|

|

|

|

|||||

|

|

|

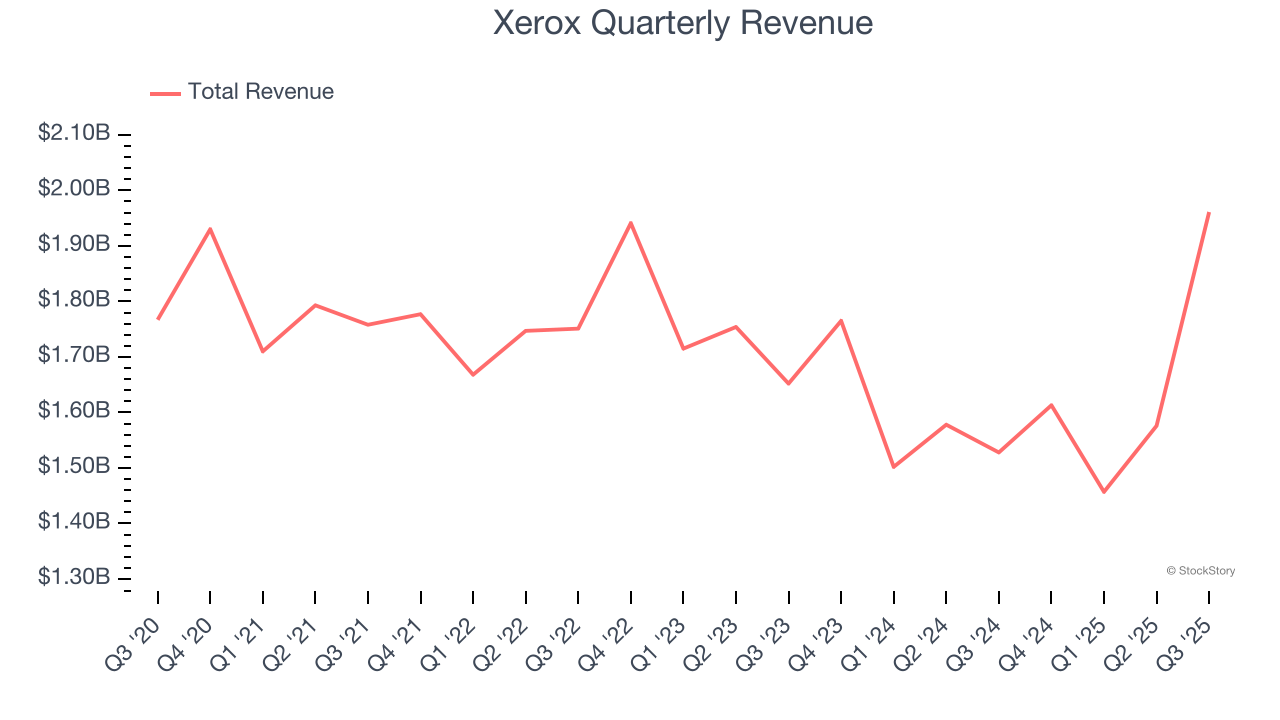

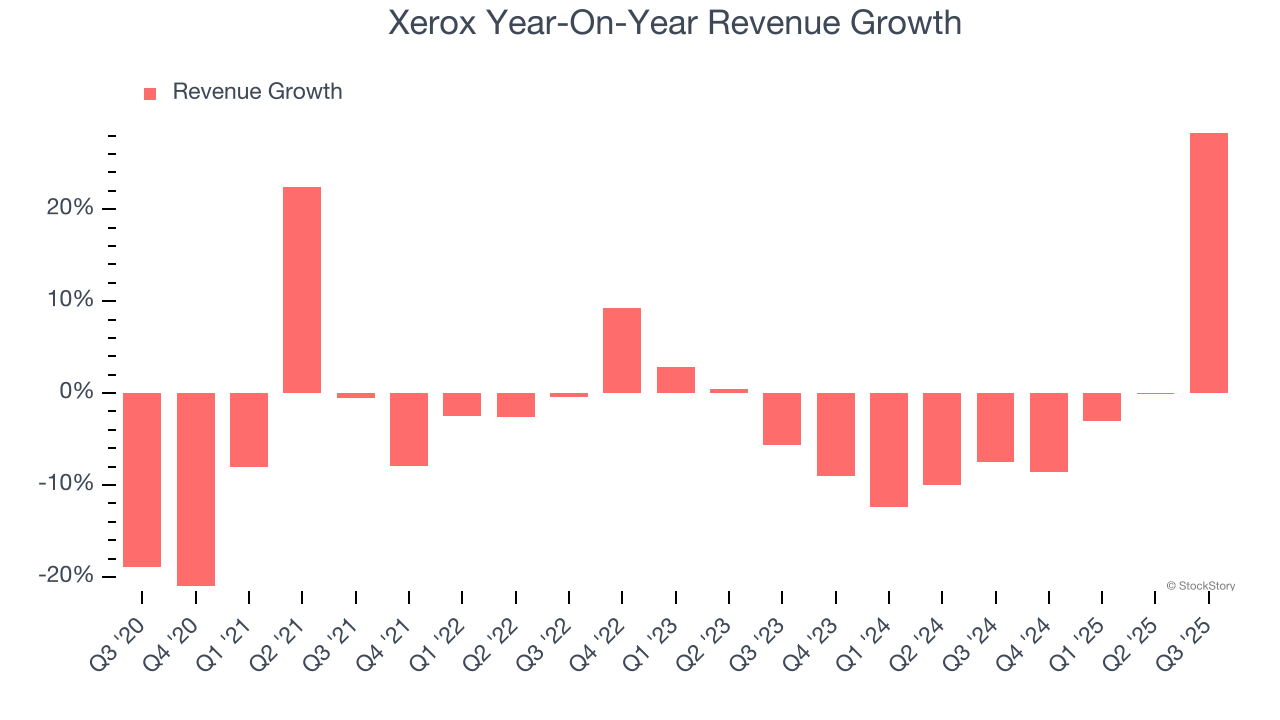

Document technology company Xerox (NASDAQ:XRX) fell short of the markets revenue expectations in Q3 CY2025, but sales rose 28.3% year on year to $1.96 billion. Its non-GAAP profit of $0.20 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Xerox? Find out by accessing our full research report, it’s free for active Edge members.

“While continued macro volatility and near-term uncertainties on government funding decisions weighed on transactional print this quarter, consistent page volume trends and strong IT Solutions momentum reinforce our confidence that Reinvention will deliver durable productivity and long‑term value. We are accelerating that work from a solid foundation established by the Lexmark acquisition and the expansion of our IT Solutions capabilities,” said Steve Bandrowczak, chief executive officer at Xerox.

Pioneering the modern office copier and inventing technologies like Ethernet and the laser printer, Xerox (NASDAQ:XRX) provides document management systems, printing technology, and workplace solutions to businesses of all sizes across the globe.

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $6.61 billion in revenue over the past 12 months, Xerox is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. For Xerox to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

As you can see below, Xerox’s demand was weak over the last five years. Its sales fell by 2.6% annually, a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Xerox’s annualized revenue declines of 3.3% over the last two years align with its five-year trend, suggesting its demand has consistently shrunk.

This quarter, Xerox generated an excellent 28.3% year-on-year revenue growth rate, but its $1.96 billion of revenue fell short of Wall Street’s high expectations.

Looking ahead, sell-side analysts expect revenue to grow 21% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will catalyze better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

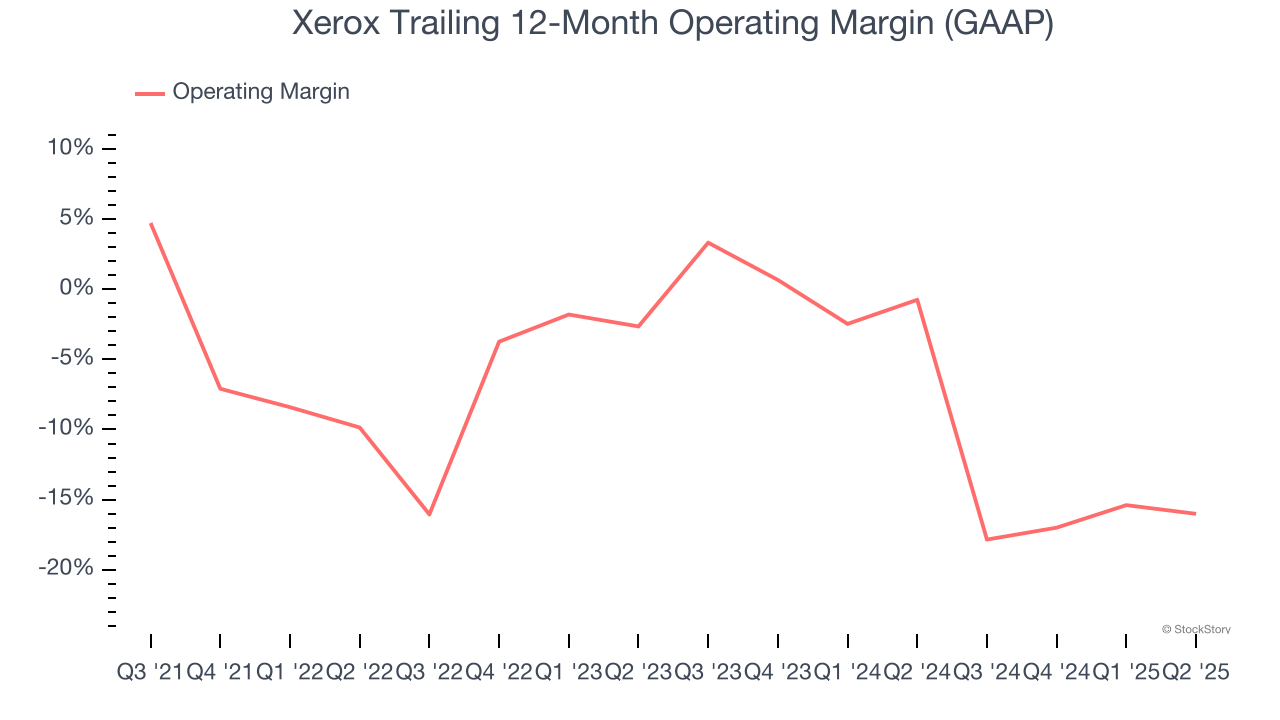

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Xerox’s high expenses have contributed to an average operating margin of negative 5% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Xerox’s operating margin decreased by 4.2 percentage points over the last five years. Xerox’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

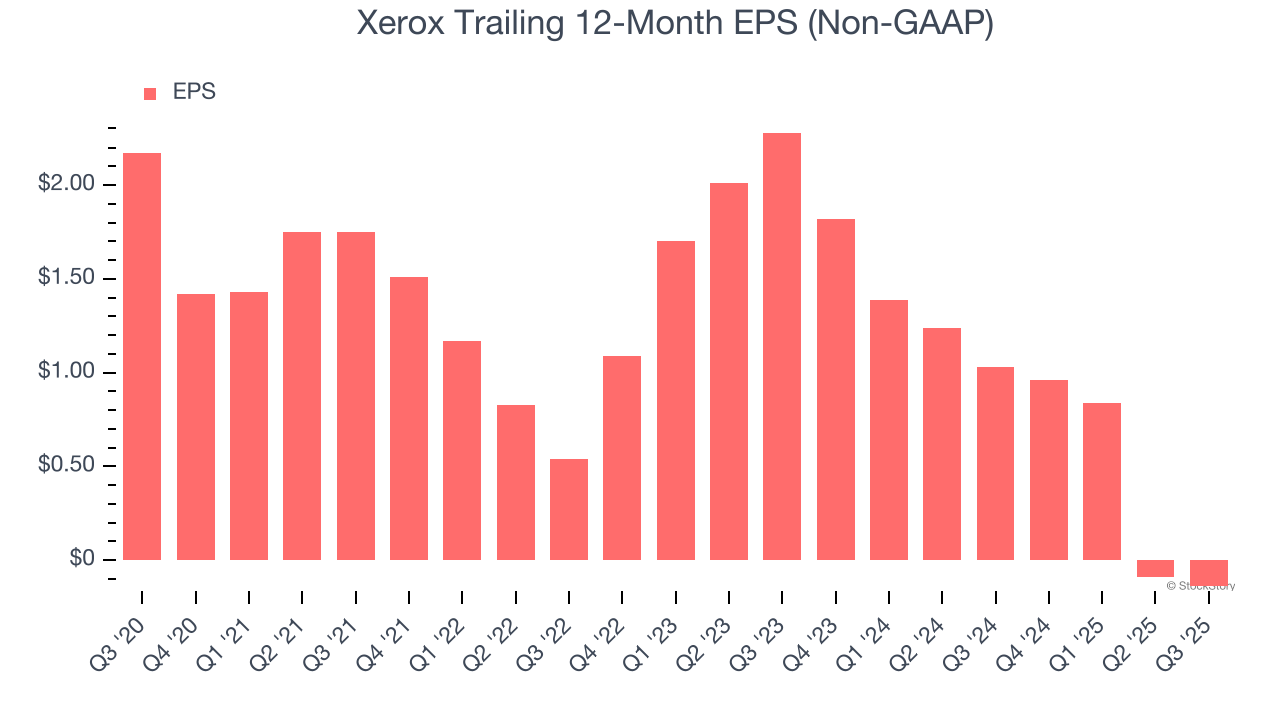

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Xerox, its EPS declined by 15.6% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

We can take a deeper look into Xerox’s earnings to better understand the drivers of its performance. As we mentioned earlier, Xerox’s operating margin declined by 4.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Xerox, its two-year annual EPS declines of 43.6% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q3, Xerox reported adjusted EPS of $0.20, down from $0.25 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Xerox’s full-year EPS of negative $0.14 will flip to positive $1.54.

It was good to see Xerox beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 13.2% to $2.97 immediately following the results.

Big picture, is Xerox a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Aug-05 | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-24 | |

| Jul-16 | |

| Jul-15 | |

| May-20 | |

| May-15 | |

| May-01 | |

| Apr-30 | |

| Apr-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite