|

|

|

|

|||||

|

|

|

Merck MRK reported third-quarter 2025 adjusted earnings per share (EPS) of $2.58, which beat the Zacks Consensus Estimate of $2.36. Earnings increased 64% year over year on a reported basis and 65% excluding foreign exchange (Fx).

Revenues in the third quarter increased 4% year over year on a reported basis and 3% excluding Fx to $17.28 billion. Sales beat the Zacks Consensus Estimate of $17.06 billion.

All sales growth numbers discussed below are on a year-over-year basis and exclude Fx impact.

Merck’s flagship product, Keytruda, generated sales of $8.14 billion in the quarter, up 8%. Sales of the drug benefited from rapid uptake across earlier-stage indications and continued strong momentum in metastatic indications.

Keytruda sales, however, missed the Zacks Consensus Estimate of $8.40 billion and our model estimate of $8.51 billion.

Alliance revenues from Lynparza and Lenvima also aided oncology sales in the third quarter. Merck has a deal with British pharma giant AstraZeneca AZN to co-develop and commercialize PARP inhibitor Lynparza and a similar one with Japan’s Eisai for its tyrosine kinase inhibitor, Lenvima.

Alliance revenues from AZN-partnered Lynparza increased 12% to $379 million in the quarter, driven by higher demand globally. Lenvima alliance revenues totaled $258 million, up 2%.

Welireg recorded sales of $196 million, up 41%. The drug’s sales benefited from higher demand in the United States as well as early launch uptake in certain European markets.

Sales Performance of MRK's Other Key Products

In vaccines, sales of HPV vaccines — Gardasil and Gardasil 9 — plunged 25% to $1.75 billion due to lower demand in China as well as in Japan. Gardasil/Gardasil 9 sales were almost in line with the Zacks Consensus Estimate and beat our estimate of $1.70 billion.

Proquad, M-M-R II and Varivax vaccines recorded combined sales of $684 million, down 3%.

Capvaxive, Merck’s recently launched pneumococcal 21-valent conjugate vaccine, generated sales worth $244 million compared with $129 million reported in the previous quarter.

In the hospital specialty portfolio, neuromuscular blockade medicine, Bridion injection, generated sales of $439 million in the quarter, up 4%. While the drug’s sales benefited from higher demand in the United States, the gains were offset by generic competition in certain international markets.

In Diabetes, Januvia/Janumet franchise sales increased 29% year over year to $624 million. Sales of the drug were driven by higher net pricing in the United States, offset by lower demand in China and generic competition in most international markets.

New PAH drug Winrevair generated sales of $360 million, increasing 141% on a year-over-year basis and 7.1% on a sequential basis, reflecting continued strong uptake.

The segment generated revenues of $1.62 billion, up 9% year over year on a reported basis and 7% excluding Fx. This growth was driven by higher demand for livestock products. Sales from this segment beat the Zacks Consensus Estimate as well as our model estimate of $1.56 billion.

Merck narrowed its sales guidance for the year. The company now expects revenues to be in the range of $64.5-$65.0 billion, compared with the previous expectation of $64.3-$65.3 billion. The updated guidance includes a revised negative impact on sales from Fx of around 0.5%.

Merck increased its adjusted EPS guidance for 2025. The company now expects adjusted EPS to be between $8.93 and $8.98 versus the prior estimated range of $8.87 and $8.97. This guidance range includes a revised negative impact of Fx of around 15 cents per share.

The updated EPS outlook includes new factors such as benefits from a revised AstraZeneca deal for Koselugo, better operations with a lower tax rate and reduced tariff costs. These gains are partly offset by costs from acquiring Verona Pharma and negative effects from foreign exchange.

Merck closed the acquisition of Verona Pharma earlier this month, which added the latter’s chronic obstructive pulmonary disease or COPD drug, Ohtuvayre, to its portfolio. The addition of Ohtuvayre strengthens Merck’s cardio-pulmonary pipeline and portfolio as the drug’s differentiated profile provides a significant edge over its competitors.

The revised guidance included a one-time charge of $300 million related to a payment made to LaNova for the technology transfer for MK-2010, which will impact EPS by almost 16 cents in aggregate.

The adjusted gross margin is expected to be around 82%, which is unchanged from the previous expectation.

Adjusted operating costs are now expected to be in the range of $25.9 to $26.4 billion (previously: $25.6 to $26.4 billion). The adjusted tax rate is now expected to be around 14% to 15% versus the prior guidance of 15% to 16%.

Merck & Co., Inc. price-consensus-eps-surprise-chart | Merck & Co., Inc. Quote

Merck delivered encouraging third-quarter results, with both earnings and sales beating estimates. Keytruda's soft sales performance raised some eyebrows. Merck defended that it was due to channel movements and not a drop in underlying demand. Robust sales of Januvia/Janumet, along with solid contributions from newer launches like Capvaxive and Winrevair, also aided the top line.

Despite the third-quarter beat, Merck’s shares were down more than 2% in pre-market trading on Thursday due to the weaker-than-expected sales performance of Keytruda, as well as the narrowed total sales guidance.

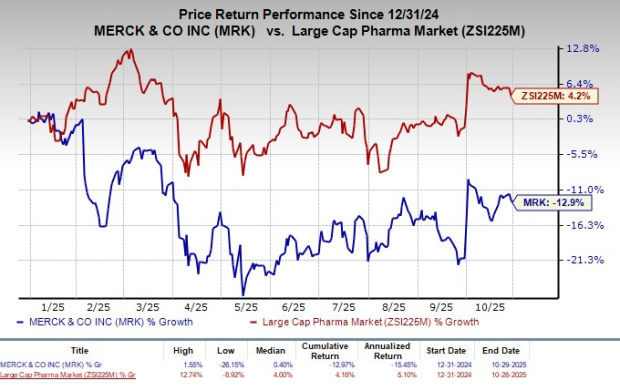

Year to date, shares of Merck have lost 12.9% against the industry’s increase of 4.2%.

Merck currently has a Zacks Rank #4 (Sell).

Some better-ranked stocks in the biotech sector are ANI Pharmaceuticals ANIP and CorMedix CRMD, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

In the past 60 days, estimates for ANI Pharmaceuticals’ earnings per share have increased from $7.25 to $7.29 for 2025. During the same time, earnings per share estimates for 2026 have increased from $7.74 to $7.81. Year to date, shares of ANIP have surged 66.8%.

ANI Pharmaceuticals' earnings beat estimates in each of the trailing four quarters, the average surprise being 22.66%.

In the past 60 days, estimates for CorMedix’s earnings per share have increased from $1.22 to $1.85 for 2025. During the same time, earnings per share estimates for 2026 have increased from $2.12 to $2.49. Year to date, shares of CRMD have rallied 39.6%.

CorMedix’s earnings beat estimates in each of the trailing four quarters, the average surprise being 34.85%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 min | |

| Mar-16 | |

| Mar-16 | |

| Mar-16 | |

| Mar-15 | |

| Mar-13 | |

| Mar-12 | |

| Mar-12 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite