|

|

|

|

|||||

|

|

|

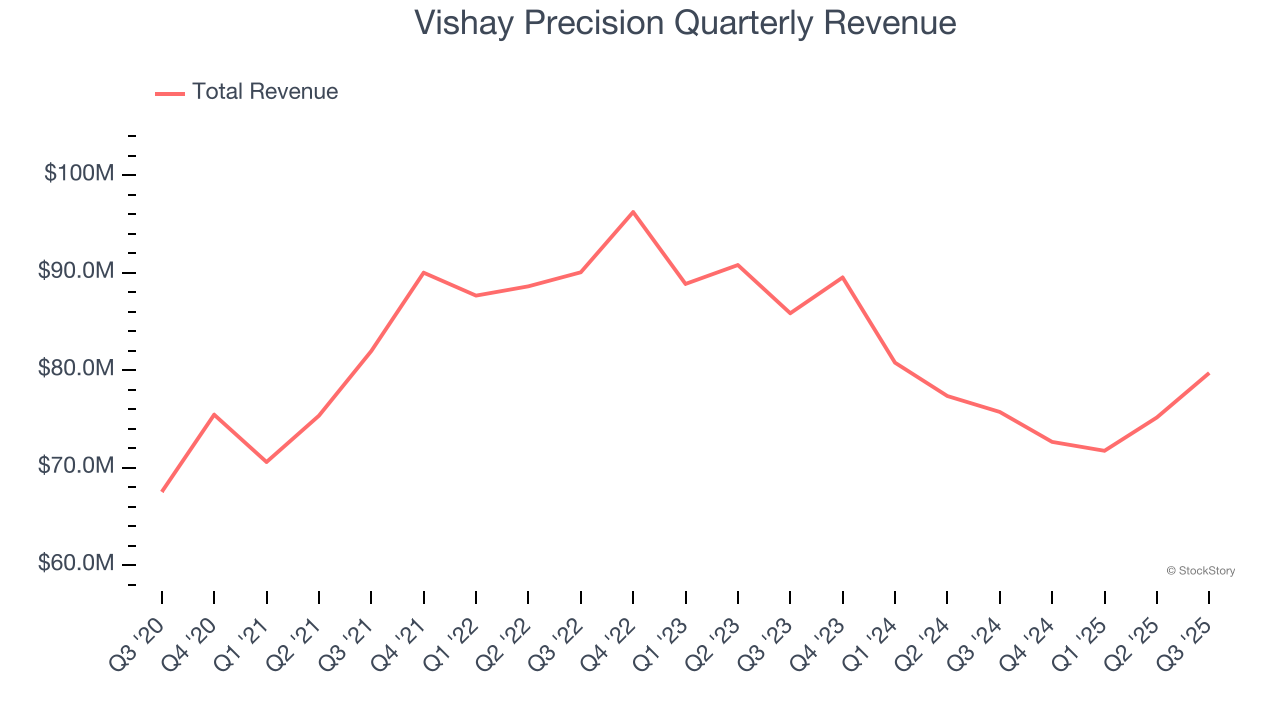

Precision measurement and sensing technologies provider Vishay Precision (NYSE:VPG) reported Q3 CY2025 results beating Wall Street’s revenue expectations, with sales up 5.3% year on year to $79.73 million. The company expects next quarter’s revenue to be around $78 million, close to analysts’ estimates. Its non-GAAP profit of $0.26 per share was 30% above analysts’ consensus estimates.

Is now the time to buy Vishay Precision? Find out by accessing our full research report, it’s free for active Edge members.

Ziv Shoshani, Chief Executive Officer of VPG, commented, “We achieved a solid quarter for VPG, as third-quarter sales grew 6.1% sequentially and were up 5.3% from the prior year. Total orders of $79.7 million were even with second-quarter levels, as strength in our Sensors segment offset lower orders in Weighing Solutions and Measurement Systems. This resulted in a book-to-bill of 1.00, the fourth consecutive quarter of book-to-bill ratios of 1.00 or better, as our Sensors and Measurement Systems reporting segments recorded book-to-bill ratios of 1.07 and 1.04, respectively. We continue to be encouraged by our business development initiatives, which include our opportunity in humanoid robots.”

Emerging from Vishay Intertechnology in 2010, Vishay Precision (NYSE:VPG) operates as a global provider of precision measurement and sensing technologies.

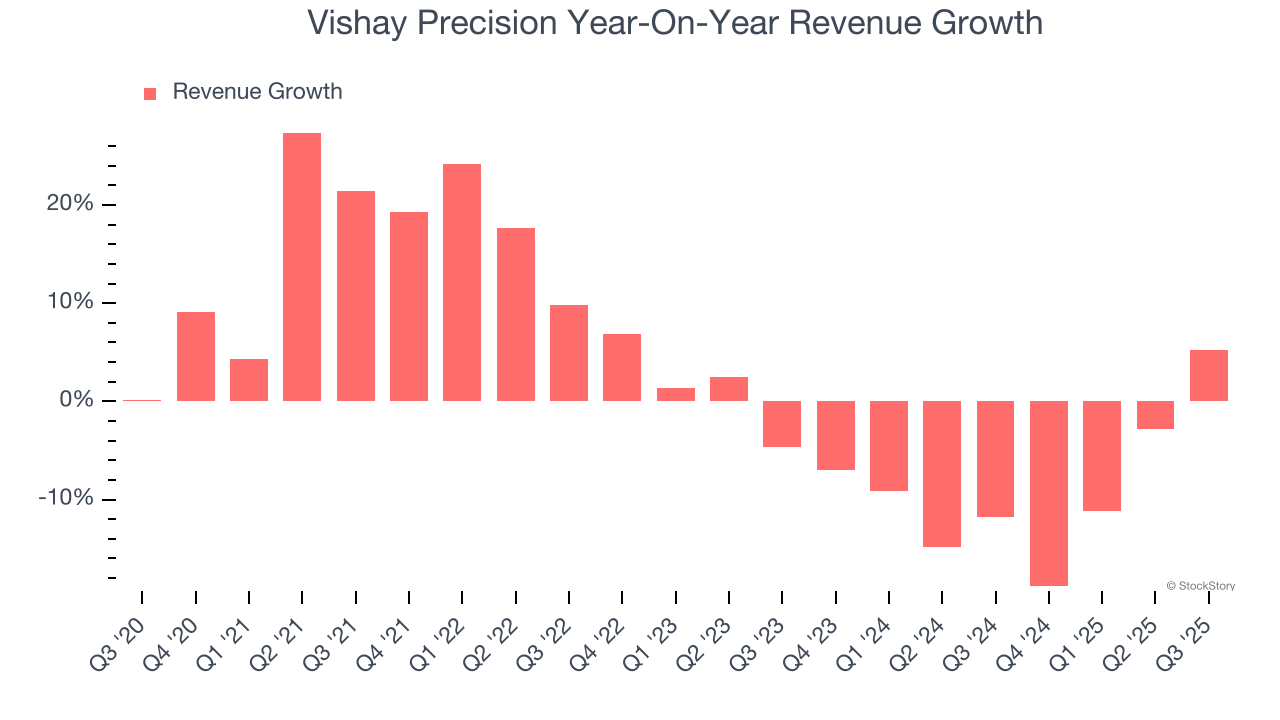

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Vishay Precision grew its sales at a sluggish 2.6% compounded annual growth rate. This fell short of our benchmarks and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Vishay Precision’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 9% annually. Vishay Precision isn’t alone in its struggles as the Electronic Components industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, Vishay Precision reported year-on-year revenue growth of 5.3%, and its $79.73 million of revenue exceeded Wall Street’s estimates by 4%. Company management is currently guiding for a 7.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months. Although this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

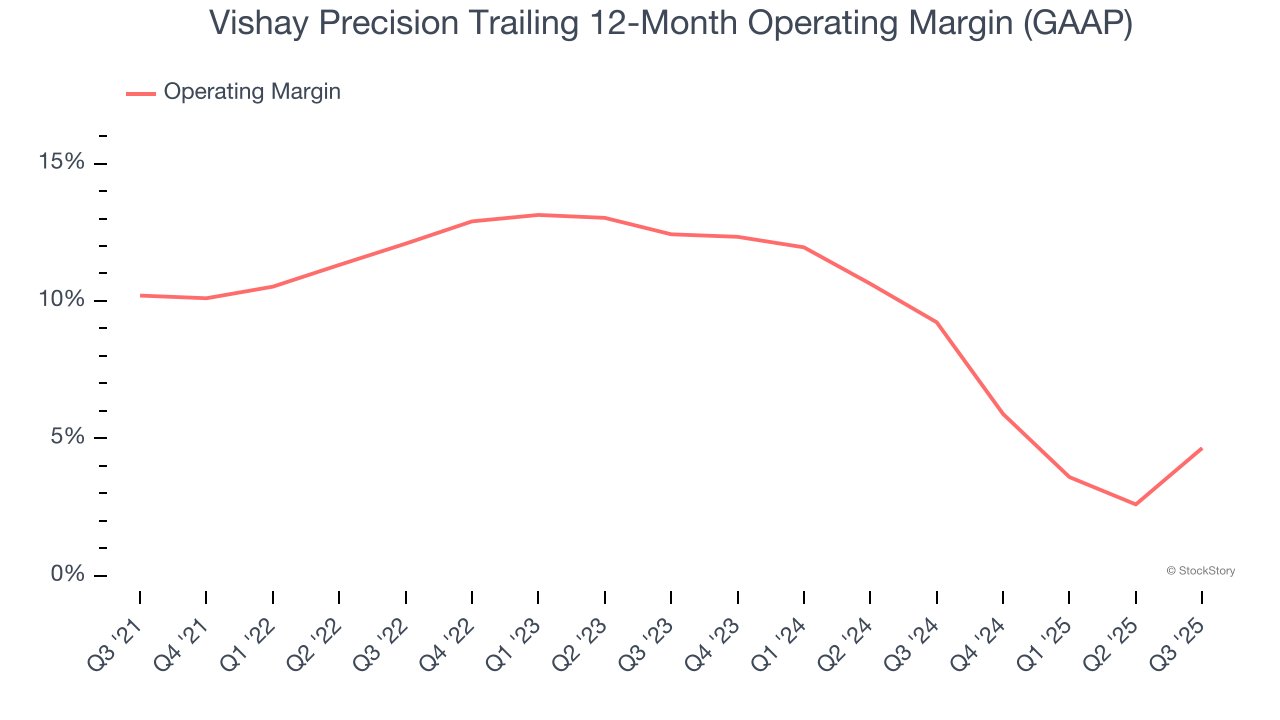

Vishay Precision has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 9.9%, higher than the broader industrials sector.

Analyzing the trend in its profitability, Vishay Precision’s operating margin decreased by 5.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q3, Vishay Precision generated an operating margin profit margin of 12.7%, up 7.6 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

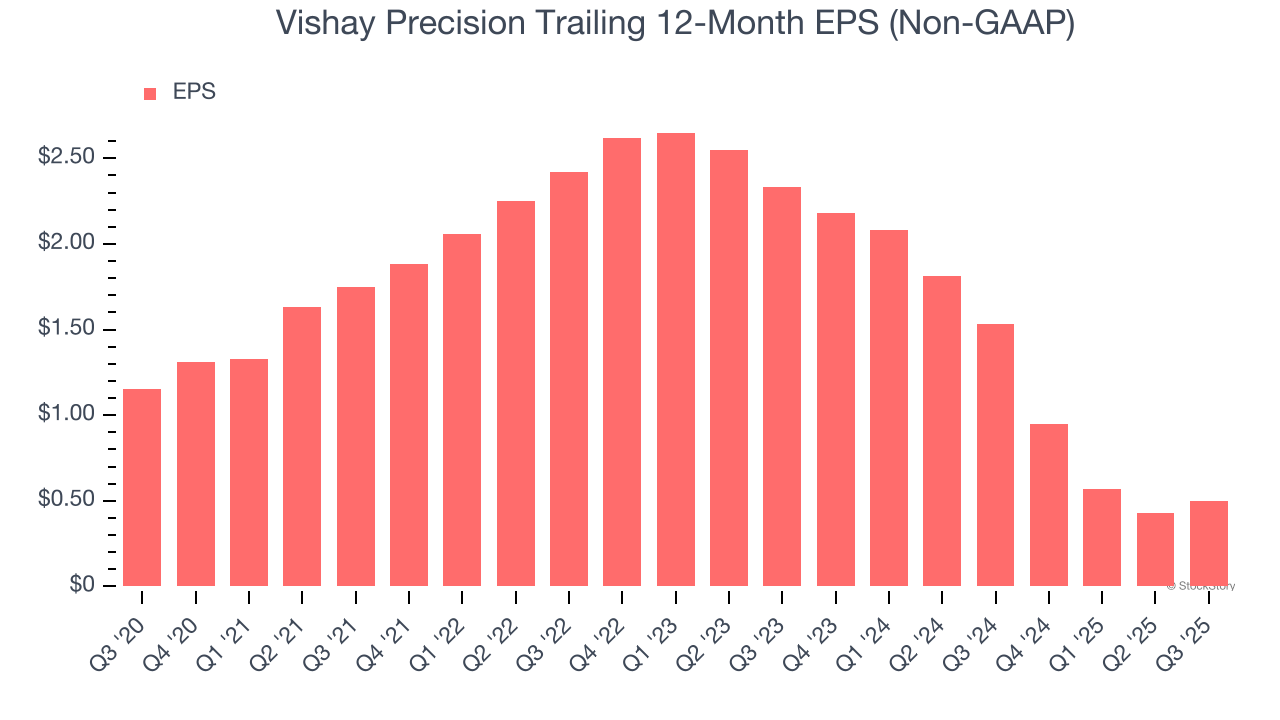

Sadly for Vishay Precision, its EPS declined by 15.3% annually over the last five years while its revenue grew by 2.6%. We can see the difference stemmed from higher interest expenses or taxes as the company actually improved its operating margin and repurchased its shares during this time.

We can take a deeper look into Vishay Precision’s earnings to better understand the drivers of its performance. As we mentioned earlier, Vishay Precision’s operating margin expanded this quarter but declined by 5.5 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Vishay Precision, its two-year annual EPS declines of 53.7% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q3, Vishay Precision reported adjusted EPS of $0.26, up from $0.19 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Vishay Precision’s full-year EPS of $0.50 to grow 132%.

It was good to see Vishay Precision beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $38.01 immediately following the results.

Is Vishay Precision an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Jul-15 | |

| Jun-30 | |

| Jun-29 | |

| Jun-18 | |

| May-28 | |

| May-19 | |

| May-12 | |

| May-12 | |

| May-12 | |

| May-12 | |

| May-12 | |

| May-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite