|

|

|

|

|||||

|

|

|

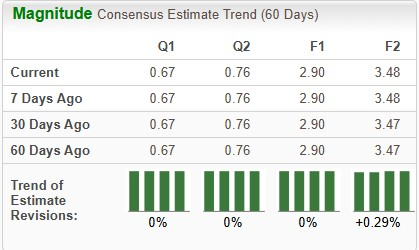

Uber Technologies UBER is slated to release third-quarter 2025 results on Nov. 4, before market open. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings and revenues is pegged at 67 cents per share and $13.26 billion, respectively.

The earnings estimate for the to-be-reported quarter has remained stable over the past 60 days. The Zacks Consensus Estimate for quarterly revenues indicates an 18.5% uptick from the year-ago quarter’s figure. The same for quarterly earnings indicates a 44.2% decline from the year-ago quarter’s figure.

For 2025, the Zacks Consensus Estimate for UBER’s revenues is pegged at $51.43 billion, implying an expansion of 16.9% year over year. The consensus mark for 2025 EPS is pegged at $2.9, implying a decline of 36.4% on a year-over-year basis.

In the trailing four quarters, this company’s earnings surpassed estimates on each occasion, the average beat being 199.8%.

Uber Technologies, Inc. price-eps-surprise | Uber Technologies, Inc. Quote

Our proven model does not conclusively predict an earnings beat for UBER this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

UBER has an Earnings ESP of -1.30% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Uber’s gross bookings are likely to have been impressive in the September quarter. The company expects gross bookings in the $48.25-$49.75 billion range, indicating 17-21% growth on a constant-currency basis compared with third-quarter 2024 results.

Our estimate for gross bookings in the third quarter of 2025 is pegged at $48.3 billion, representing 17.9% growth from the actual third-quarter 2024 results. We expect both its mobility and delivery segments to record double-digit increases in gross bookings in the September quarter. In the third quarter, Uber expects adjusted EBITDA to be in the range of $2.19 billion to $2.29 billion, indicating year-over-year growth of 30% to 36%.

However, tariff-related headwinds are likely to hurt results. We believe that more than the financial numbers, it is the guidance that investors will watch more closely. Uber has been focusing on autonomous vehicles to drive growth. The company is expected to provide updates on the same on the third-quarter conference call.

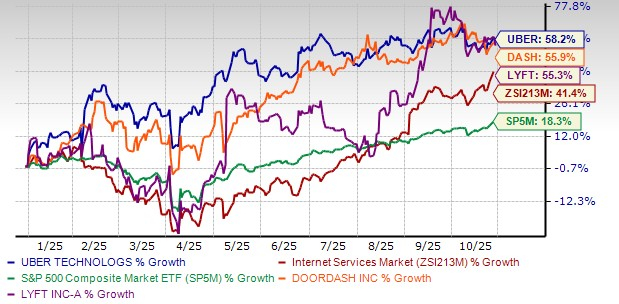

Uber has navigated the recent tariff-induced stock market volatility well, registering a 58.2% year-to-date gain, while the Zacks Internet-Services industry is up 41.4%. The S&P 500 index has risen 18.3%. Uber’s main competitor, Lyft LYFT, has gained only 55.3% in the same timeframe. Another industry player, DoorDash DASH, too, has lagged Uber year to date, gaining 55.9%.

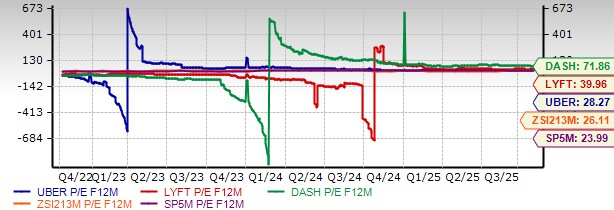

From a valuation perspective, Uber is trading at an expensive level compared with its industry and the S&P 500. Going by its price/earnings ratio, the company is trading at a forward earnings multiple of 28.27, above the industry’s 26.11 and the S&P 500's 23.99. The company has a Value Score of D. Meanwhile, Lyft trades at a forward earnings multiple of 39.96, whereas DoorDash’s P/E sits at 71.86. Lyft and DoorDash have a Value Score of C and F, respectively.

Agreed that Uber’s valuation is anything but tempting. The company’s high debt levels and concerns pertaining to currency represent further headwinds. However, not all is gloom and doom for this dominant ride-sharing company.

The company’s diversification efforts and shareholder-friendly approach are praiseworthy. Uber’s large size (market capitalization of $201.08 billion) positions it well to overcome turbulent times, such as the current one. Diversification is imperative for big companies to reduce risks and Uber has excelled in this area. The company has engaged in numerous acquisitions, geographic and product diversifications and innovations. Uber’s endeavors to expand into international markets are commendable and provide it with the benefits of geographical diversification.

Prudent investments enable Uber to extend its services and solidify comprehensive offerings. Moreover, Uber aims to gain a stronghold in the highly promising robotaxi market through strategic partnerships. To this end, the company has partnerships with many companies. By adopting this approach, Uber has avoided the massive R&D costs associated with developing autonomous systems independently.

So, all in all, it is worth holding on to Uber stock now. However, investing ahead of its upcoming results does not seem like a good idea. It is better to wait for management’s commentary on tariffs and fourth-quarter guidance to get more clarity on near-term prospects.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 38 min | |

| 3 hours | |

| 11 hours | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

JOBY Stock On Track To Snap 5-Week Slide On FAA Milestone: Why One Analyst Still Sees A 32% Downside

UBER

New feeds test provider finance

|

| Feb-27 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite