|

|

|

|

|||||

|

|

|

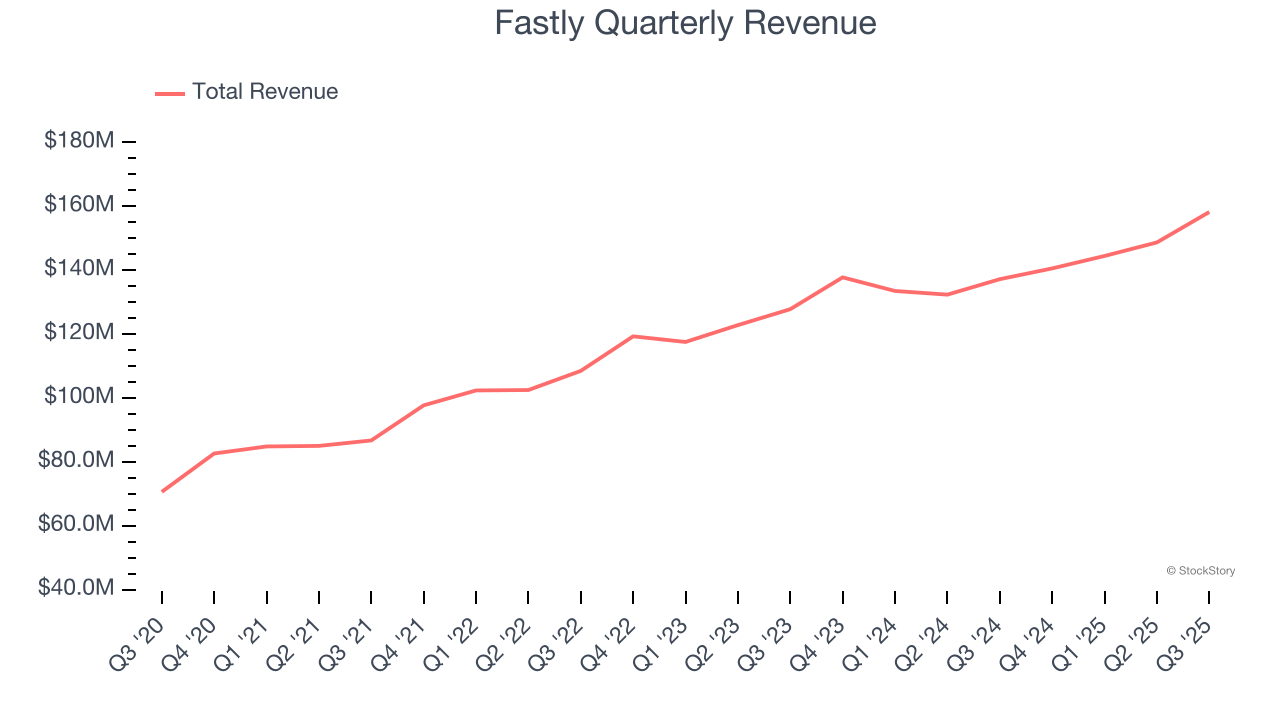

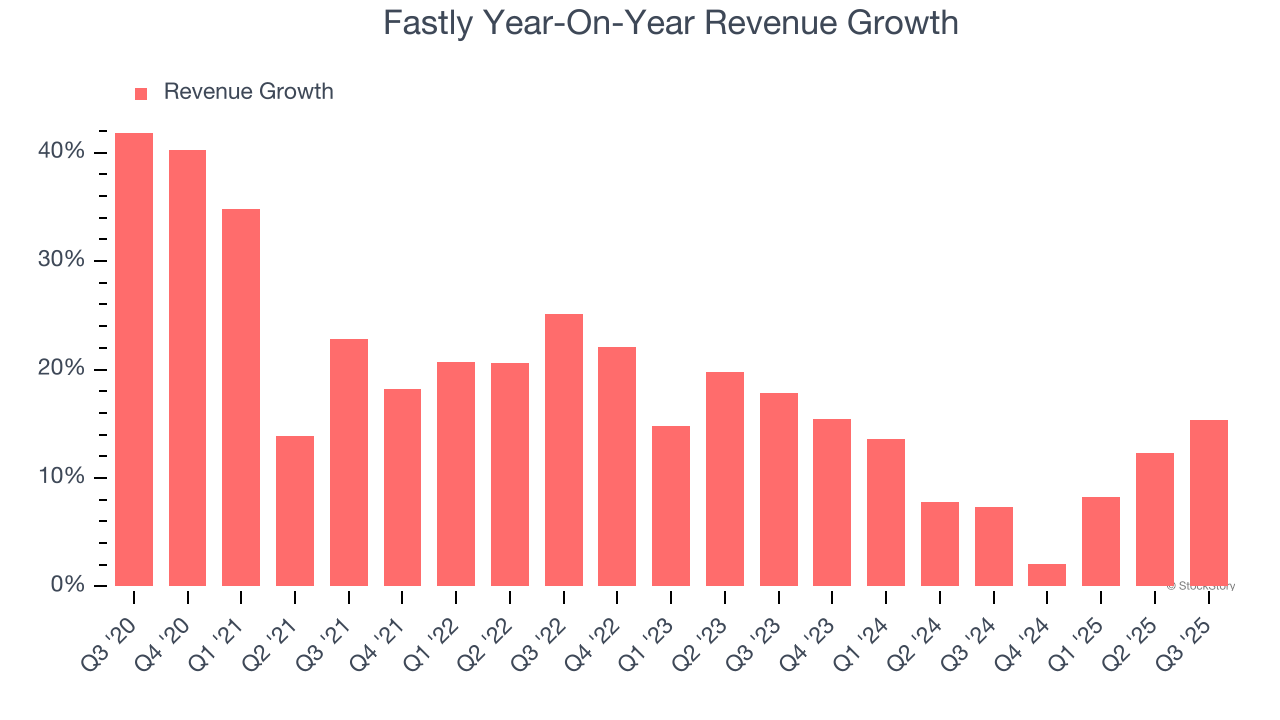

Edge cloud platform Fastly (NYSE:FSLY) announced better-than-expected revenue in Q3 CY2025, with sales up 15.3% year on year to $158.2 million. On top of that, next quarter’s revenue guidance ($161 million at the midpoint) was surprisingly good and 4.7% above what analysts were expecting. Its non-GAAP profit of $0.07 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Fastly? Find out by accessing our full research report, it’s free for active Edge members.

Taking its name from the core advantage it delivers to customers, Fastly (NYSE:FSLY) operates an edge cloud platform that processes, secures, and delivers web content as close to end users as possible, enabling faster digital experiences.

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Fastly grew its sales at a 17.2% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Fastly’s recent performance shows its demand has slowed as its annualized revenue growth of 10.2% over the last two years was below its five-year trend.

This quarter, Fastly reported year-on-year revenue growth of 15.3%, and its $158.2 million of revenue exceeded Wall Street’s estimates by 4.7%. Company management is currently guiding for a 14.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

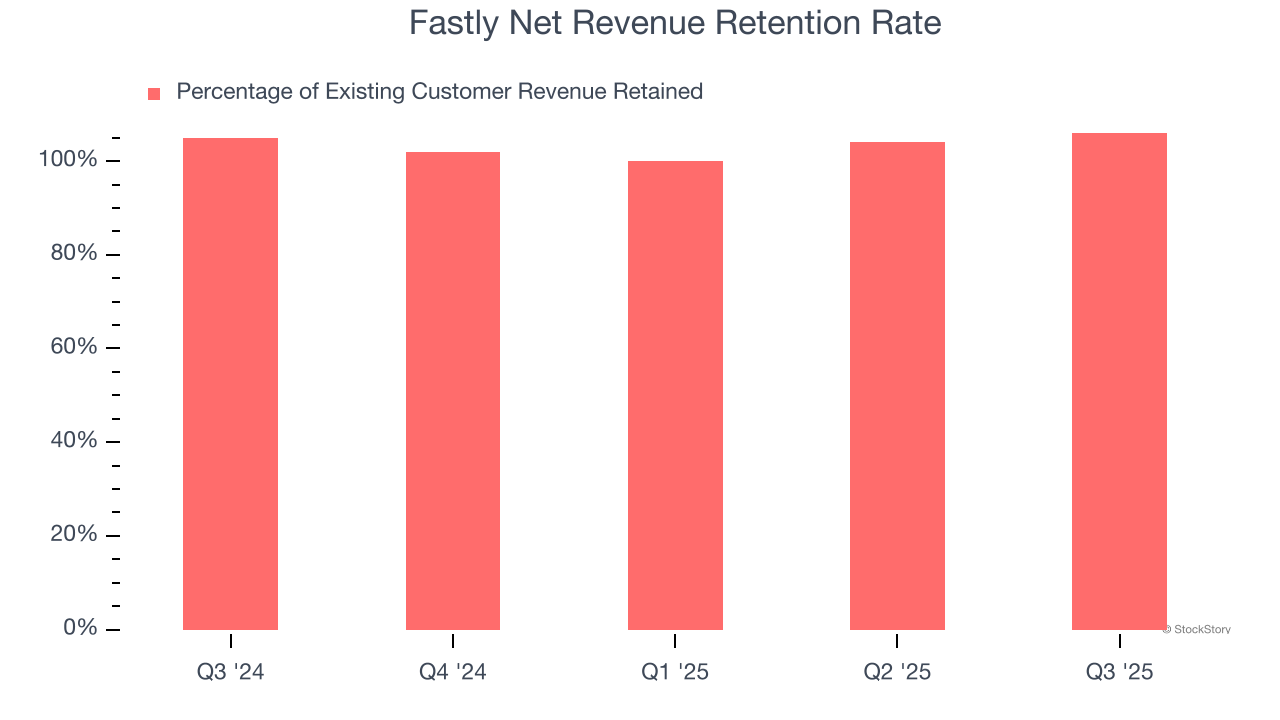

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Fastly’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 103% in Q3. This means Fastly would’ve grown its revenue by 3% even if it didn’t win any new customers over the last 12 months.

Fastly has an adequate net retention rate, showing us that it generally keeps customers but lags behind the best SaaS businesses, which routinely post net retention rates of 120%+.

We were impressed by Fastly’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 12.8% to $9.10 immediately after reporting.

Fastly may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Apr-02 | |

| Apr-02 | |

| Mar-31 | |

| Mar-30 | |

| Mar-24 | |

| Mar-21 | |

| Mar-14 | |

| Mar-10 | |

| Mar-09 | |

| Mar-06 | |

| Mar-04 | |

| Mar-03 | |

| Mar-02 | |

| Mar-02 | |

| Feb-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite