|

|

|

|

|||||

|

|

|

Fomento Economico Mexicano S.A.B. de C.V. FMX, alias FEMSA, reported third-quarter 2025 adjusted net majority earnings per ADS of 88 cents, down from $1.37 in the year-ago quarter and missed the Zacks Consensus Estimate of $1.06. The company reported net majority earnings per ADS of 38 cents (Ps. 70 cents per FEMSA unit).

Net consolidated income was Ps. 5,838 million (US$318.2 million), reflecting a decline of 36.8% from the year-ago quarter.

Total revenues were US$11.7 billion (Ps. 214,638 million), which rose 9.1% year over year in the local currency and beat the Zacks Consensus Estimate of $11.2 billion. Revenue growth was driven by gains across all its business units and favorable currency rates, particularly in Europe, due to the depreciation of the Mexican Peso against many of the foreign operating currencies. Including the currency effects and M&A, comparable revenues grew 4.9% year over year.

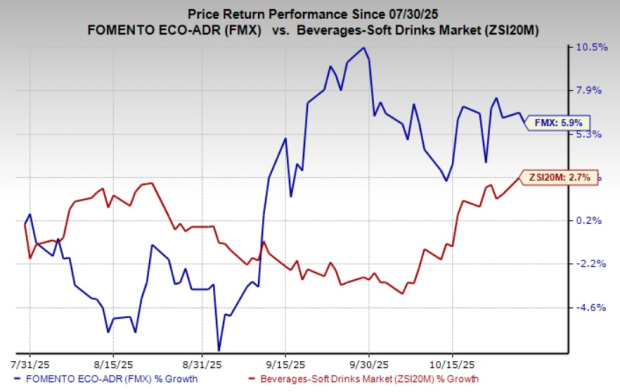

Shares of this Zacks Rank #2 (Buy) company have rallied 5.9% in the past three months compared with the industry’s 2.7% growth.

FEMSA’s gross profit rose 8% year over year to Ps. 85,709 million (US$4.67 billion). The consolidated gross margin contracted 40 basis points (bps) to 39.9%, driven by gross margin contractions in Coca-Cola FEMSA and Fuel, and the consolidation of its lower-margin US operation within Proximity Americas. These were partly offset by margin expansion in OXXO Mexico within Proximity Americas, and stable margins at Health and Proximity Europe. Including the currency effects and M&A, gross profit rose 7.7% year over year.

The company’s gross margin expanded 80 bps at Proximity Americas, and was flat at both Proximity Europe and Health divisions. However, the gross margin contracted 60 bps at the Fuel segment and 100 bps at Coca-Cola FEMSA.

FEMSA’s operating income (income from operations) improved 4.3% year over year to Ps. 18,126 million (US$988.1 million), driven by growth across all business units, except Health and Fuel, as well as favorable currency effects, particularly in Europe. Including the currency effects and M&A, operating income increased 6.5% year over year. The consolidated operating margin decreased 40 bps to 8.4%, caused by declines across the Health and Fuel segments, as well as the consolidation of the US Proximity business. This was partly negated by operating margin growth in OXXO Latam, Coca-Cola FEMSA and Proximity Europe, as well as flat margin in OXXO Mexico.

Fomento Economico Mexicano S.A.B. de C.V. price-consensus-eps-surprise-chart | Fomento Economico Mexicano S.A.B. de C.V. Quote

Proximity Americas: Total revenues for the segment rose 9.2% year over year to Ps. 84,738 million (US$4.6 billion). The company reported a 1.7% growth in same-store sales for Proximity Americas, caused by a 4.9% rise in average customer tickets, offset by a 3.1% store traffic decline. Including currency effects and M&A, revenues at Proximity Americas rose 4.8% year over year and same-store sales were up 1.8%. The strong top-line performance reflects improved same-store sales, the consolidation of the US operation into the results, and currency tailwinds. The company noted that the challenging environment continued in Mexico due to a soft consumer environment.

The Proximity Americas division had 25,378 OXXO stores as of Sept. 30, 2025. Operating income improved 7.1% year over year, and 6.6% including currency effects and M&A. The segment's operating margin contracted 20 bps to 8.8%, resulting from higher selling expenses, which rose at a faster pace than revenues. This increase was partly driven by higher minimum wages in Mexico, partially offset by cost-containment measures such as variable shift policies that reduced staffing needs per OXXO store, along with other efficiency initiatives. The remaining uptick in selling expenses is mainly attributable to the ongoing expansion of OXXO LATAM and the integration of Delek operations.

Proximity Europe: Total revenues for the segment grew 10.1% year over year to Ps. 14,837 million (US$808.8 million). The segment benefited from currency appreciation of the Euro and the Swiss Franc against the Mexican peso. Excluding currency effects, total revenues for the segment were up 3.3% year over year, aided by improved retail sales, mainly in Switzerland, as well as positive trends in Swiss B2C foodservice. This was partly offset by lower sales in its B2B foodservice business. Operating income for the segment rose 29.1% year over year. The operating margin expanded 70 bps to 4.8%, driven by higher retail sales in Switzerland, contributions from B2C Swiss foodservice and effective cost management.

Health Division: The segment reported total revenues of Ps. 21,483 million (US$1.19 billion), up 2.9% year over year and 4.5% on a currency-neutral basis. Revenues were aided by growth in Colombia, Ecuador and Chile, partially offset by a challenging competitive landscape in Mexico. The segment’s store base reached 4,391 locations as of Sept. 30, 2025. Same-store sales rose 0.8% in Mexican pesos and 4.1% on a currency-neutral basis. The operating income declined 4% year over year, while the operating margin contracted 30 bps to 4%.

Fuel Division: Total revenues rose 5% year over year to Ps. 17,933 million (US$977.6 million). Average same-station sales rose 8.3%, driven by a 9.6% increase in the average volume and a 1.2% decline in the average price per liter, offset by a decline in the wholesale business volume. The company had 558 OXXO Gas service stations as of Sept. 30, 2025. Operating income fell 0.8%, with operating margin contracting 30 bps to 4.6%. The contraction reflects the company’s continued focus on driving efficiencies and streamlining its organization to navigate the voluntary, industry-wide price commitments.

Coca-Cola FEMSA: Total revenues for the segment advanced 3.3% year over year to Ps. 71,884 million (US$3.9 billion). On a currency-neutral basis, revenues moved up 5.1%. Coca-Cola FEMSA’s consolidated operating income increased 6.8% year over year and 6.2% on a currency-neutral basis. The segment’s operating margin expanded 50 bps to 14.3%.

As of Sept. 30, 2025, FEMSA had cash and cash equivalents of Ps. 123,635 million (US$6.7 billion). The company’s long-term debt was Ps. 130,822 million (US$7.1 billion).

In the third quarter of 2025, capital expenditure totaled Ps. 13,128 million (US$715.6 million), an increase from the prior year due to higher spending in Coca-Cola FEMSA to increase production and distribution capacity. This was offset by lower CAPEX across the rest of its businesses due to reduced investments following the temporary pause in the expansion strategy at OXXO Chile and Peru, as well as in Health Mexico.

Proximity Americas recorded slightly lower CAPEX in Mexico, as its strategy focuses on more selective store openings, particularly the less CAPEX-intensive OXXO Nicho stores, along with the remodeling and optimization of existing locations.

We have highlighted three other top-ranked stocks from the Consumer Staples sector, namely PepsiCo Inc. PEP, Coca-Cola Europacific Partners CCEP and Ambev ABEV.

PepsiCo is one of the leading global food and beverage companies. The company currently has a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for PEP’s 2025 sales indicates growth of 1.8% from the previous year’s reported figures. PepsiCo delivered a trailing four-quarter average earnings surprise of 1.1%.

Coca-Cola Europacific Partners, a consumer-packaged goods company, is engaged in producing, distributing and marketing non-alcoholic ready-to-drink beverages. It presently carries a Zacks Rank #2.

The Zacks Consensus Estimate for CCEP’s 2025 sales and EPS indicates growth of 24.2% and 7.3%, respectively, from the prior-year reported levels.

Ambev is engaged in producing, distributing and selling beer, carbonated soft drinks and other non-alcoholic and non-carbonated products in many countries across the Americas. ABEV currently has a Zacks Rank #2.

The Zacks Consensus Estimate for the company’s 2025 sales implies growth of 3.7% from the previous year’s reported number. Ambev delivered a trailing four-quarter negative earnings surprise of 4.2%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite