|

|

|

|

|||||

|

|

|

While the S&P 500 is up 21% since May 2025, Wabtec (currently trading at $204 per share) has lagged behind, posting a return of 6.9%. This might have investors contemplating their next move.

Is WAB a buy right now? Or is its underperformance reflective of its business quality?

Also known as Wabtec, Westinghouse Air Brake Technologies (NYSE:WAB) provides equipment, systems, and related software for the railway industry.

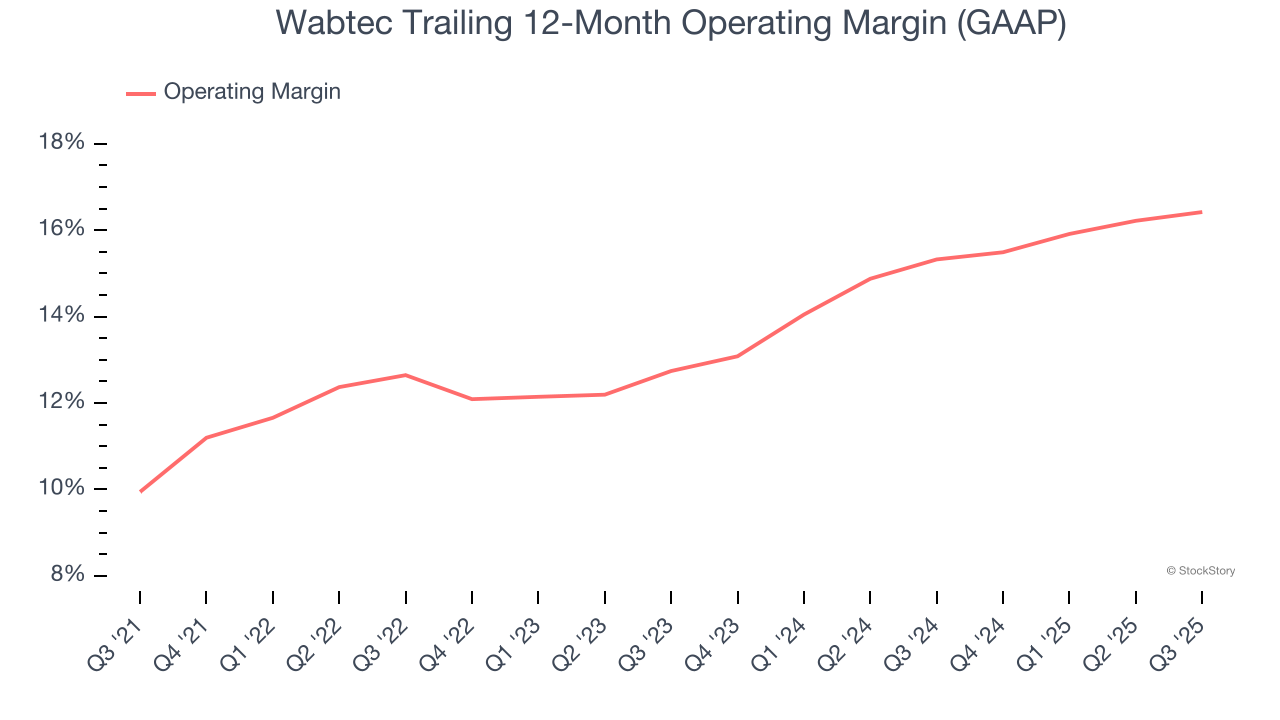

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Analyzing the trend in its profitability, Wabtec’s operating margin rose by 6.5 percentage points over the last five years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 16.4%.

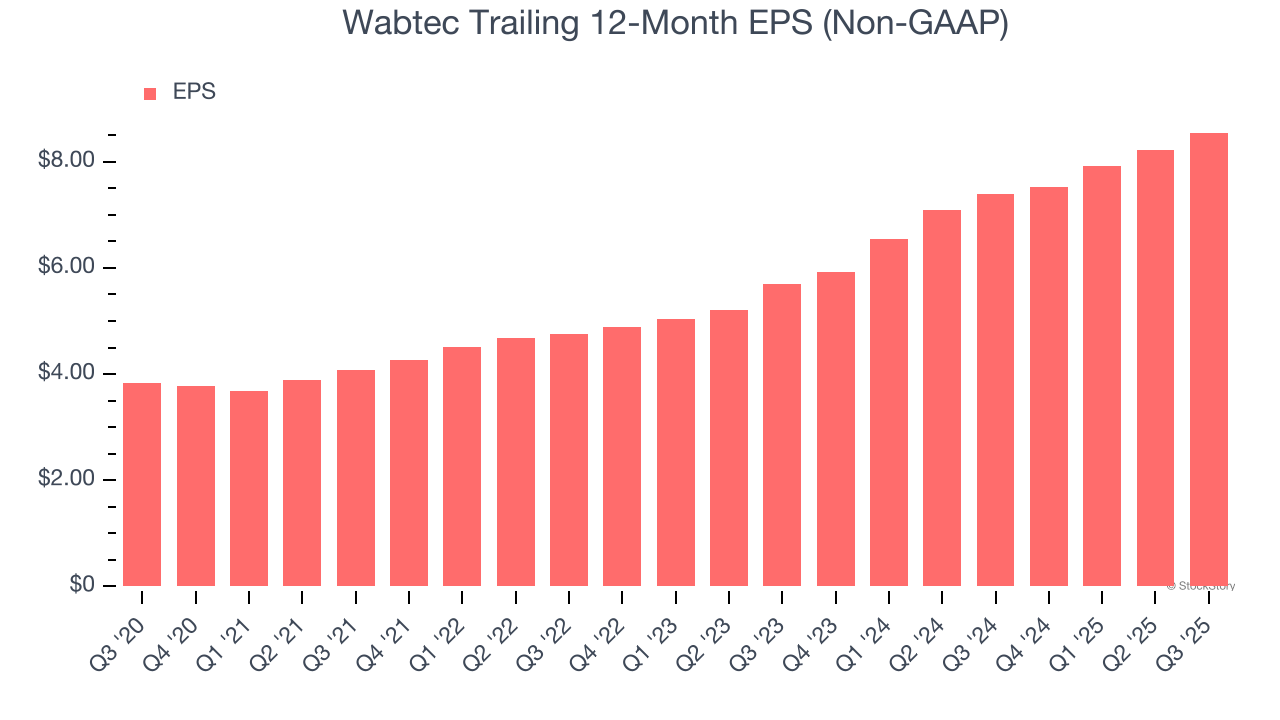

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Wabtec’s EPS grew at a spectacular 17.4% compounded annual growth rate over the last five years, higher than its 6.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

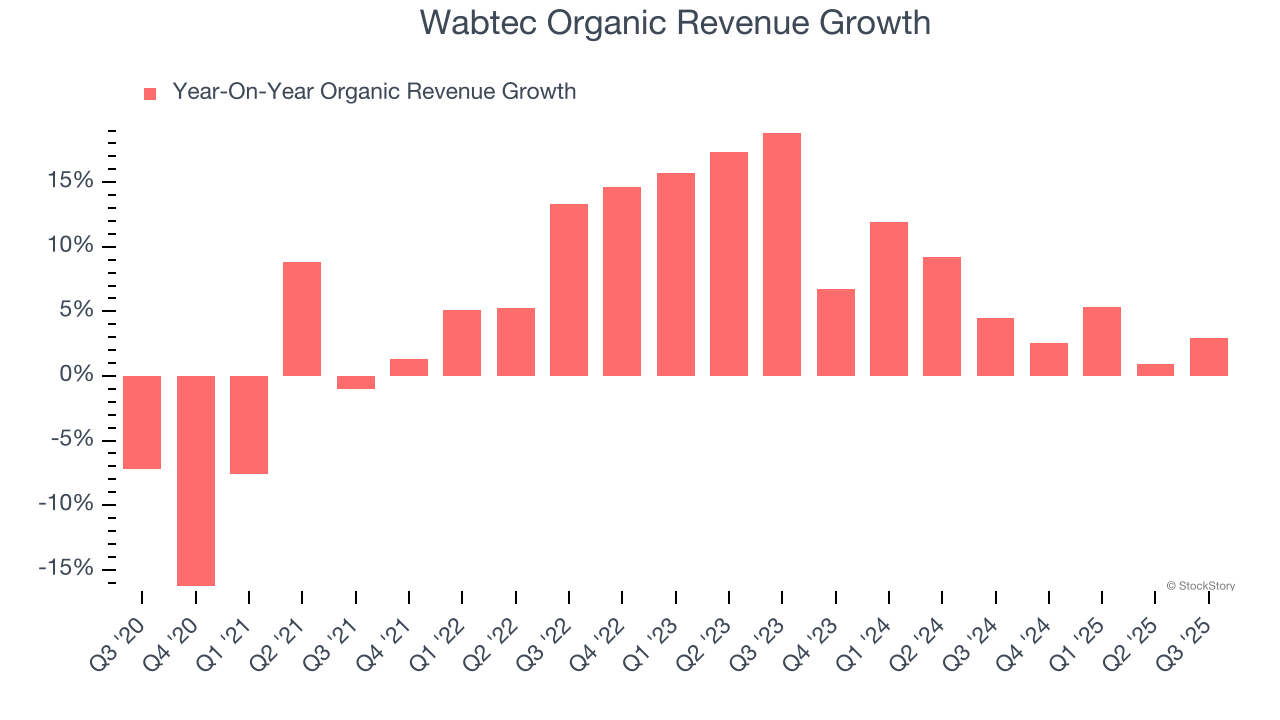

Investors interested in Heavy Transportation Equipment companies should track organic revenue in addition to reported revenue. This metric gives visibility into Wabtec’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Wabtec’s organic revenue averaged 5.5% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Wabtec’s merits more than compensate for its flaws. With its shares underperforming the market lately, the stock trades at 20.8× forward P/E (or $204 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free for active Edge members.

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jun-24 | |

| May-13 | |

| May-12 | |

| May-02 |

Broadcom, Viking, Rio Tinto Lead Five Stocks Near Buy Points In Strong Market

WAB

Investor's Business Daily

|

| Apr-27 | |

| Apr-23 | |

| Apr-22 | |

| Apr-22 | |

| Apr-22 | |

| Apr-17 | |

| Apr-02 | |

| Mar-30 | |

| Mar-18 | |

| Mar-12 | |

| Mar-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite