|

|

|

|

|||||

|

|

|

The Boeing Company BA is expected to report third-quarter 2025 results on Oct. 29, before market open.

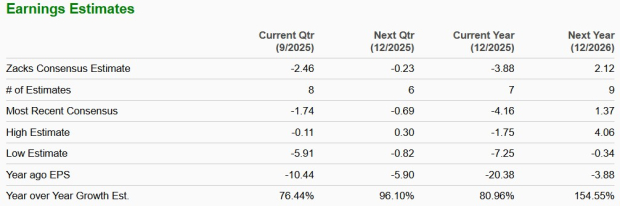

The Zacks Consensus Estimate for earnings is pegged at a loss of $2.46 per share. The Zacks Consensus Estimate for revenues is pinned at $21.92 billion, indicating growth of 22.9% from the year-ago reported figure.

The company beat on earnings in two of the trailing four quarters and missed in two, delivering an average surprise of 0.87%.

Our proven model does not predict an earnings beat for Boeing this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here as you will see below.

Earnings ESP: The company’s Earnings ESP is -49.51%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: Currently, Boeing carries a Zacks Rank #4 (Sell).

You can see the complete list of today's Zacks #1 Rank stocks here.

Some stocks in the same sector that have the combination of factors indicating an earnings beat are CurtissWright CW and Howmet Aerospace HWM. CW and HWM have an Earnings ESP of +1.59% and +0.30%, respectively. CurtissWright holds a Zacks Rank #2 and Howmet Aerospace has a Zacks Rank #3 at present.

Increased fleet utilization due to steadily rising international commercial air travel must have supported the volume of sales for commercial jet services. It is expected that this, in addition to the increased volume of government jet services supported by the growing demand for defense-related aftermarket aircraft repair, support, and upgrades, improved the top-line performance of Boeing Global Services ("BGS") segment in the third quarter. Higher commercial services revenues and strong government services margins likely boosted BGS’s operating earnings in the soon-to-be-reported quarter.

In the third quarter, Boeing’s commercial aircraft deliveries grew 37.9% year over year, reflecting continued recovery in production and delivery momentum. This substantial increase in deliveries likely translated into higher revenues for the company’s commercial segment. However, on the defense side, shipments declined 5.9% from the prior-year period. The weaker delivery volumes in this segment are expected to have partly offset some of the positives in the to-be-reported quarter.

Boeing appears to have mitigated much of its tariff risk via favorable trade deals and a strong U.S. based supply chain. By doing this, a significant negative surprise from tariffs in the third quarter is expected to have been avoided. Even with tariffs in place, the company still has to deal with supply-chain logistics, delivery ramp issues, and rising input costs, all of which are expected to have had an adverse impact on overall profitability.

In the past six months, the stock has returned 22.4% compared with the industry’s growth of 25.8%.

Boeing is currently trading at a premium compared to its industry on a forward 12-month P/S basis.

CurtissWright is also trading at a discount compared to its industry on a forward 12-month P/S basis. Howmet Aerospace is trading at a premium compared to its industry on a forward 12-month P/S basis.

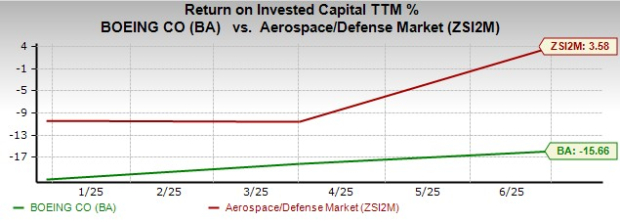

The image below shows that BA stock’s trailing 12-month return on invested capital (ROIC) not only lags the peer group’s average return but also reflects a negative figure. This suggests that the company's investments are not yielding sufficient returns to cover its expenses.

The steadily rising demand for commercial air travel and the replacement of aging fleets are driving the need for new jets and aftermarket services. These factors are important growth drivers for Boeing, the largest commercial aircraft manufacturer in America.

Although the commercial aerospace market has been benefiting from steady growth in air travel in recent times, persistent supply-chain issues, particularly arising from a shortage of aircraft parts, continue to affect the global aviation industry. For aircraft manufacturers like Boeing, this therefore presents a serious headwind.

Additionally, jet makers may face difficulties in sourcing sufficient quantities of steel and aluminum domestically, at least in the near term. Beyond higher manufacturing costs, reduced availability of these metals could further delay completion of Boeing's major aircraft program, creating uncertain challenges for this jet giant in maintaining its delivery schedules.

Boeing is expected to benefit from steadily rising international commercial air travel and solid commercial deliveries. However, lower defense deliveries and consistent supply-chain issues are expected to have offset some of the positives during the third quarter.

Considering its price underperformance, poor ROIC and consistent supply-chain issues, it is advisable for investors to avoid this stock at present.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite