|

|

|

|

|||||

|

|

|

Shopify SHOP is scheduled to report its third-quarter 2025 results on Nov. 4.

For the to-be-reported quarter, Shopify expects revenues to grow in the mid-to-high twenties percentage rate on a year-over-year basis.

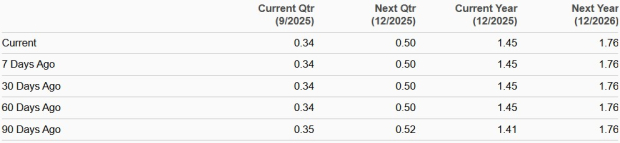

The Zacks Consensus Estimate for revenues is currently pegged at $2.75 billion, suggesting growth of 27.3% from the year-ago quarter’s reported figure.

The consensus mark for earnings is pegged at 34 cents per share, unchanged over the past 30 days and indicating a 5.6% decline from the figure reported in the year-ago quarter.

SHOP’s earnings beat the Zacks Consensus Estimate in two of the trailing four quarters, in line in one and missing in the remaining one, the earnings surprise being 13.62%, on average.

Shopify Inc. price-eps-surprise | Shopify Inc. Quote

Let’s see how things have shaped up prior to this announcement.

Shopify is benefiting from strong growth in its merchant base, a trend that will likely be reflected in third-quarter results. Gross Merchandise Volume (GMV) in the second quarter of 2025 was $87.84 billion, which increased 30.6% year over year. Same-store sales growth from existing merchants, a higher number of merchants on SHOP’s platform and strong international growth drove GMV. These same factors are expected to have driven GMV growth in the to-be-reported quarter as well. The Zacks Consensus Estimate for third-quarter 2025 GMV is currently pegged at $88 billion, indicating 25.7% year-over-year growth.

New merchant-friendly tools, such as Shop Minis, Shop Cash and Sign in with Shop, as well as Shop Pay solutions, are helping SHOP win merchants regularly. These factors are expected to have benefited Merchant Solutions’ revenues in the to-be-reported quarter. The consensus mark for Merchant Solutions revenues is currently pegged at $2.04 billion, suggesting 54.8% growth from the figure reported in the year-ago quarter. The Zacks Consensus Estimate for third-quarter 2025 Subscription revenues is currently pegged at $705 million, indicating 15.6% growth from the figure reported in the year-ago quarter.

Shopify’s growing international footprint has been a key catalyst. International GMV grew 42% year over year in the second quarter of 2025, with Europe leading the charge (currently one-fourth of Shopify’s business). Shopify Capital is now available in Germany and the Netherlands, providing more merchants with access to growth funding. The company also launched Shop Pay Installments in Canada.

Moreover, a strong cash balance, $5.82 billion as of June 30, and improving free cash flow margin (up 100 basis points sequentially in the second quarter of 2025) reflect strong liquidity. Shopify expects the free cash flow margin to be in the mid to high-teens for the third quarter of 2025.

SHOP shares have appreciated 63.3% year to date (YTD), outperforming the Zacks Computer & Technology sector’s rise of 30.9% and the Zacks Internet Services industry’s return of 43.9%.

Shopify has outperformed peers including Amazon AMZN, Wix.com WIX and Commerce.com CMRC. YTD, Amazon shares have returned 13.7% while Wix.com and Commerce.com shares dropped 26% and 37%, respectively.

However, the Value Score of F suggests a stretched valuation for Shopify at this moment.

SHOP stock is trading at a premium with a forward 12-month price/sales of 17.05X compared with the industry’s 7.06X, Amazon’s 3.08X, Wix.com’s 3.44X and Commerce.com’s 1.02X.

Shopify’s long-term prospects are strong, given its growing merchant base and expanding partner base. Shopify’s rich partner, which includes Microsoft, TikTok, Roblox, PayPal, Snap, Pinterest, Criteo, IBM, Cognizant, Google Cloud and Adayen, has further expanded its merchant base.

SHOP has diversified its payment product offerings through an expanded partnership with PayPal. Shopify’s partnership with Microsoft involves the integration of Shopify’s Checkout Kit into Microsoft’s Copilot, a major player in the AI space. This integration allows merchants to embed their checkout process directly within Microsoft’s AI-driven platform, enabling seamless shopping experiences for users.

The company’s investment in AI-driven tools, such as AI store builder, Catalog, Universal Cart and Sidekick, is helping merchants improve customer engagement and streamline operations. Infusion of AI into Shop search and the home feed is helping buyers see the right products at the right time, driving higher engagement and conversion. This bodes well for merchant base expansion and Shopify’s prospects.

Shopify currently sports a Zacks Rank #1 (Strong Buy), which implies that investors should start accumulating the stock ahead of third-quarter earnings. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN

Investor's Business Daily

|

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite