|

|

|

|

|||||

|

|

|

Mondelez International, Inc. MDLZ posted third-quarter 2025 results, with the top line increasing year over year and surpassing the Zacks Consensus Estimate. However, the bottom line declined year over year but beat the consensus mark.

The company updated its 2025 outlook, reflecting a slightly more cautious stance than its previous guidance. It reported third-quarter results that showed the impacts of record-high cocoa costs, which peaked during the period. Shares of the company declined 6.2% after trading hours yesterday following the earnings release.

MDLZ expects some market challenges to continue, but sees early signs of cocoa price easing and a better crop outlook. Management is focused on restoring volume growth, boosting brand investments, and improving cost efficiencies, positioning the company for steady progress in 2026 and beyond.

Mondelez International, Inc. price-consensus-eps-surprise-chart | Mondelez International, Inc. Quote

Net revenues increased 5.9% year over year to $9,744 million, beating the Zacks Consensus Estimate of $9,737 million. The year-over-year increase in the top line stemmed from an increase in organic net revenues, positive foreign currency impacts, and additional revenues from the acquisition of Evirth.

Adjusted earnings were 73 cents per share, which decreased 24.2% on a constant-currency (cc) basis. The metric beat the Zacks Consensus Estimate of 72 cents. The decline was mainly caused by operating declines, partially offset by lower taxes, fewer shares outstanding, higher equity method investment earnings, and the impacts of an acquisition.

Organic net revenues grew 3.4% year over year in the third quarter. This upside was primarily fueled by an increase of 8.0 percentage points (pp) in pricing, partially offset by an unfavorable volume/mix impact of 4.6 pp. Our model estimated organic net revenue growth of 4.6%.

Revenues from emerging markets increased 9.9% to $3.88 billion, and rose 7.1% on an organic basis. Organic growth was backed by favorable pricing actions, which increased 11.8 pp and unfavorable volume/mix was down 4.7 pp.

Revenues from developed markets increased 3.3% to $5.86 billion, with an organic rise of 1.2%. This growth was primarily driven by strong pricing execution, which increased 5.7 pp, while the volume/mix effect declined 4.5 pp.

Region-wise, revenues in North America declined 0.4% year over year. The metric in Latin America; Asia, the Middle East and Africa; and Europe grew 2.8%, 9% and 10.6%, respectively. On an organic basis, revenues rose 4.7%, 5.3% and 5.1% in Latin America; Asia, the Middle East and Africa; and Europe, respectively. In contrast, organic revenues in North America fell 0.3%.

Adjusted gross profit decreased by $796 million at cc, and the adjusted gross margin declined by 1,010 basis points to 30.4%. The decrease was primarily caused by higher raw material and transportation costs and an unfavorable product mix, partially offset by increased pricing and lower manufacturing costs resulting from productivity improvements.

Mondelez’s adjusted operating income decreased by $582 million at cc, while the adjusted operating income margin declined by 690 basis points to 12%. The decrease was primarily driven by higher input cost inflation and an unfavorable product mix, partially offset by higher net pricing, lower advertising and consumer promotion costs, reduced manufacturing costs from productivity gains, and lower overhead expenses.

This Zacks Rank #4 (Sell) company ended the quarter with cash and cash equivalents of $1.37 billion, long-term debt of $17.1 billion and total equity of $26.2 billion. MDLZ provided $2.12 billion in net cash from operating activities for the three months ended Sept. 30, 2025. The adjusted free cash flow was $1.24 billion for the same period. Management expects a free cash flow of more than $3 billion for 2025.

The company returned $3.7 billion to shareholders through cash dividends and share repurchases in the first nine months of 2025.

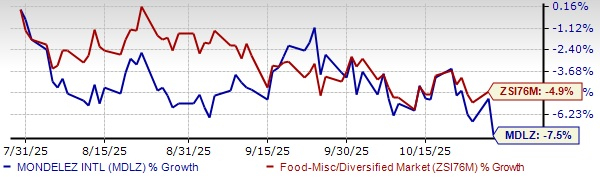

MDLZ Stock's Past 3 Months' Performance

Mondelez’s updated 2025 outlook reflects a slightly more cautious stance compared to its previous guidance. The company expects organic net revenue growth of 4% or higher, down from the earlier mentioned 5%.

Adjusted EPS is anticipated to decline 15% year over year on a cc basis, a steeper drop than the prior stated 10%. Currency translation is estimated to increase 2025 net revenue growth 0.5% and raise adjusted EPS by 5 cents.

The company’s shares have lost 7.5% in the past three months compared with the industry’s 4.9% decline.

We have highlighted three better-ranked stocks from the staple sector, namely United Natural Foods, Inc. UNFI, PepsiCo, Inc. PEP and Ollie's Bargain Outlet Holdings OLLI.

United Natural is the leading distributor of natural, organic and specialty food and non-food products, currently sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

UNFI delivered an earnings surprise of 416.2% in the trailing four quarters, on average. The Zacks Consensus Estimate for United Natural’s current fiscal-year sales and earnings indicates growth of 2.5% and 167.6%, respectively, from the year-ago reported figures.

PepsiCo is one of the leading global food and beverage companies. It currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for PepsiCo’s current financial-year sales indicates year-over-year growth of 1.8%, whereas that for EPS suggests a decline of 0.6%. PEP has a trailing four-quarter negative earnings surprise of 1.1%, on average.

Ollie's Bargain is a value retailer of brand-name merchandise at drastically reduced prices and currently carries a Zacks Rank #2. OLLI delivered a trailing four-quarter earnings surprise of 4.2%, on average.

The Zacks Consensus Estimate for Ollie's Bargain’s current fiscal-year sales and earnings indicates 16.4% and 16.5% rallies, respectively, from the year-earlier reported levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-29 |

Food Mega-Mergers Hardly Ever Work. Could McCormick-Unilever Be Different?

PEP

The Wall Street Journal

|

| Mar-26 | |

| Mar-25 | |

| Mar-25 | |

| Mar-25 | |

| Mar-24 | |

| Mar-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite