|

|

|

|

|||||

|

|

|

Kinross Gold Corporation KGC is slated to report third-quarter 2025 results after the closing bell on Nov. 4. The benefits of higher gold prices, cost management and strong production are expected to reflect on its performance.

The Zacks Consensus Estimate for third-quarter earnings has been revised upward in the past 60 days. The consensus estimate for earnings is pegged at 33 cents per share, suggesting a 37.5% year-over-year rise. The Zacks Consensus Estimate for revenues currently stands at $1.53 billion, indicating a 6.9% rise on a year-over-year basis.

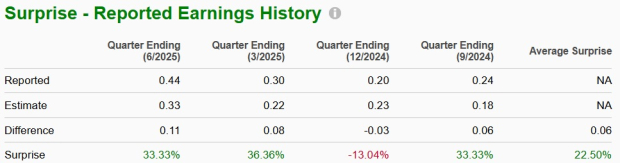

KGC beat the Zacks Consensus Estimate for earnings in three of the trailing four quarters and missed it once. In this timeframe, it delivered an earnings surprise of 22.5%, on average.

Our proven model predicts an earnings beat for KGC this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

KGC has an Earnings ESP of +13.46% and a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Higher gold prices are likely to have supported the company’s performance in the third quarter. Gold prices have racked up strong gains this year as worries over the global trade war have boosted safe-haven demand. Prices hit new highs driven by a surge in safe-haven demand amid the intense trade tussle, geopolitical tensions, a weak dollar and increased purchases by central banks.

The Federal Reserve’s interest rate reduction, hopes of more rate cuts amid concerns over the labor market, along with concerns over a protracted U.S. government shutdown and U.S.-China trade tensions, triggered the recent rally, driving prices north of $4,000 per ton for the first time. Prices of the yellow metal closed nearly 17% higher in the third quarter and have surged roughly 52% this year. Our estimate for third-quarter average realized gold price per ounce for KGC is pegged at $3,230, suggesting a 30.4% rise from the prior-year quarter.

Kinross has a strong production profile and boasts a promising pipeline of exploration and development projects. Tasiast and Paracatu, the company’s two biggest assets, remain the key contributors to cash flow generation and production. Tasiast, which remains the lowest-cost asset within its portfolio, is likely to have achieved strong performance, while Paracatu is expected to have delivered steady production in the September quarter.

The company’s cost-control actions, coupled with continued strength in gold prices, are also expected to have allowed it to maintain the strong margin performance in the third quarter. Kinross is focused on prioritizing margin improvement to drive cash flow, which should support shareholder returns.

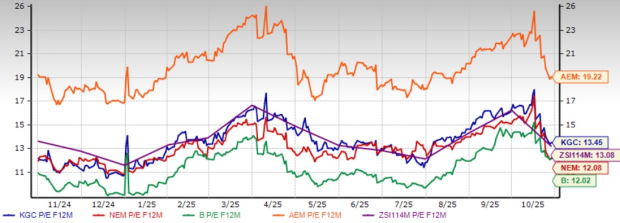

KGC’s shares have surged 129.2% in a year, topping the Zacks Mining – Gold industry’s 71.1% rise and the S&P 500’s increase of 23%. With respect to its major gold mining peers, Barrick Mining Corporation B, Newmont Corporation NEM and Agnico Eagle Mines Limited AEM have rallied 65.9%, 75.3% and 81.7%, respectively, over the same period.

From a valuation standpoint, Kinross Gold is currently trading at a forward 12-month earnings multiple of 13.45, a roughly 2.8% premium to the peer group average of 13.08X. KGC is trading at a premium to Barrick Mining and Newmont and at a discount to Agnico Eagle. Kinross Gold, Barrick Mining and Newmont have a Value Score of B, each, while Agnico Eagle has a Value Score of C.

Kinross has a strong production profile and boasts a promising pipeline of exploration and development projects. Its key development projects and exploration programs, including Great Bear in Ontario and Round Mountain Phase X in Nevada, remain on track. These projects are expected to boost production and cash flow and deliver significant value.

Kinross continues to demonstrate strong financial performance and remains committed to driving shareholder returns. KGC has a strong liquidity position and generates substantial cash flows, which allows it to finance its development projects, pay down debt and drive shareholder value. Higher gold prices should boost KGC’s profitability and drive cash flow generation.

With a strong pipeline of development projects, solid financial health, rising earnings estimates and a healthy growth trajectory, KGC stock presents an attractive investment case ahead of its earnings announcement. With compelling fundamentals and gold price tailwinds firmly remaining in place, KGC looks poised to deliver attractive returns to investors, making it a prudent choice for those looking to capitalize on favorable market conditions.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-13 | |

| Mar-13 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 |

The Winners and Losers of Monday's Selloff: Carnival, American Airlines and Exxon

NEM

The Wall Street Journal

|

| Mar-09 | |

| Mar-09 | |

| Mar-09 | |

| Mar-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite