|

|

|

|

|||||

|

|

|

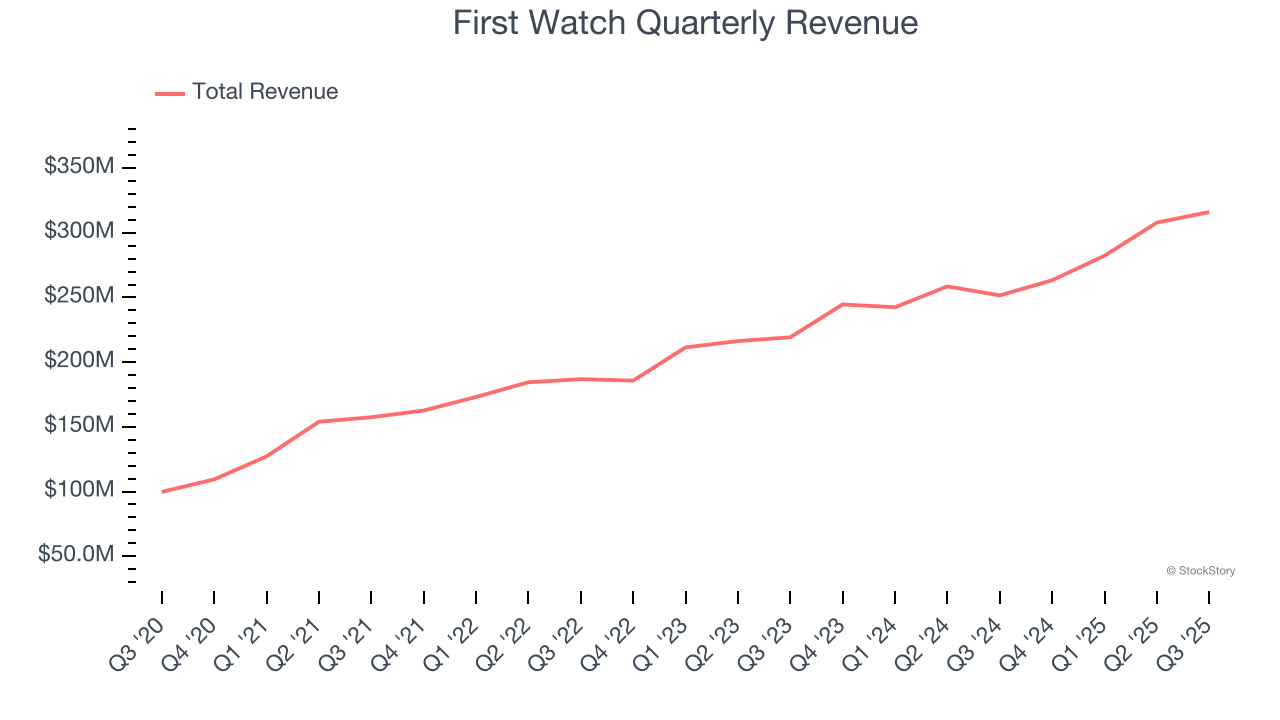

Breakfast restaurant chain First Watch Restaurant Group (NASDAQ:FWRG) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 25.6% year on year to $316 million. Its GAAP profit of $0.05 per share was $0.02 below analysts’ consensus estimates.

Is now the time to buy First Watch? Find out by accessing our full research report, it’s free for active Edge members.

“Our strong third quarter results and sequential year-to-date improvement in same restaurant traffic growth, same restaurant sales growth, and restaurant-level operating profit margin, are testament to the enduring strength of our business model and the efforts of our teams,” stated Chris Tomasso, CEO and President of First Watch.

Based on a nautical reference to the first work shift aboard a ship, First Watch (NASDAQ:FWRG) is a chain of breakfast and brunch restaurants whose menu is heavily-focused on eggs and griddle items such as pancakes.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.17 billion in revenue over the past 12 months, First Watch is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, First Watch’s 18.8% annualized revenue growth over the last six years (we compare to 2019 to normalize for COVID-19 impacts) was excellent as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, First Watch reported robust year-on-year revenue growth of 25.6%, and its $316 million of revenue topped Wall Street estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 17.4% over the next 12 months, similar to its six-year rate. Still, this projection is admirable and implies the market sees success for its menu offerings.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

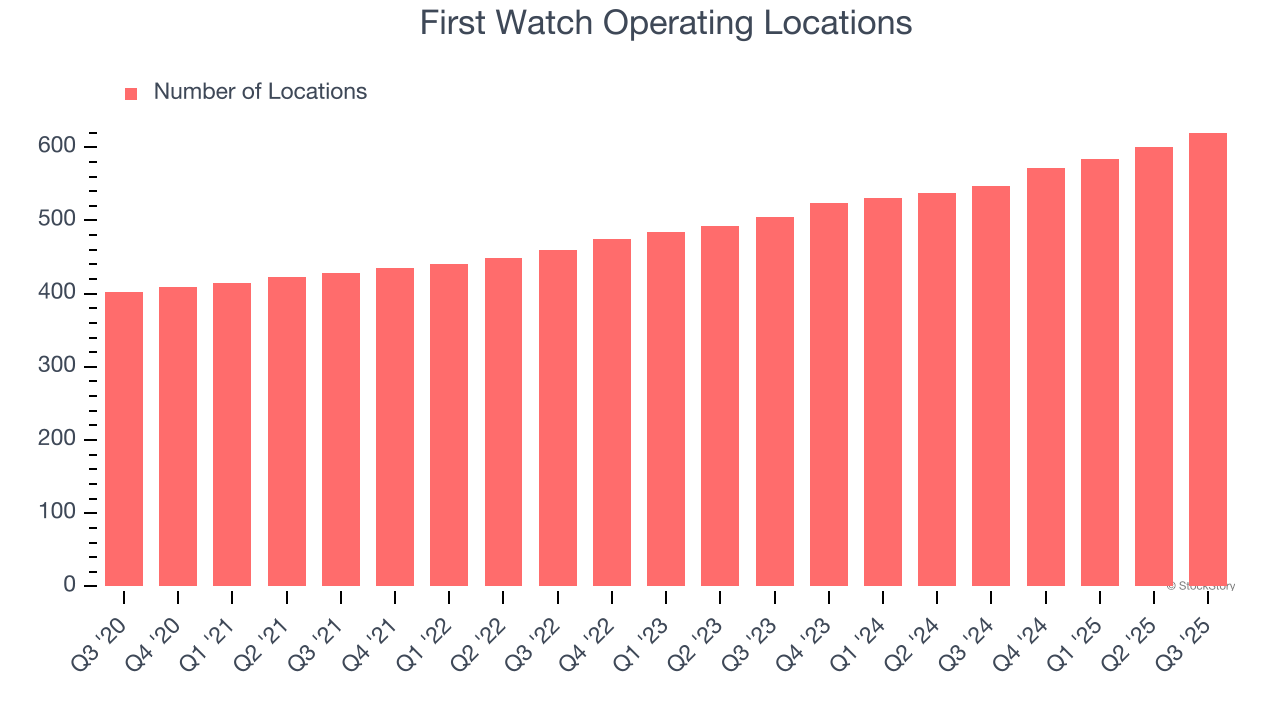

First Watch sported 620 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 10.2% annual growth, among the fastest in the restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

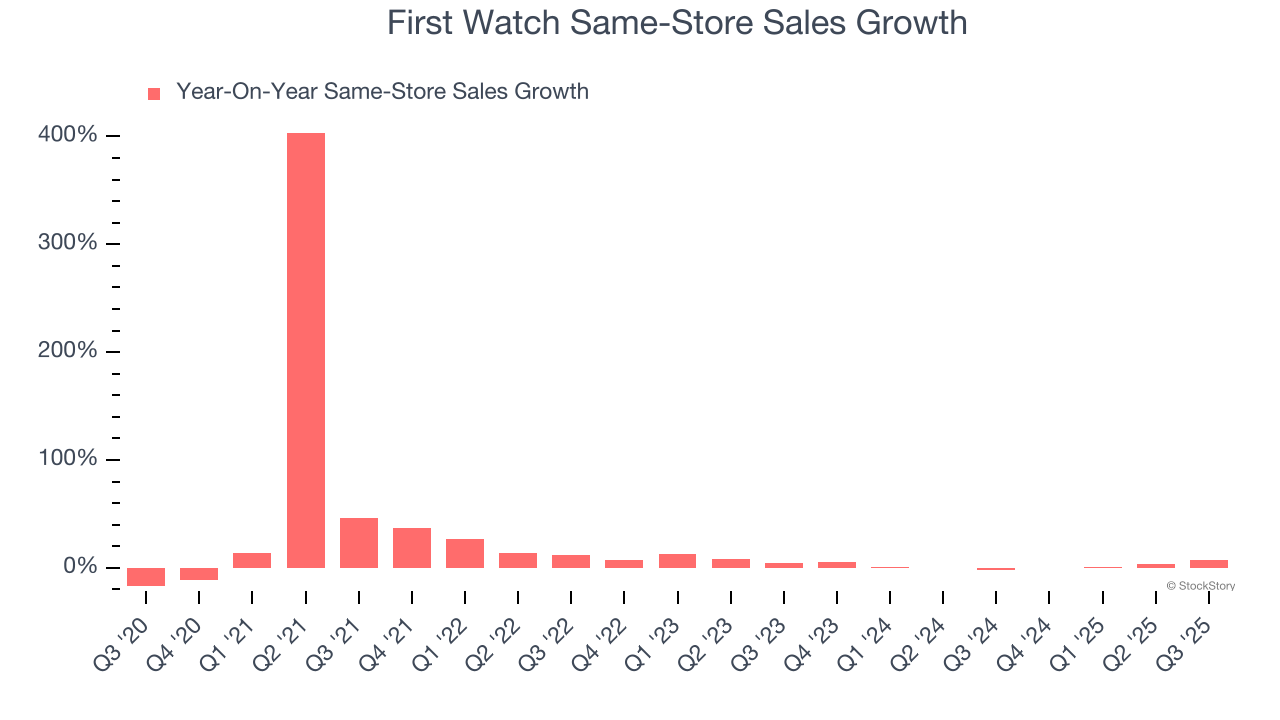

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

First Watch’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.8% per year. This performance suggests it should consider improving its foot traffic and efficiency before expanding its restaurant base.

In the latest quarter, First Watch’s same-store sales rose 7.1% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

We were impressed by how significantly First Watch blew past analysts’ same-store sales expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its EPS was in line. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 9.6% to $17.40 immediately following the results.

First Watch had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-21 | |

| Jul-01 | |

| Jun-09 | |

| Jun-09 | |

| Jun-08 | |

| May-06 | |

| May-05 | |

| May-05 | |

| May-04 | |

| May-04 | |

| Apr-21 | |

| Apr-12 |

Restaurants Are Finding It Harder Than Ever to Hire Someone to Wash the Dishes

FWRG

The Wall Street Journal

|

| Mar-10 | |

| Mar-09 | |

| Mar-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite