|

|

|

|

|||||

|

|

|

Anheuser-Busch InBev SA/NV BUD, also known as AB InBev, is slated to release third-quarter 2025 earnings on Oct. 30, before the opening bell. The leading alcohol beverage company is likely to register year-over-year top-line growth when it reports quarterly numbers.

The Zacks Consensus Estimate for AB InBev’s quarterly revenues is pegged at $15.4 billion, indicating 2% growth from the year-ago quarter’s reported number. For third-quarter earnings, the consensus mark is pegged at 97 cents per share, suggesting a 1% decline from the prior-year reported figure. The consensus estimate for earnings has moved down 4% in the past 30 days.

In the last reported quarter, the company’s earnings per share beat the Zacks Consensus Estimate by 4.3%. It has a trailing four-quarter average earnings surprise of 10.1%.

Anheuser-Busch InBev SA/NV price-eps-surprise | Anheuser-Busch InBev SA/NV Quote

AB InBev’s results are expected to reflect the benefits of its robust strategic measures, including pricing actions, continued premiumization and other revenue-management initiatives. The company is also likely to have benefited from strong consumer demand for its brand portfolio. BUD’s relentless execution, investment in brands and accelerated digital transformation have been driving its top-line momentum for a while. These factors are expected to have bolstered the sales performance in the to-be-reported quarter.

BUD’s premiumization efforts bode well. The company has been focused on premium beer offerings, aligning with consumer preferences in the alcohol industry. It continues to build a diverse portfolio of global, international, craft and specialty premium brands, with its global brands leading the premiumization trend. The expansion of the Beyond Beer portfolio and investments in B2B platforms, e-commerce and digital marketing bode well. Such efforts are expected to have aided the company’s performance in third-quarter 2025.

However, AB InBev’s business remains under significant pressure due to soft volumes resulting from soft industries, and performance in China and Brazil. This shows that much of the company’s revenue growth is price/mix-driven rather than consumption growth. In mature markets, shifting consumer preferences, rising health consciousness, and competition from spirits and non-alcoholic alternatives are constraining volume expansion. As a result, we expect continued volume pressures in the to-be-reported quarter.

The company is expected to have witnessed elevated costs from commodity cost inflation and higher supply-chain costs, and investments to support long-term growth. In addition, a tough macroeconomic environment, including a soft consumer backdrop in China and Argentina, is concerning. Currency and interest rate fluctuations are likely to have been other deterrents. Such limitations are anticipated to have weighed on BUD’s quarterly performance.

Our proven model does not conclusively predict an earnings beat for AB InBev this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks before they are reported with our Earnings ESP Filter.

AB InBev has an Earnings ESP of -1.40% and a Zacks Rank of 4 (Sell).

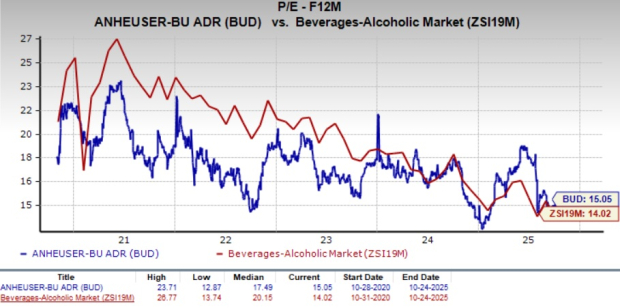

The stock has a forward 12-month price-to-earnings ratio of 15.05X compared with the five-year high of 23.71X and the Beverages - Alcohol industry’s average of 14.02X.

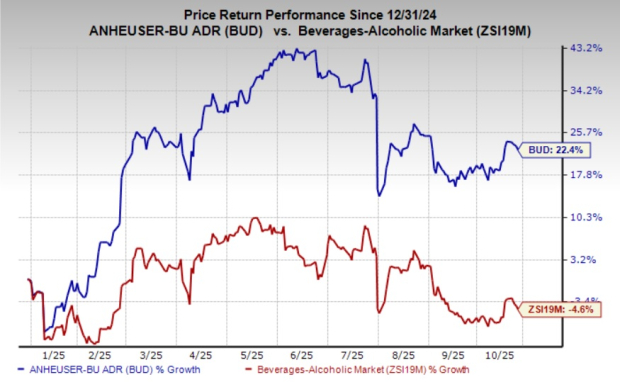

The recent market movements show that BUD shares have rallied 22.4% in the year-to-date period against the industry's 4.6% decline.

Here are some companies, which, according to our model, have the correct combination to beat on earnings this time around.

Vital Farms VITL currently has an Earnings ESP of +8.84% and flaunts a Zacks Rank of 1. VITL is anticipated to register increases in its top and bottom lines when it reports third-quarter 2025 results. The Zacks Consensus Estimate for Vital Farms’ quarterly revenues is pegged at $200 million, indicating growth of 31.7% from the figure reported in the prior-year quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Vital Farms’ bottom line has been unchanged in the past 30 days at 29 cents per share. This implies a surge of 81.3% from the year-ago quarter’s reported figure. VITL delivered an earnings beat of 35.8%, on average, in the trailing four quarters.

Monster Beverage MNST currently has an Earnings ESP of +0.82% and a Zacks Rank of 3. The company is likely to register increases in the top and bottom lines when it reports third-quarter 2025 numbers. The Zacks Consensus Estimate for quarterly earnings per share is pegged at 48 cents, suggesting a 20% rally from the year-ago period’s reported number. The consensus mark has been unchanged in the past 30 days.

The consensus estimate for Monster Beverage’s quarterly revenues is pegged at $2.1 billion, which indicates growth of 11.9% from the prior-year quarter’s actual. MNST has a trailing four-quarter earnings surprise of 0.2%, on average.

The Campbell's Company CPB has an Earnings ESP of +1.49% and a Zacks Rank of 3 at present. CPB is likely to register top and bottom-line declines when it releases first-quarter fiscal 2026 results. The Zacks Consensus Estimate for its quarterly revenues is pegged at $2.7 billion, which implies a dip of 3.7% from the figure in the prior-year quarter.

The consensus estimate for Campbell's bottom line has been unchanged at 74 cents per share in the past 30 days. The estimate indicates a 16.9% decline from the year-ago quarter’s actual. CPB delivered an earnings surprise of 6.2%, on average, in the trailing four quarters.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 15 hours | |

| Mar-31 | |

| Mar-27 | |

| Mar-26 | |

| Mar-26 | |

| Mar-26 | |

| Mar-19 | |

| Mar-18 | |

| Mar-16 | |

| Mar-13 | |

| Mar-13 | |

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite