|

|

|

|

|||||

|

|

|

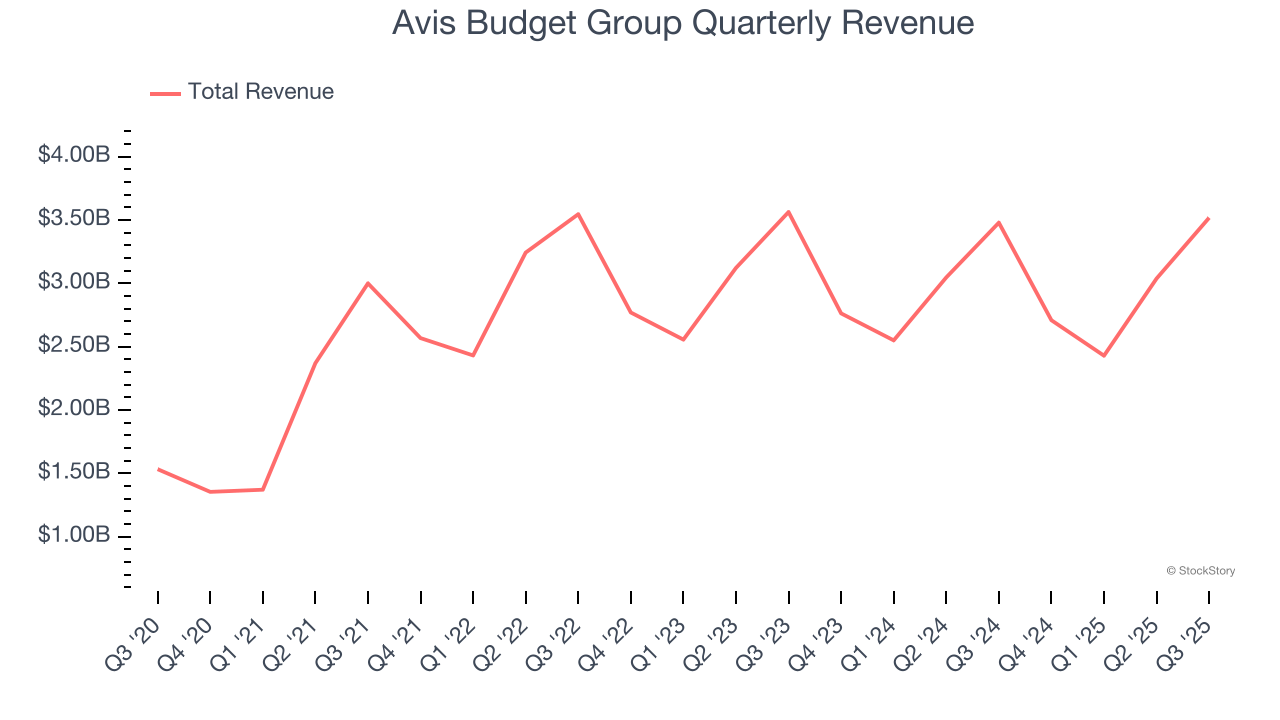

Car rental services provider Avis (NASDAQ:CAR) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 1.1% year on year to $3.52 billion. Its GAAP profit of $10.11 per share was 27.9% above analysts’ consensus estimates.

Is now the time to buy Avis Budget Group? Find out by accessing our full research report, it’s free for active Edge members.

“This quarter marked meaningful progress for Avis Budget Group as we returned to revenue growth while continuing to invest in our future. We remain focused on leading the industry through innovation and a steadfast commitment to delivering an exceptional customer experience,” said Brian Choi, Avis Budget Group Chief Executive Officer.

The parent company of brands such as Zipcar and Budget Truck Rental, Avis (NASDAQ:CAR) is a provider of car rental and mobility solutions.

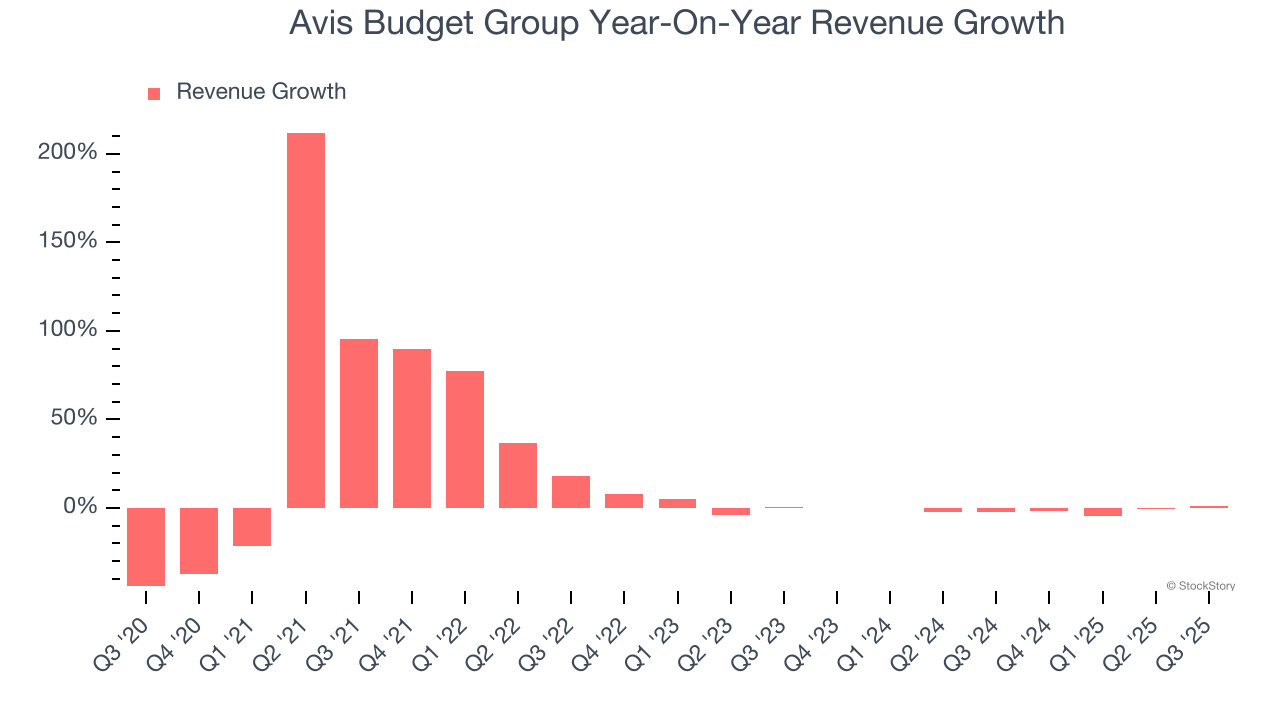

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Avis Budget Group grew its sales at an exceptional 13.5% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Avis Budget Group’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 1.3% over the last two years. Avis Budget Group isn’t alone in its struggles as the Ground Transportation industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

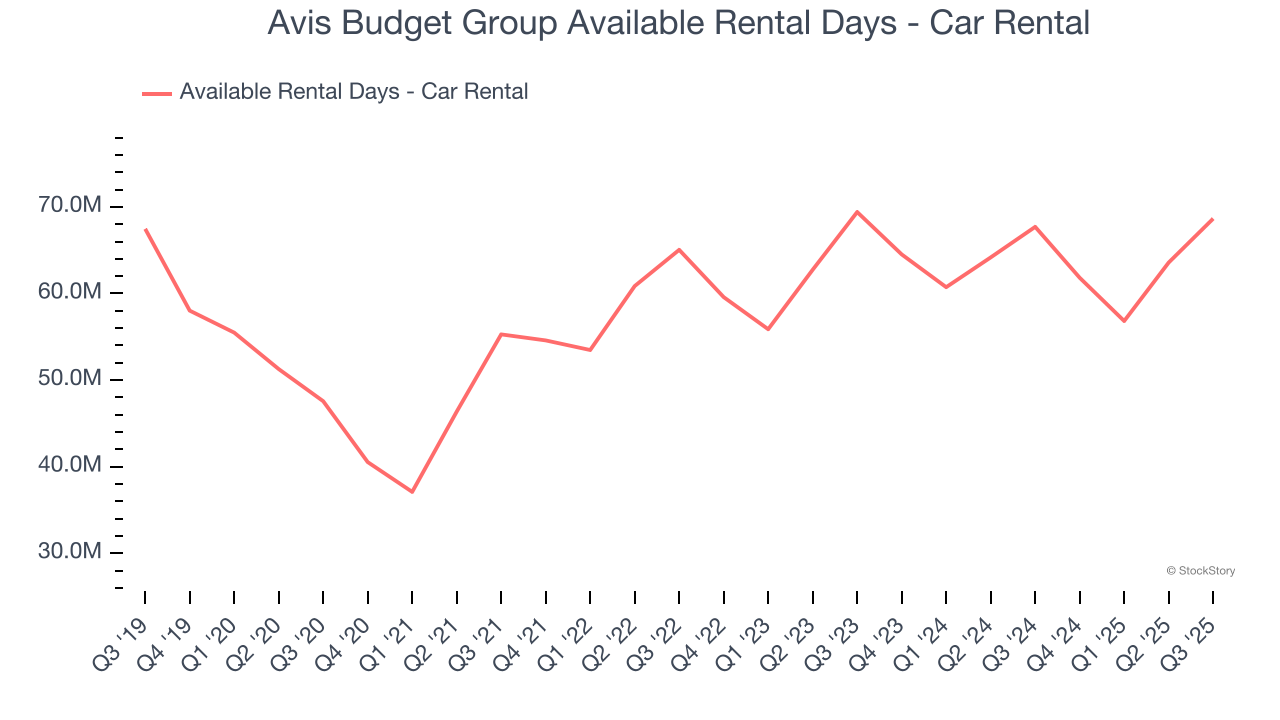

Avis Budget Group also discloses its number of available rental days - car rental, which reached 68.65 million in the latest quarter. Over the last two years, Avis Budget Group’s available rental days - car rental were flat. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, Avis Budget Group reported modest year-on-year revenue growth of 1.1% but beat Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 1.1% over the next 12 months. While this projection indicates its newer products and services will catalyze better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

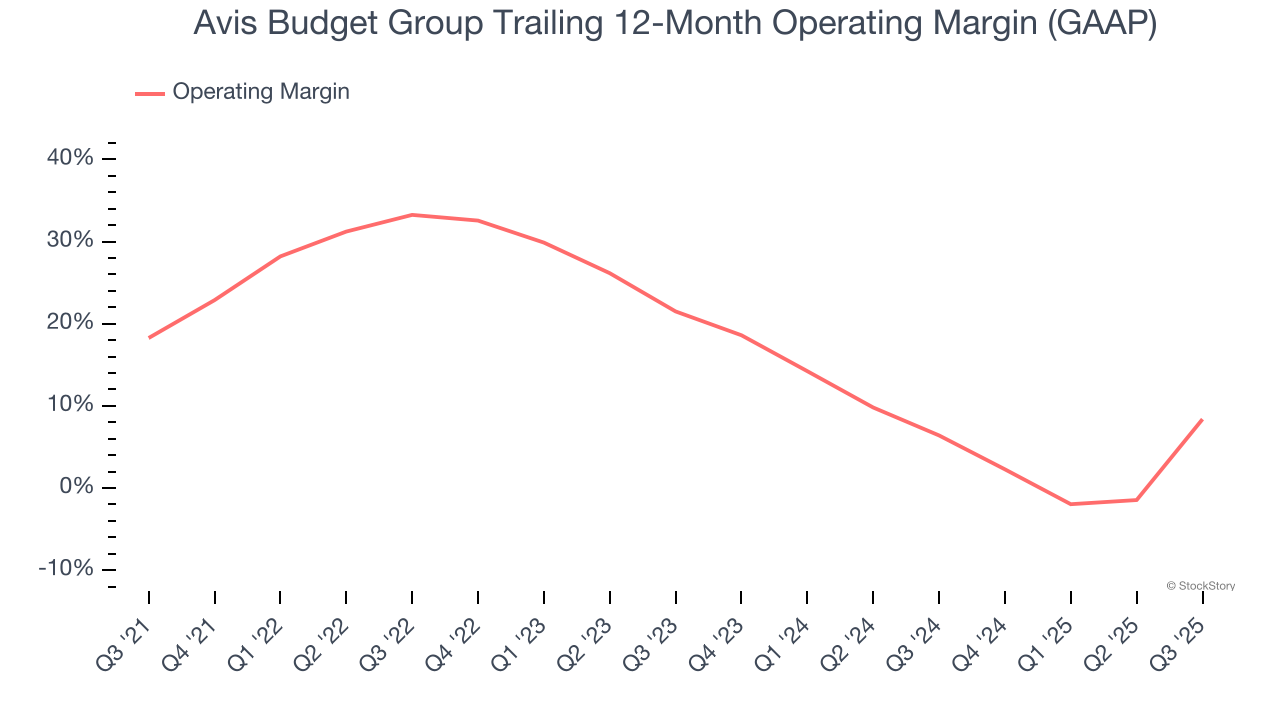

Avis Budget Group has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17.5%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Avis Budget Group’s operating margin decreased by 9.9 percentage points over the last five years. Many Ground Transportation companies also saw their margins fall (along with revenue, as mentioned above) because the cycle turned in the wrong direction. We hope Avis Budget Group can emerge from this a stronger company, as the silver lining of a downturn is that market share can be won and efficiencies found.

In Q3, Avis Budget Group generated an operating margin profit margin of 45%, up 32.6 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

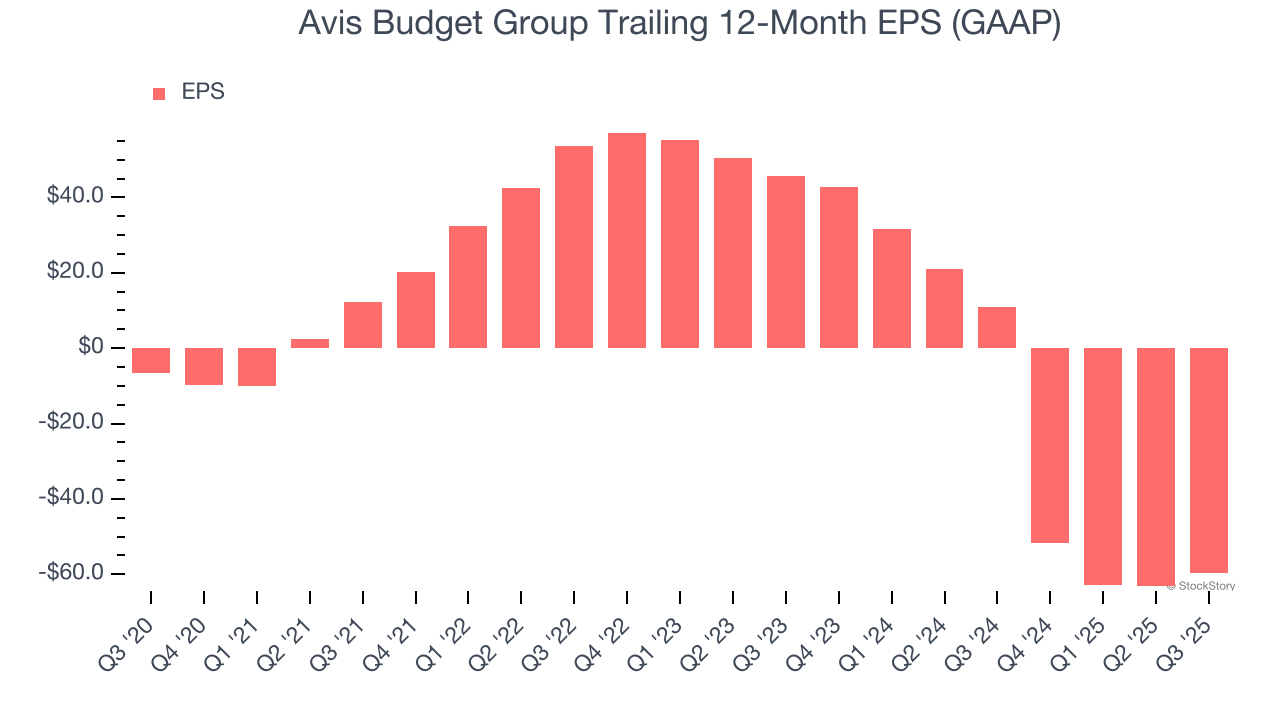

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Avis Budget Group’s earnings losses deepened over the last five years as its EPS dropped 55.7% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Avis Budget Group’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Avis Budget Group, its EPS declined by more than its revenue over the last two years, dropping 81.9%. This tells us the company struggled to adjust to shrinking demand.

In Q3, Avis Budget Group reported EPS of $10.11, up from $6.64 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

It was good to see Avis Budget Group beat analysts’ revenue, EBITDA, and EPS expectations this quarter. We Zooming out, we think this was a good print with some key areas of upside. The stock traded up 9.6% to $170 immediately after reporting.

Indeed, Avis Budget Group had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-13 | |

| Jul-09 | |

| Jul-07 | |

| Jul-06 | |

| Jun-23 | |

| Jun-23 | |

| Jun-23 | |

| Jun-23 | |

| Jun-23 | |

| Jun-22 | |

| Jun-08 | |

| Jun-01 | |

| May-29 | |

| May-28 | |

| May-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite