|

|

|

|

|||||

|

|

|

The past six months have been a windfall for Microchip Technology’s shareholders. The company’s stock price has jumped 56.2%, hitting $65.50 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Microchip Technology, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

Despite the momentum, we don't have much confidence in Microchip Technology. Here are three reasons you should be careful with MCHP and a stock we'd rather own.

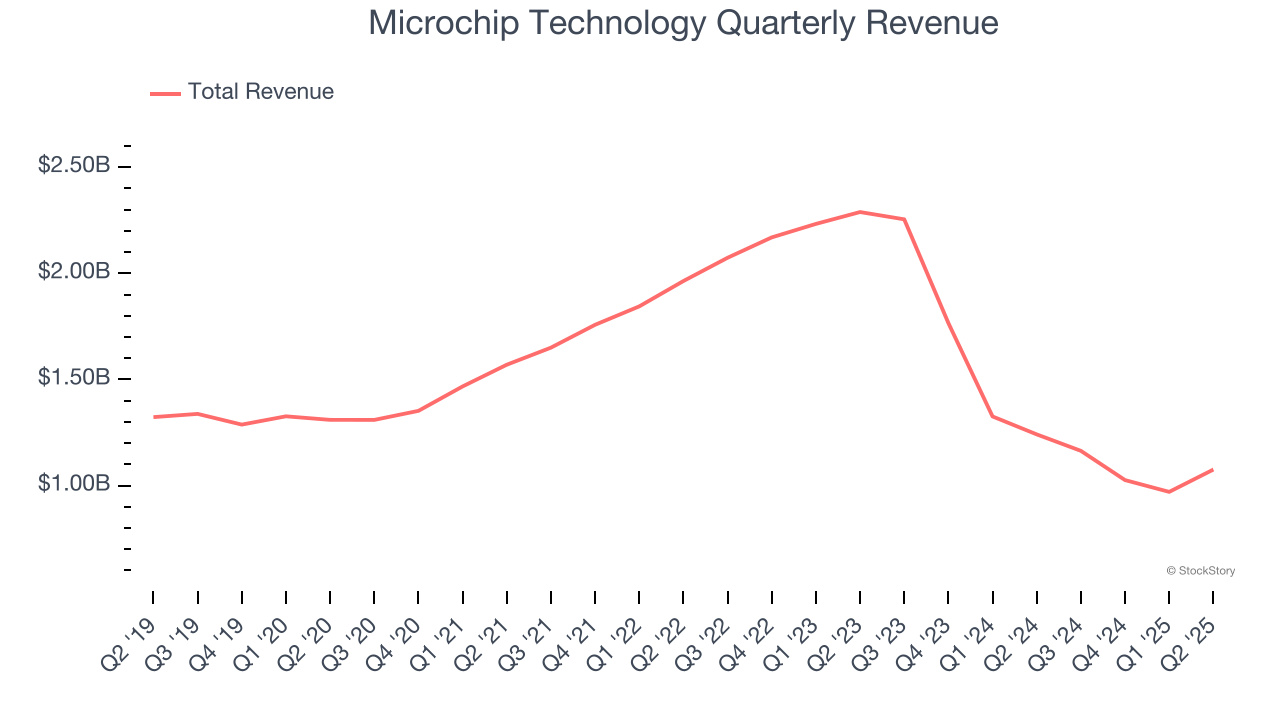

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Microchip Technology’s demand was weak over the last five years as its sales fell at a 4.2% annual rate. This was below our standards and is a sign of poor business quality. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

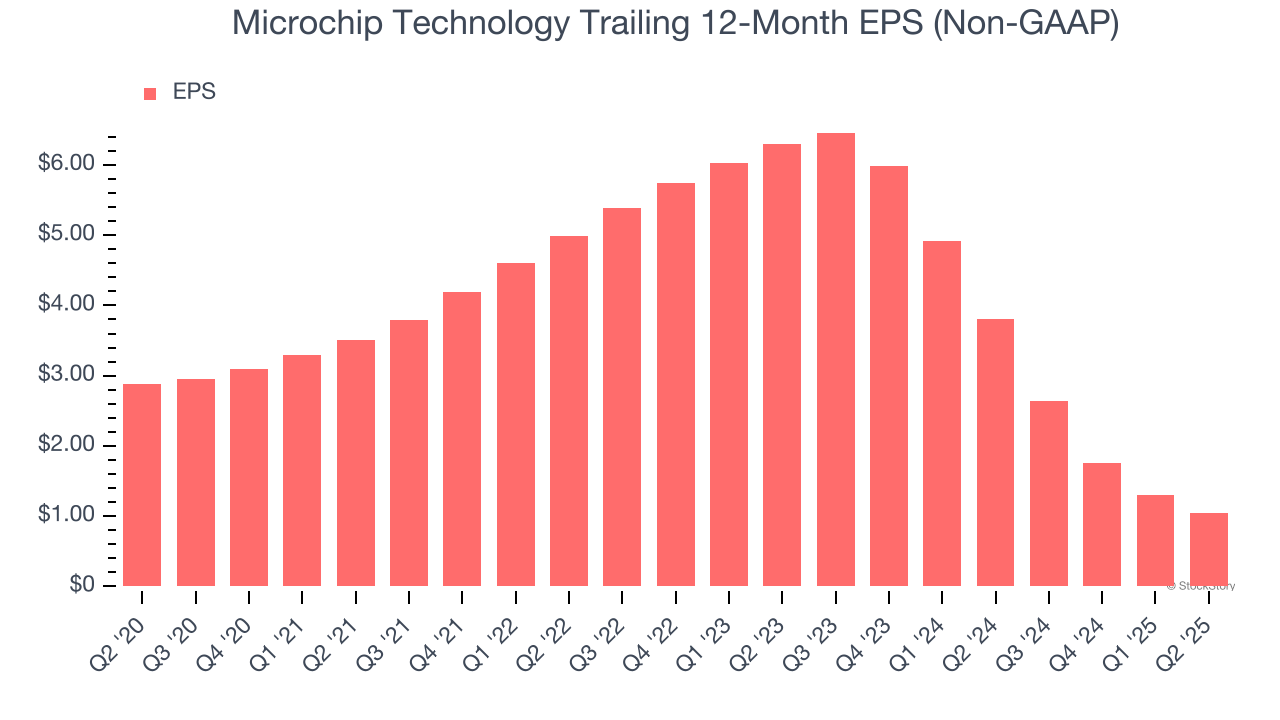

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Microchip Technology, its EPS declined by 18.5% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

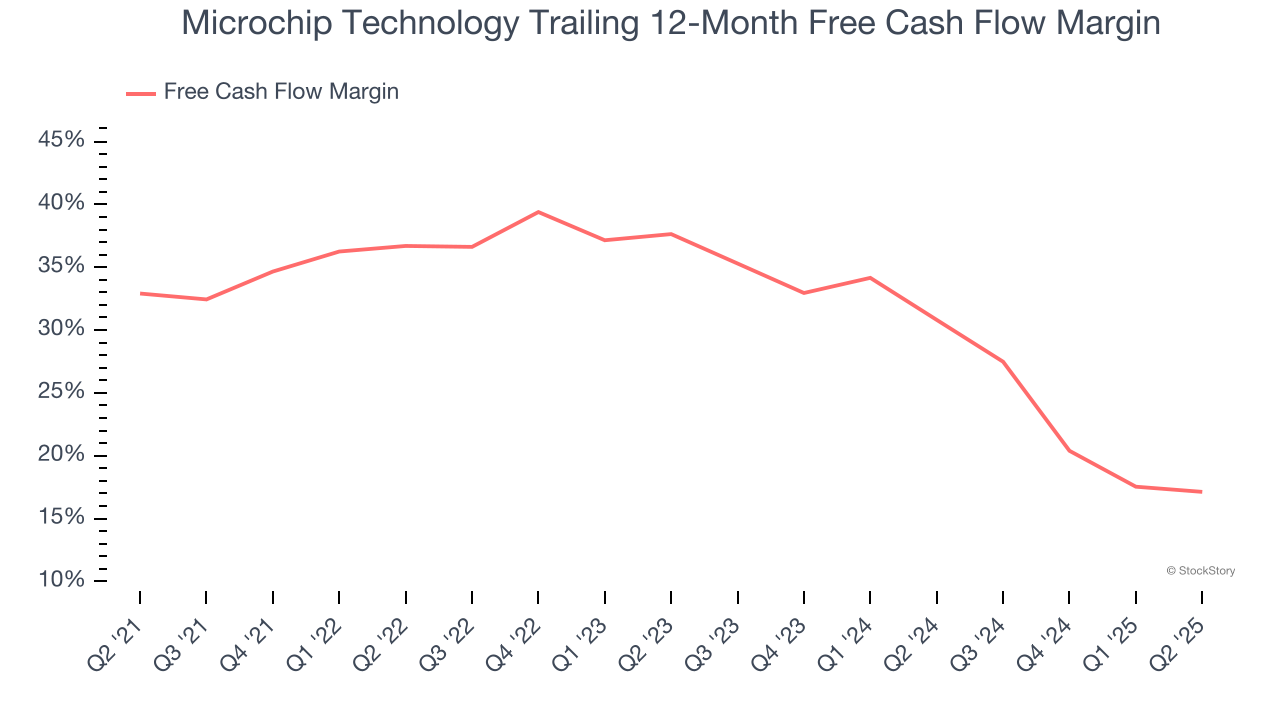

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Microchip Technology’s margin dropped by 15.8 percentage points over the last five years. Continued declines could signal it is in the middle of an investment cycle. Microchip Technology’s free cash flow margin for the trailing 12 months was 17.1%.

We cheer for all companies solving complex technology issues, but in the case of Microchip Technology, we’ll be cheering from the sidelines. After the recent rally, the stock trades at 36.8× forward P/E (or $65.50 per share). This valuation tells us a lot of optimism is priced in - you can find more timely opportunities elsewhere. Let us point you toward one of our all-time favorite software stocks.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Mar-16 | |

| Mar-16 | |

| Mar-16 | |

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-10 | |

| Mar-09 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-06 | |

| Mar-05 | |

| Mar-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite