|

|

|

|

|||||

|

|

|

Pharma/biotech giants Pfizer PFE and Bristol Myers BMY boast a dominant position in the lucrative oncology space.

Oncology or cancer is one of the most sought-after areas in the pharma/biotech space. As the world at large continues to grapple with a significant increase in the number of cancer patients, the market for cancer medicines is expected to grow.

Pfizer is one of the largest and most successful drugmakers in the field of oncology. Oncology sales comprise around 25% of its total revenues.

Oncology is a key therapeutic area of focus for Bristol Myers, which is developing and delivering transformational medicines in this space.

Both drugmakers have strong footholds in their respective target markets, delivering consistent returns to shareholders. Let us delve into their fundamentals, potential growth prospects, challenges and valuation levels to make a prudent investment choice as of now.

Pfizer has an innovative oncology product portfolio with a focus to target cancer from multiple angles, including small molecules, antibody-drug conjugates (ADCs), and multispecific antibodies, including other immune-oncology biologics that treat a wide range of cancers, including certain types of breast cancer, genitourinary cancer and hematologic malignancies, as well as certain types of melanoma, gastrointestinal, gynecological and lung cancer.

Approved drugs in the portfolio include Ibrance, Xtandi, Padcev, Lorbrena, Adcetris, Inlyta, Braftovi/Mektovi, Bosulif, Tukysa, Elrexfio and Talzenna among others. Breast cancer drug Ibrance is one of the top revenue generators.

The acquisition of Seagen in December 2023 strengthened PFE’s oncology portfolio by adding four ADCs — Adcetris, Padcev, Tukysa and Tivdak. The incremental sales from Seagen boosted oncology sales in 2024 and the first half of 2025. Seagen also has some next-generation ADC candidates in its pipeline and their successful development should further strengthen its portfolio.

PFE is working on the label expansion of many of its cancer drugs that should boost sales.

Pfizer recently inked a licensing agreement with 3SBio for the development, manufacturing and commercialization of SSGJ-707, a bispecific antibody targeting PD-1 and VEGF, outside China.

Pfizer also has oncology biosimilars in its portfolio and markets six of them for cancer. Oncology biosimilars primarily include Retacrit, Ruxience, Zirabev, Trazimera and Nivestym. Pfizer is also advancing a robust pipeline of oncology candidates, with several entering late-stage development. By 2030, it expects to have eight or more blockbuster oncology medicines in its portfolio.

Apart from oncology, Pfizer’s portfolio has a variety of drugs and vaccines for diseases like COVID-19, inflammation & immunology diseases, rare diseases and migraine, among others.

BMY is focused on extending and strengthening its leadership in immuno-oncology (IO), as well as diversifying beyond IO. Blockbuster IO drug Opdivo, approved for several cancer indications, drives its oncology franchise along with Yervoy and Opdualag.

The FDA recently granted approval to Opdivo Qvantig (nivolumab and hyaluronidase-nvhy) injection for subcutaneous use. Per BMY, this new subcutaneous formulation of Opdivo should help extend the reach and impact of its immuno-oncology franchise to patients into the next decade.

Reblozyl, approved for first-line MDS-associated anemia, continues to drive market share within the larger first-line ring sideroblasts negative population.

BMY’s oncology portfolio also comprises CAR-T cell therapy Breyanzi, which is approved to treat various types of B-cell malignancies.

The company has also been active on the acquisition front to expand its oncology portfolio/pipeline. In 2024, BMY acquired Mirati, a commercial-stage targeted oncology company, obtaining the rights to commercialize lung cancer medicine Krazati and to further develop several clinical assets, including PRMT5 Inhibitor.

Krazati, a KRAS inhibitor, is approved for second-line non-small cell lung cancer (NSCLC) and is in clinical development with a PD-1 inhibitor for first-line NSCLC. It is also FDA approved for advanced or metastatic KRAS-mutated colorectal cancer with cetuximab. In addition, PRMT5 Inhibitor is a potential first-in-class MTA-cooperative PRMT5 inhibitor, which is advancing to the next stage of development.

The acquisition of RayzeBio, a leader in the field of radiopharmaceuticals for solid tumor oncology, provided BMY with RYZ101, a late-stage asset, an investigational new drug engine and in-house manufacturing capabilities.

In 2022, BMY acquired Turning Point and added lead asset, repotrectinib, and other clinical and pre-clinical stage assets to its pipeline. Repotrectinib was approved by the FDA in November 2023 and is marketed under the brand name Augtyro.

Augtyro, a kinase inhibitor, is indicated for the treatment of adult patients with locally advanced or metastatic ROS1-positive NSCLC. It is also intended for the treatment of adult and pediatric patients 12 years of age and older with solid tumors that have NTRK gene fusion, are locally advanced or metastatic or where surgical resection is likely to result in severe morbidity, and have progressed following treatment or have no satisfactory alternative therapy.

The company recently collaborated with BioNTech for the global co-development and co-commercialization of the latter’s investigational bispecific antibody BNT327 across numerous solid tumor types.

Bristol Myers is also focused on developing drugs with presence in hematology, immunology, cardiovascular, neuroscience and other therapeutic areas.

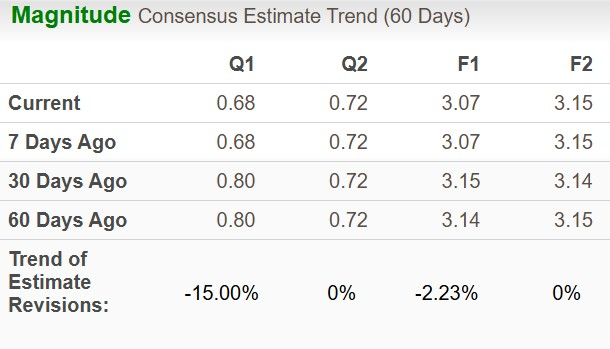

The Zacks Consensus Estimate for PFE’s 2025 sales implies a year-over-year decrease of 0.36%, and that for earnings per share (EPS) suggests a year-over-year decline of 1.29%. EPS estimates for 2025 have moved south in the past 60 days while the same for 2026 has remained unchanged in this timeframe.

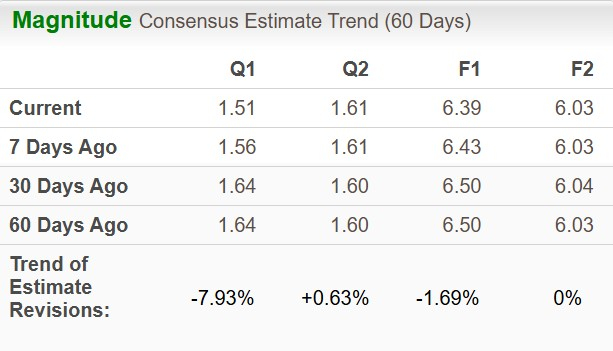

The Zacks Consensus Estimate for BMY’s 2025 sales implies a year-over-year decrease of 1.97% while that for earnings per share (EPS) suggests an increase of 455.65%. The extraordinary EPS growth rate is primarily due to an extremely low EPS figure in 2024 as a result of acquisition expenses.

EPS estimates for 2025 have moved south in the past 60 days while that for 2026 has remained unchanged in the same timeframe.

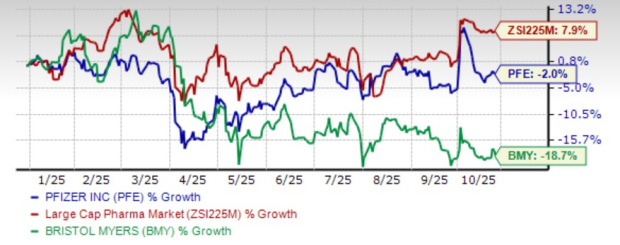

From a price-performance perspective, shares of PFE have declined 2%, while those of BMY have lost 18.7%. The large-cap pharma industry has gained 7.9% in the said period.

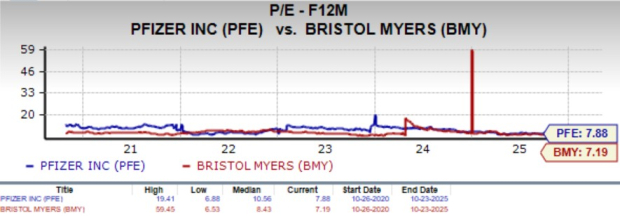

From a valuation standpoint, we use the P/E ratio of the large-cap pharma industry to compare these companies. Going by the same, PFE is slightly more expensive than BMY. PFE’s shares currently trade at 7.88X forward earnings, higher than 7.19X for BMY.

PFE and BMY’s attractive dividend yield is a strong positive for investors. However, PFE’s dividend yield of 6.97% is higher than BMY’s 5.66%.

Large pharma/biotech companies are generally considered safe havens for investors interested in this sector.

While PFE has a strong and diverse portfolio, it faces challenges like declining sales of its COVID-19 products and U.S. Medicare Part D headwinds in 2025. Several of its key products face patent expirations, which will significantly impact its top-line growth. PFE currently carries a Zacks Rank #4 (Sell).

BMY’s efforts to revive the top line in the face of generic challenges for key drugs are commendable. Growth in sales of newer drugs should enable the company to offset the impact of generic competition of key drugs. The recent collaborations and acquisitions also strengthen its pipeline.

BMY currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Hence, BMY is a better pick at present compared to PFE, given its valuation and growth prospects, while the latter grapples with multiple challenges.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours |

Bristol Myers, NVIDIA join forces to build life sciences most powerful AI factory

BMY

Pharmaceutical Technology

|

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite