|

|

|

|

|||||

|

|

|

DexCom, Inc. DXCM is scheduled to report third-quarter 2025 resultson Oct. 30, after the closing bell. In the last reported quarter, the company’s adjusted earnings per share (EPS) of 48 centssurpassed the Zacks Consensus Estimate by 6.7%.

Let us check out the factors that might have shaped DXCM’s performance prior to the announcement.

Dexcom enters the third quarter with solid operational momentum, supported by continued patient growth, improving access and a strengthening global footprint. The company raised its full-year revenue outlook following the second quarter, reflecting confidence in the durability of underlying demand and expanding reimbursement for Type 2 populations. Management also signaled that gross margins should progressively improve through the back half of the year as shipping costs normalize and inventory stabilization efforts begin to pay off.

Commercial execution remains a focal point heading into the third quarter. The product portfolio is delivering healthy uptake, particularly as G7 penetration increases and Stelo builds early adoption. Competitive noise persists, but Dexcom’s steady cadence of innovation, broadening payer coverage, and enhancements to data and usability position it well.

Third-quarter performance is likely to have benefited from ongoing access expansion and smoother channel operations. Dexcom highlighted strong new patient additions in each of the past two quarters and noted that more than 100 health systems are now integrated with Epic, supporting prescription workflow and reducing onboarding friction. Coverage continues to broaden for people with Type 2 diabetes who are not on insulin, as Dexcom secured access through a third major PBM and expects roughly six million covered lives this year. These tailwinds are likely to have contributed to healthier prescription trends and stronger pharmacy channel throughput during the third quarter.

Per the second quarter earnings call, management highlighted signs of continued stabilization within the DME channel, noting that relationships with major distributors are now much stronger than before and that efforts to ensure adequate inventory and improve communication have helped restore confidence among partners. The company also underscored progress on customer support initiatives, including the rollout of a nationwide pharmacy warranty program that allows users to access replacement sensors as early as the same day if needed.

These operational improvements are likely to have supported smoother fulfillment and reduced service disruptions in the third quarter, helping sustain patient adherence and sensor utilization. Improved channel execution may also have contributed to steadier prescription trends and limited churn, providing a modest tailwind to revenue and overall customer satisfaction through the period.

Dexcom’s international business maintained healthy growth entering into the third quarter, driven by expanding Type 2 access and ongoing market penetration. Coverage for people with Type 2 diabetes in regions such as Ontario, alongside momentum in markets like France and Japan, helped accelerate adoption in the second quarter. The company continues to invest in primary care education and digital prescribing tools to support broader usage across geographies.

Management spoke confidently about international contribution through the balance of 2025, noting that growing awareness among primary care providers and improving prescription visibility should help sustain steady volume trends. Despite some variability across reimbursement systems, Dexcom’s strengthening clinical and economic case remains a supportive backdrop as the company advances its CGM offerings globally.

In the third quarter, these dynamics likely supported continued adoption in key markets such as Canada, Japan, and Europe, with expanding Type 2 access and primary-care engagement helping drive incremental patient starts. Broader utilization of Dexcom ONE+ and improving market access could have also supported sequential volume growth, tempering reimbursement variability and contributing modestly to international revenue momentum during the period.

Stelo remains an early but important growth vector as Dexcom builds a consumer-friendly platform for people with prediabetes and Type 2 diabetes who are not using insulin. Management noted more than 400,000 app downloads as of the second quarter and highlighted its rollout across new channels, including Amazon. The company is also enhancing the Stelo experience through health ecosystem partnerships, most notably with Oura, which integrates glucose insights with activity, sleep and stress data. Smart Food Logging, an AI-driven feature launched during the second quarter, is designed to increase user engagement and help translate glucose patterns into actionable insights.

While still relatively small in financial contribution, Stelo is expected to represent roughly 2% to 3% of 2025 sales. In the third quarter, these efforts likely supported incremental user growth and broader engagement, aided by expanded distribution and improving feature depth. Early integration benefits may have helped drive more consistent usage patterns, while continued digital marketing and co-promotion through partners like Oura likely sustained momentum. Management reiterated that the product is resonating with its target audience, and ongoing feature expansion and personalization could help accelerate adoption as the category develops.

DexCom, Inc. price-eps-surprise | DexCom, Inc. Quote

Dexcom raised its full-year 2025 revenue outlook to a range of $4.60 to $4.625 billion following second-quarter results, reflecting 14 to 15 percent growth. Margin expectations remain unchanged, with full-year gross margin projected at approximately 62 percent and operating margin at roughly 21 percent. Management expects sequential improvement in gross margin in both the third and fourth quarters as expedited freight costs ease, inventory levels normalize, and manufacturing scale efficiencies improve.

The company exited the second quarter with more stable production output, confidence in cost trajectory and solid sales momentum. These dynamics are likely to have supported better cost absorption and steadier fulfillment in the third quarter, helping gross margin move toward its full-year target. Management continues to expect additional leverage as the G7 mix increases and warranty-related service capabilities shift toward pharmacy, which should help maintain customer satisfaction and support operational efficiency.

For third-quarter 2025, the Zacks Consensus Estimate for revenues is pegged at $1.18 billion, implying an improvement of 18.4% from the prior-year quarter’s reported figure.

The consensus estimate for EPS is pegged at 57 cents, indicating an increase of 26.7% from the prior-year period’s reported number.

Per our proven model, the combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. That is not the case here, as you will see below.

Earnings ESP:Cardinal Health has an Earnings ESP of -3.04%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank:The company currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

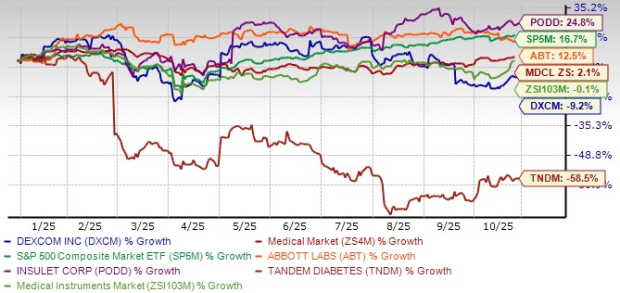

In the year-to-date period, Dexcom’s shares have plunged 9.2%, underperforming the Medical Instruments Market’s 0.1% contraction and the Medical Market’s 2.1% gain. DXCM has also lagged the S&P 500 Composite’s 16.7% increase.

Year-to-Date Price Comparison

Among key peers, Insulet PODD has led the group with a 24.8% rise, while Abbott Laboratories ABT posted solid growth of 12.5%. In contrast, Dexcom (DXCM) is down 9.2% in the year-to-date period, while Tandem Diabetes TNDM has significantly lagged, plunging 58.5%.

From a valuation standpoint, DXCM’s forward 12-month price-to-sales ratio is 5.33X, above the Medical Instruments Market at 4.35X. The company is trading at a discount to PODD at 7.57X, but at a premium to TNDM at 0.94X. Meanwhile, ABT stands at 4.66X, placing DXCM roughly in the middle of its core diabetes-technology peers.

Dexcom’s long-term runway is supported by the continued expansion of the CGM category beyond its traditional Type 1 base. Management remains focused on unlocking the broader Type 2 and pre-diabetes markets, where penetration today is still minimal despite compelling clinical evidence. Coverage is steadily improving, including recent wins in the U.S. pharmacy channel and public reimbursement expansion in regions like Ontario. In parallel, the Stelo platform is helping Dexcom participate in an even wider metabolic-health audience, supported by ecosystem integrations such as Oura and app-level enhancements that deepen engagement. As prescribing broadens in primary care and digital workflows like Epic integration reduce friction, Dexcom’s addressable market is poised to scale materially over the coming years.

Innovation remains central to Dexcom’s long-term strategy. The company is advancing a pipeline that includes the 15-day G7, which begins rolling out in the second half of 2025, and G8, its next-generation platform designed to improve usability and wearability. Software continues to evolve quickly; Dexcom has already introduced more than a dozen app updates this year to enhance data visualization, connectivity, and AI-guided food logging. These steady improvements strengthen differentiation and help the company meet the needs of a growing mix of users, including people with Type 2 diabetes, metabolic-health consumers, and specialty populations like gestational patients. With additional RCT readouts expected in 2026 for Type 2 non-insulin users, Dexcom has multiple clinical catalysts that could reinforce the case for broader adoption.

Operational scaling offers clearer visibility into Dexcom’s long-term margin trajectory. Management noted progress rebuilding inventory and boosting production to meet demand, even amid elevated freight expenses. As inventory normalizes and shipping becomes more efficient, gross margins are expected to trend toward the full-year target. Expanded commercial infrastructure and strengthened DME relationships, along with same-day warranty access through retail pharmacies, are enhancing supply reliability and the customer experience. Together, these initiatives position Dexcom to drive profitable growth and sustained operating leverage.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite