2007, Netflix (NASDAQ: NFLX) is a pioneering streaming content platform.

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Netflix’s 11.3% annualized revenue growth over the last three years was decent. Its growth was slightly above the average consumer internet company and shows its offerings resonate with customers.

This quarter, Netflix’s year-on-year revenue growth was 17.2%, and its $11.51 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 16.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 14.2% over the next 12 months, an acceleration versus the last three years. This projection is particularly healthy for a company of its scale and implies its newer products and services will spur better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

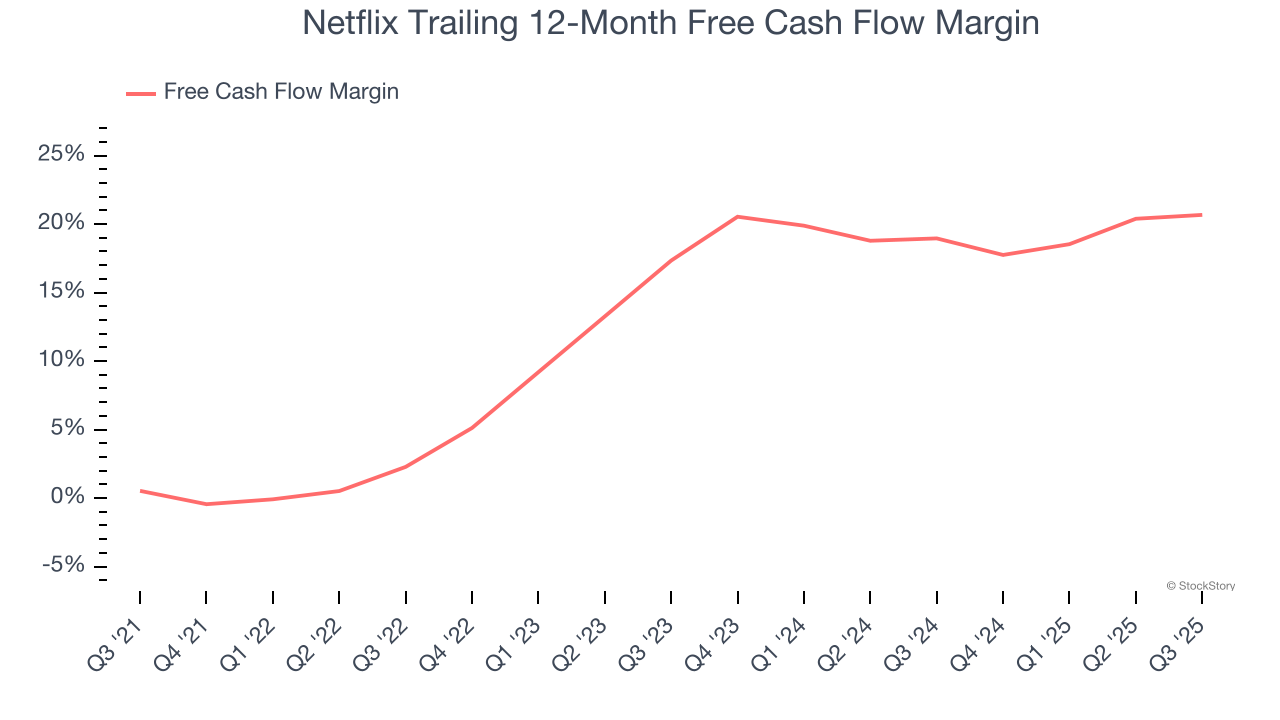

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Netflix has shown robust cash profitability, driven by its cost-effective customer acquisition strategy that enables it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 19.9% over the last two years, quite impressive for a consumer internet business.

Taking a step back, we can see that Netflix’s margin expanded by 18.4 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Netflix’s free cash flow clocked in at $2.66 billion in Q3, equivalent to a 23.1% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

This was a noisy quarter. While revenue was in line, reported operating margin and EPS were below expectations. However, a major headwind was a $619 million expense related to "an ongoing dispute with Brazilian tax authorities" that will not impact future results. Absent this expense, operating margin in the quarter would have been roughly five percentage points higher. The stock traded down 6.2% to $1,165 immediately following the results.

So do we think Netflix is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| 1 hour | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 10 hours | |

| 12 hours | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite