|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Its software titles like Photoshop and Acrobat are must-haves for many professionals.

Artificial intelligence (AI), however, has intensified competition in the space.

The stock now trades at a P/E multiple that's well below the S&P 500 average.

Adobe (NASDAQ: ADBE)'s stock has been struggling mightily in recent months. It has fallen by 25% this year, and it hasn't been trading at such low levels since 2023. For a leading tech company to be in such a rapid decline, this could open up a great opportunity for investors to buy right now, particularly as an investment to hang on to for the long term.

But is Adobe's stock really a bargain buy, or are there risks that are weighing on its valuation which should make you think twice about investing in it?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

A year ago, Adobe was trading at a significant premium as its price-to-earnings (P/E) multiple was well over 40. Now, however, the stock's P/E multiple is around 21. A lower earnings multiple can signify that investors see problems with the business and are concerned about its future growth prospects, which is what I believe is happening.

In Adobe's case, there are reasons to indeed be concerned about its future. While it has some prominent software titles in its portfolio, including Photoshop and Acrobat, artificial intelligence (AI) is leveling the playing field for competitors and at the same time giving users new ways, such as chatbots, to edit and create images in seconds. As a result, it may become more difficult for customers to justify keeping a subscription to Adobe's software when there may be far cheaper alternatives.

The good news, however, is that despite these concerns, the business still hasn't been performing badly.

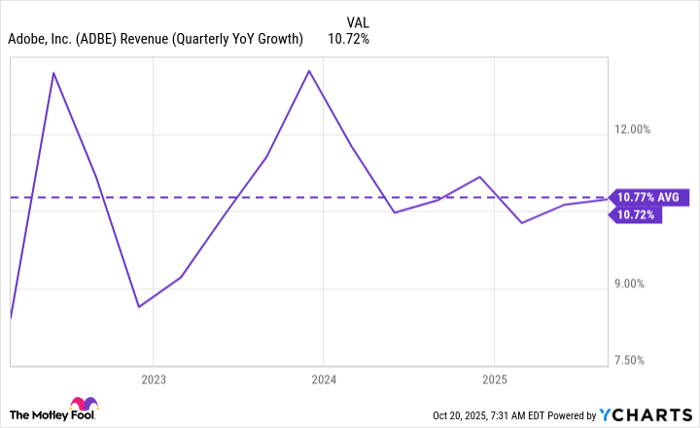

What's encouraging about Adobe is that despite the competition in AI and design software, its sales haven't fallen over a cliff. Its growth rate remains above 10%, which is in line with its average over the past few years.

ADBE Revenue (Quarterly YoY Growth) data by YCharts

But that doesn't mean it's out of the clear by any means, or that AI isn't a long-term concern. The big question boils down to whether this resiliency is a sign of strength in its brand and portfolio of products, or whether it's simply too early to tell if consumers are pivoting away from the software.

It could take some time before cancellations show up in the company's earnings and affect its numbers, as Adobe isn't known for making things easy. In the past, the Federal Trade Commissioner has taken action against the software giant about making it too difficult to cancel its recurring subscriptions, and there are plenty of social media posts expressing frustration over the issue.

While there's no denying how successful and popular Adobe's products have been over the years, whether they can withstand the threat from AI is what could make or break the stock as a long-term investment.

AI is making it easier for anyone to be a photo editor, even without advanced skills, and that can make it difficult for Adobe to convince consumers that its premium-priced software is worth subscribing to now

But Adobe also has flexibility to adjust pricing and offer promotions to win over customers -- its gross profit margin is close to 90%, which gives it plenty of room to maneuver on price while still ensuring it posts strong earnings numbers. Adobe has also enhanced its applications with AI and that has helped give its sales a boost of late.

While there is some risk with the stock, at a significantly reduced valuation and its P/E multiple now below the S&P 500 average of 25, there's a good margin of safety that comes with these shares, which is why Adobe might be worth buying on weakness today. The business may face challenges, but by no means is it in a dire situation.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 20, 2025

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe. The Motley Fool has a disclosure policy.

| 12 hours | |

| Feb-21 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite