|

|

|

|

|||||

|

|

|

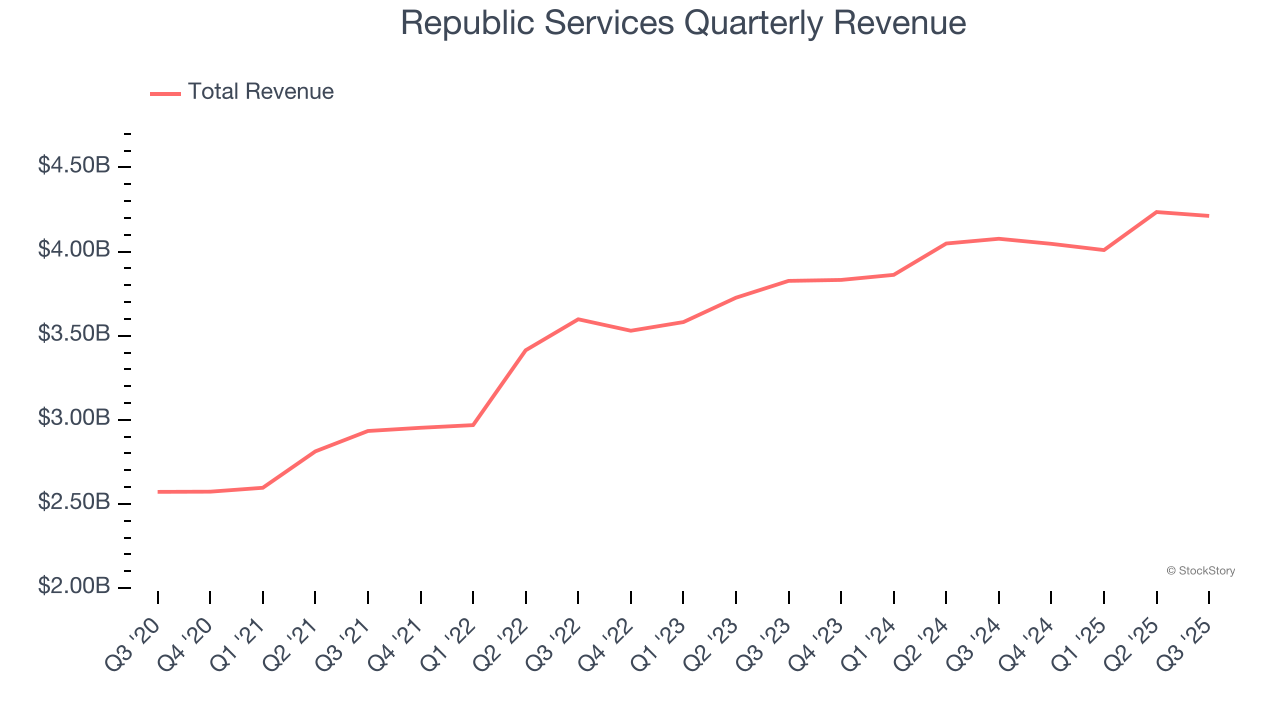

Waste management company Republic Services (NYSE:RSG) fell short of the markets revenue expectations in Q3 CY2025 as sales rose 3.3% year on year to $4.21 billion. Its non-GAAP profit of $1.90 per share was 6.5% above analysts’ consensus estimates.

Is now the time to buy Republic Services? Find out by accessing our full research report, it’s free for active Edge members.

"We delivered strong third-quarter results as we continue to execute our strategy for sustainable, profitable growth," said Jon Vander Ark, president and chief executive officer.

Processing several million tons of recyclables annually, Republic (NYSE:RSG) provides waste management services for residences, companies, and municipalities.

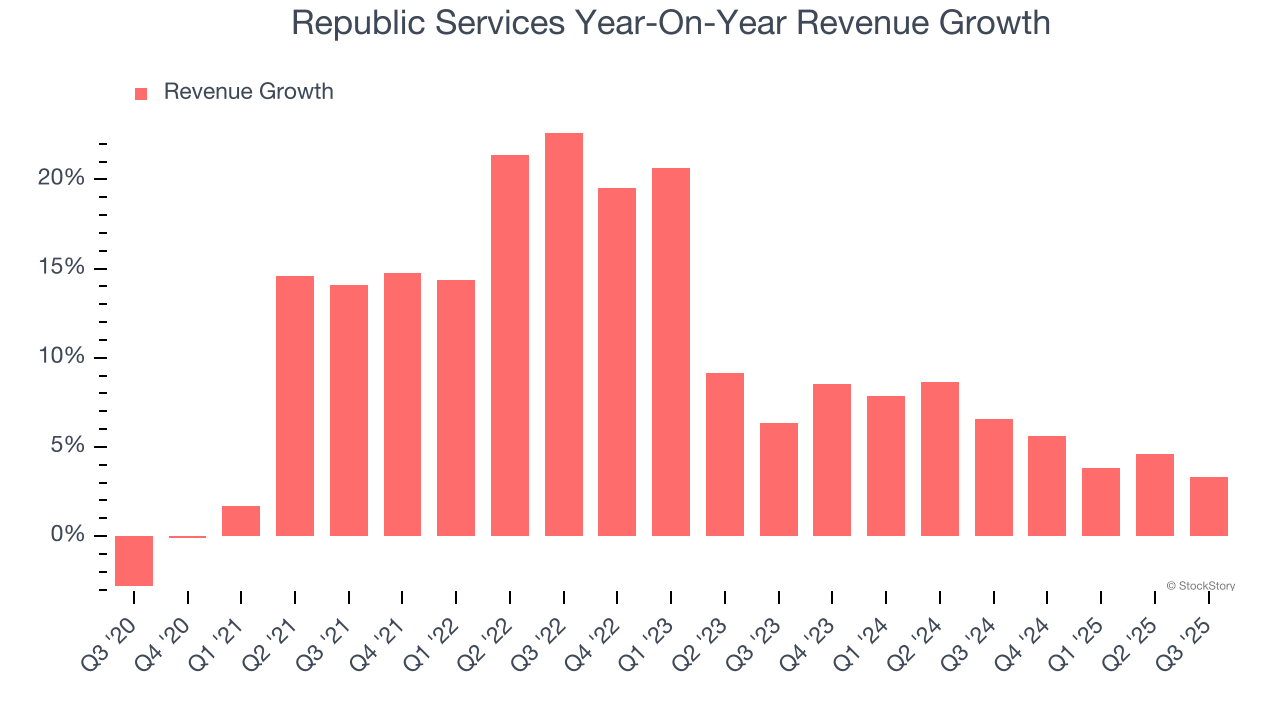

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Republic Services’s sales grew at a solid 10.2% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Republic Services’s recent performance shows its demand has slowed as its annualized revenue growth of 6.1% over the last two years was below its five-year trend.

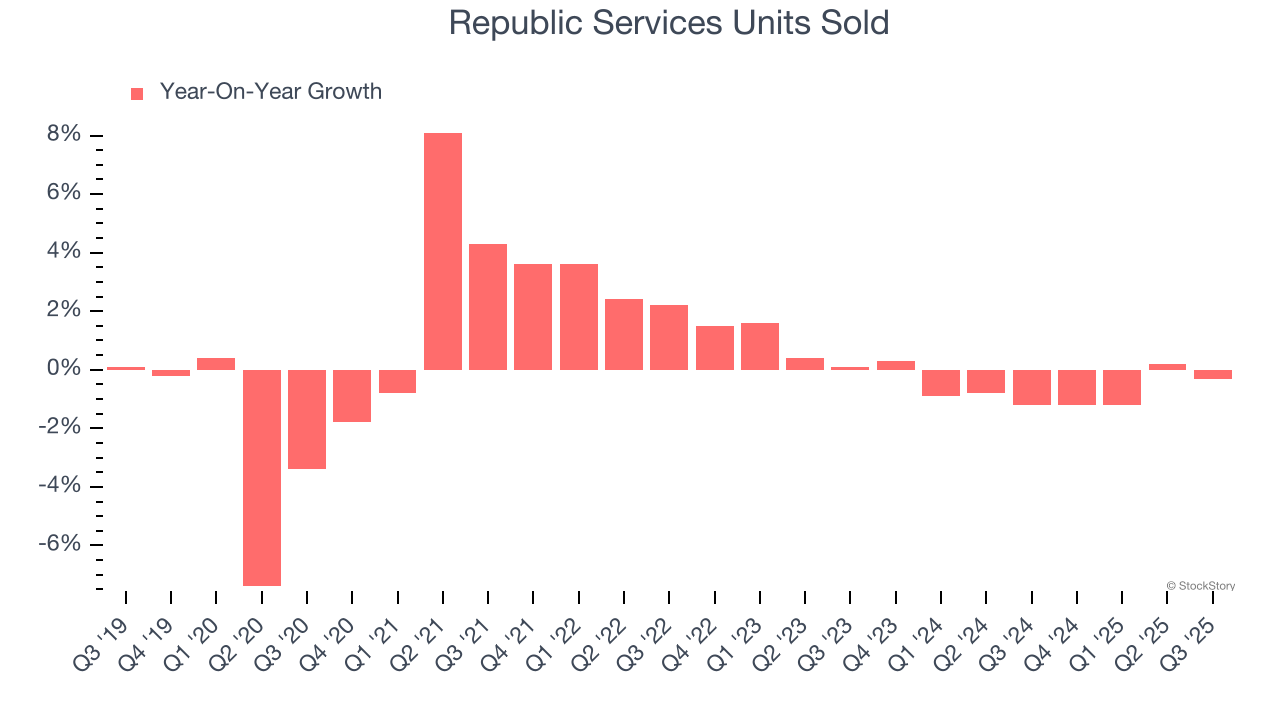

We can dig further into the company’s revenue dynamics by analyzing its number of units sold. Over the last two years, Republic Services’s units sold were flat. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Republic Services’s revenue grew by 3.3% year on year to $4.21 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

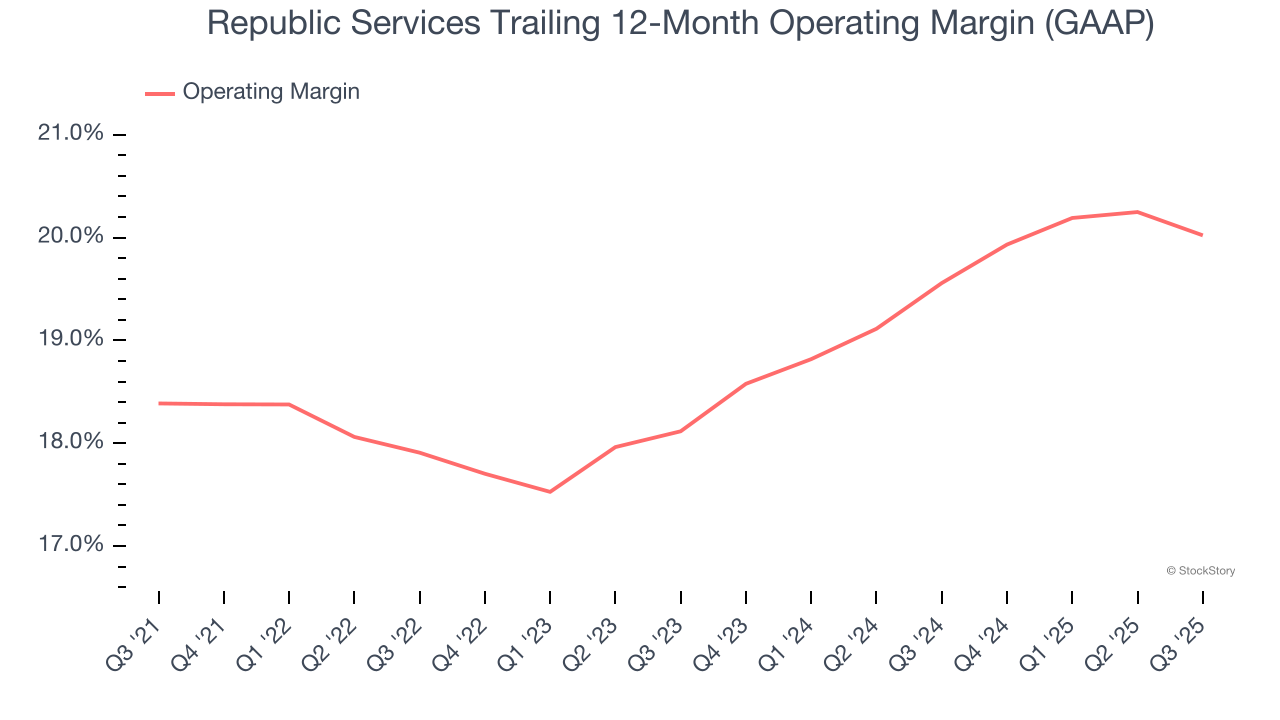

Republic Services has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 18.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Republic Services’s operating margin rose by 1.6 percentage points over the last five years, as its sales growth gave it operating leverage. Its expansion shows it’s one of the better Waste Management companies as most peers saw their margins plummet.

In Q3, Republic Services generated an operating margin profit margin of 19.8%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

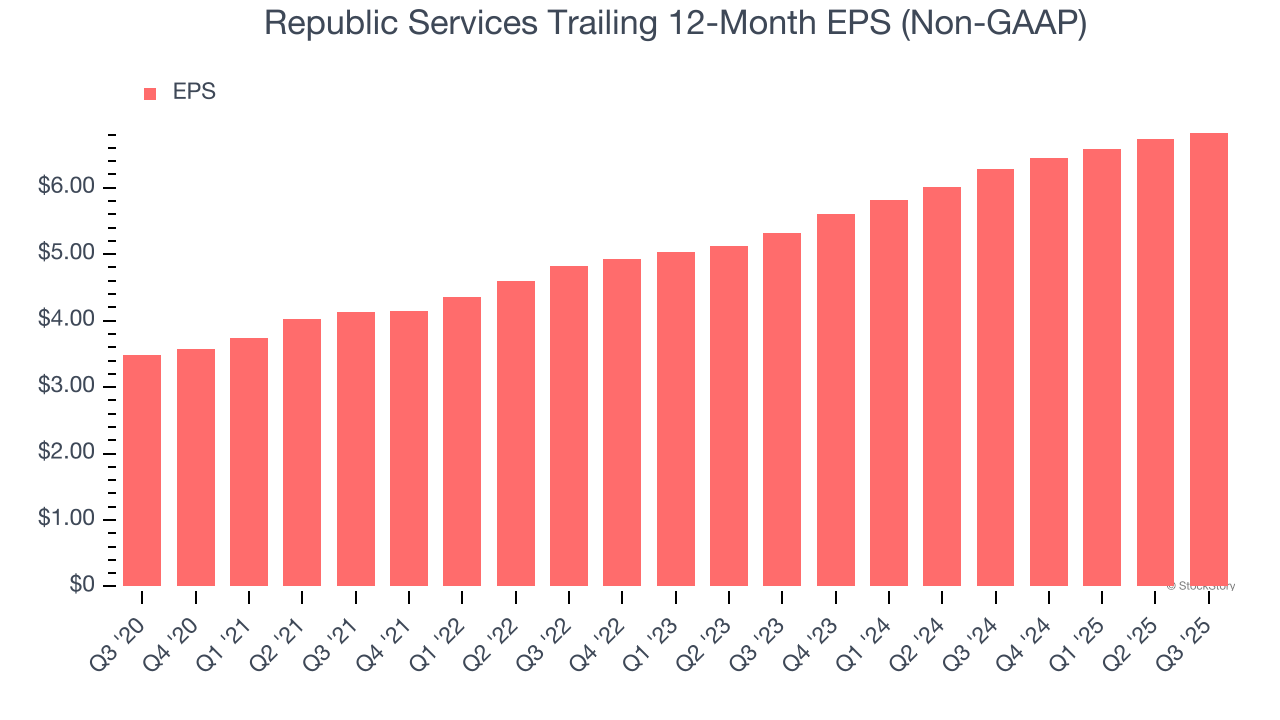

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Republic Services’s EPS grew at a remarkable 14.4% compounded annual growth rate over the last five years, higher than its 10.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

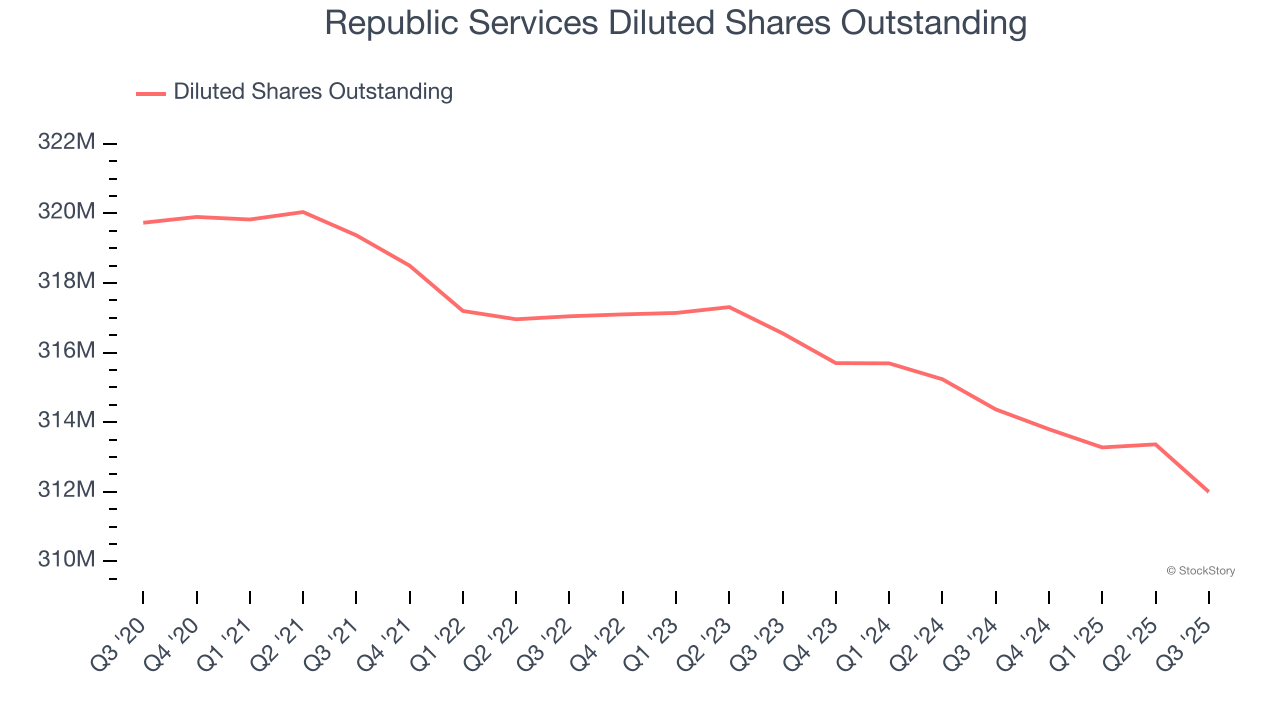

Diving into Republic Services’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Republic Services’s operating margin was flat this quarter but expanded by 1.6 percentage points over the last five years. On top of that, its share count shrank by 2.4%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Republic Services, its two-year annual EPS growth of 13.3% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q3, Republic Services reported adjusted EPS of $1.90, up from $1.81 in the same quarter last year. This print beat analysts’ estimates by 6.5%. Over the next 12 months, Wall Street expects Republic Services’s full-year EPS of $6.83 to grow 6.1%.

It was encouraging to see Republic Services beat analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its sales volume missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $208.80 immediately after reporting.

Republic Services may have had a tough quarter, but does that actually create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jun-15 | |

| Jun-03 | |

| May-20 | |

| May-20 | |

| May-12 | |

| May-08 | |

| May-08 | |

| May-07 | |

| May-07 | |

| Apr-30 | |

| Apr-22 | |

| Apr-16 | |

| Apr-10 | |

| Apr-08 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite