|

|

|

|

|||||

|

|

|

Hyatt Hotels has had an impressive run over the past six months as its shares have beaten the S&P 500 by 7.6%. The stock now trades at $148.89, marking a 32% gain. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Hyatt Hotels, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

We’re glad investors have benefited from the price increase, but we're swiping left on Hyatt Hotels for now. Here are three reasons why H doesn't excite us and a stock we'd rather own.

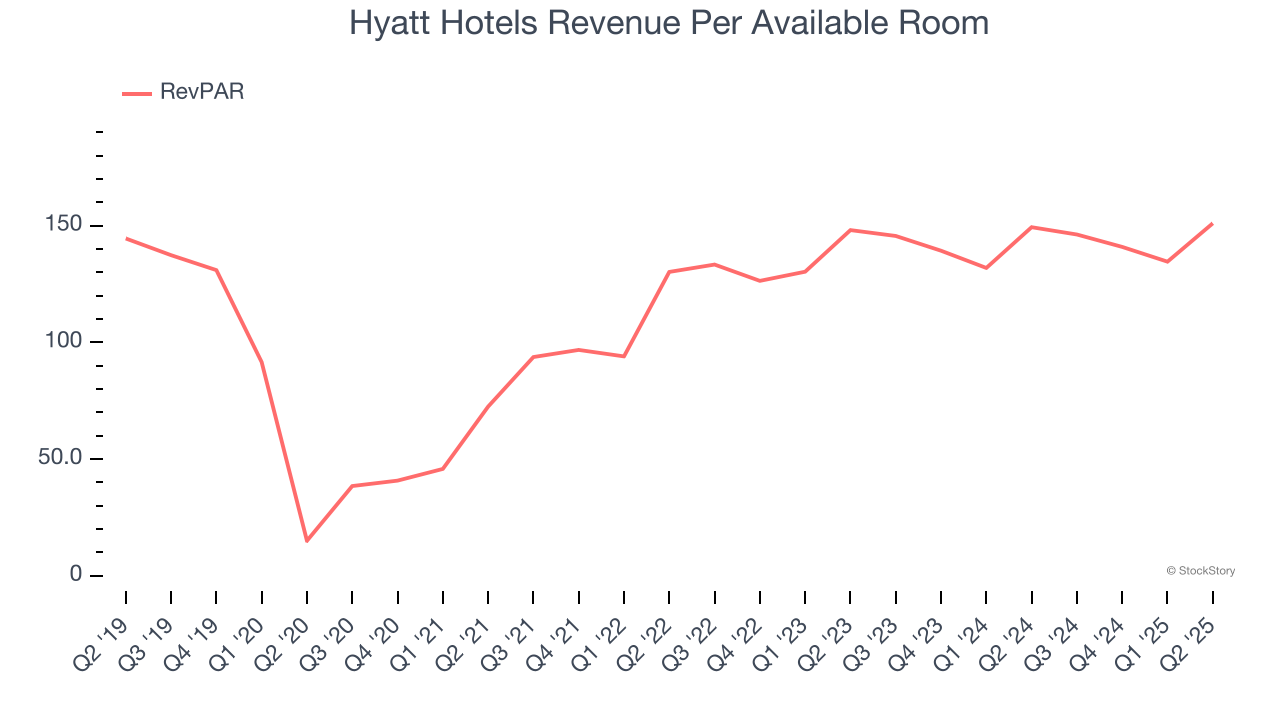

Investors interested in Travel and Vacation Providers companies should track RevPAR (revenue per available room) in addition to reported revenue. This metric accounts for daily rates and occupancy levels, painting a holistic picture of Hyatt Hotels’s demand characteristics.

Hyatt Hotels’s RevPAR came in at $150.97 in the latest quarter, and over the last two years, its year-on-year growth averaged 3.3%. This performance was underwhelming and suggests it might have to invest in new amenities such as restaurants and bars to attract customers - this isn’t ideal because expansions can complicate operations and be quite expensive (i.e., renovations and increased overhead).

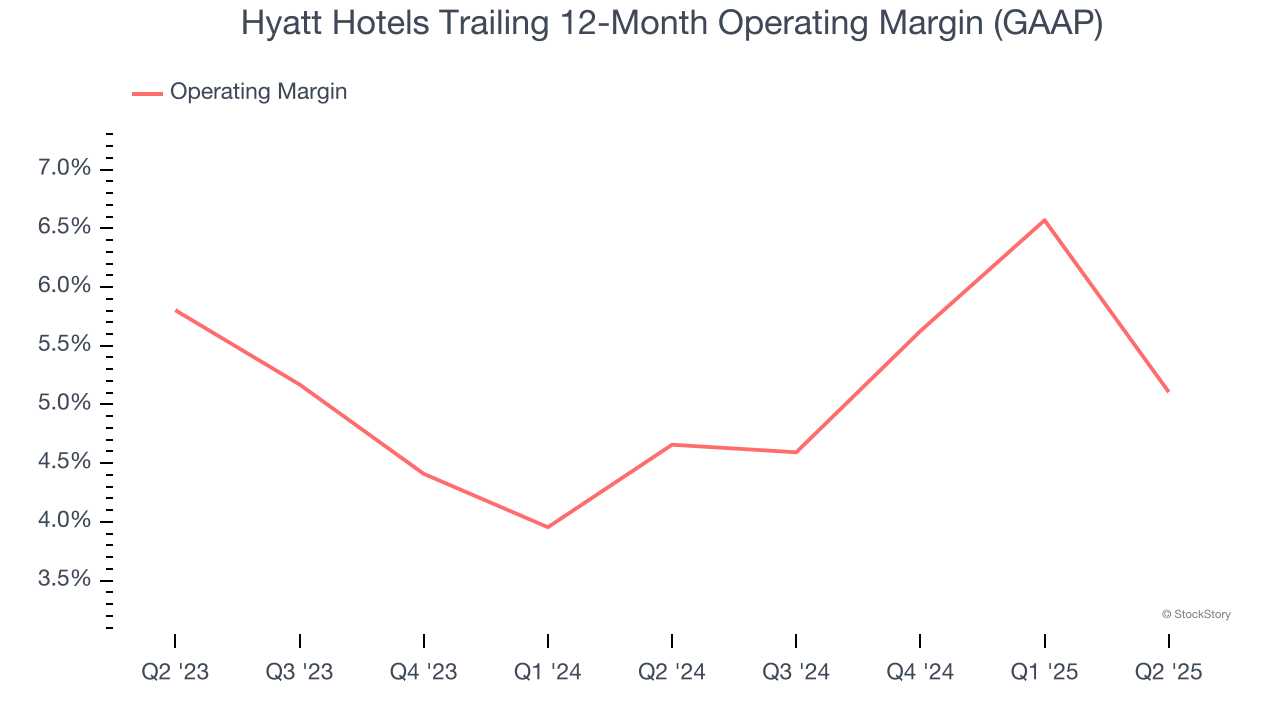

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Hyatt Hotels’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 4.9% over the last two years. This profitability was lousy for a consumer discretionary business and caused by its suboptimal cost structure.

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Hyatt Hotels’s five-year average ROIC was negative 2.6%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer discretionary sector.

Hyatt Hotels isn’t a terrible business, but it doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 48.3× forward P/E (or $148.89 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at the Amazon and PayPal of Latin America.

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Apr-02 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-26 | |

| Mar-21 | |

| Mar-19 | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-13 | |

| Mar-11 | |

| Mar-08 | |

| Feb-27 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite