|

|

|

|

|||||

|

|

|

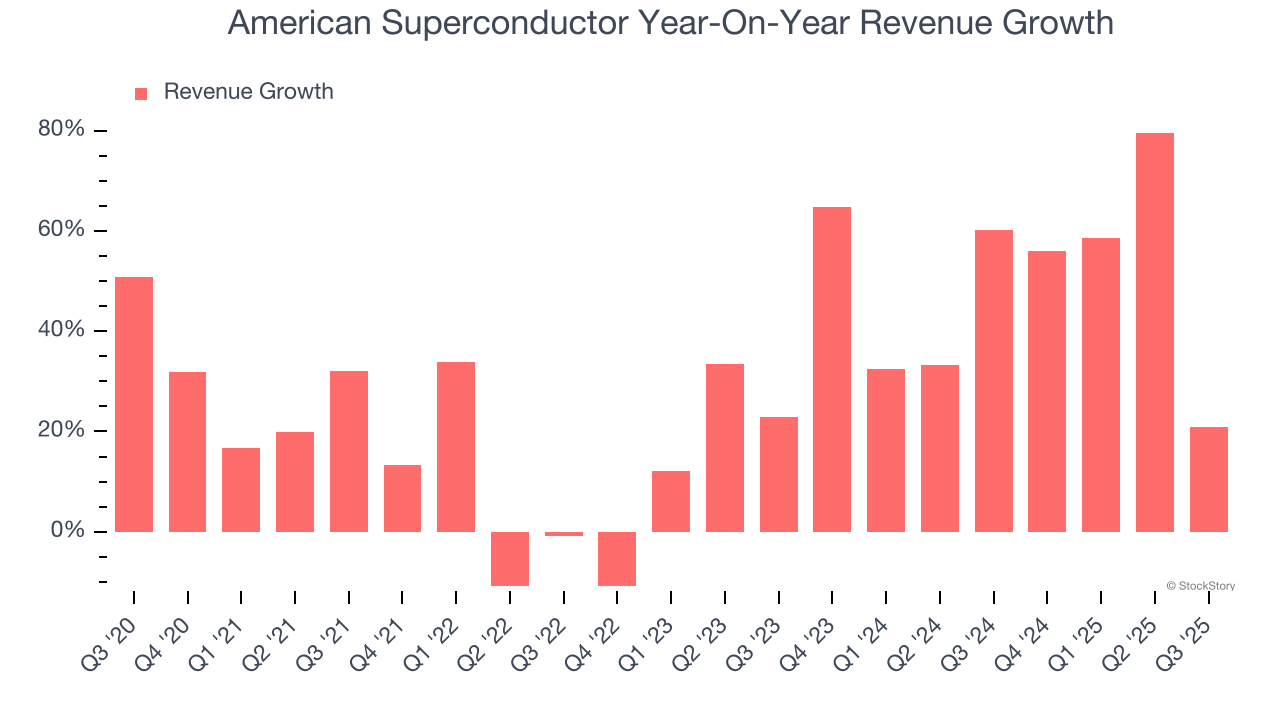

Power resiliency solutions provider American Superconductor (NASDAQ:AMSC) missed Wall Street’s revenue expectations in Q3 CY2025, but sales rose 20.9% year on year to $65.86 million. Next quarter’s revenue guidance of $67.5 million underwhelmed, coming in 0.6% below analysts’ estimates. Its non-GAAP profit of $0.20 per share was 30.4% above analysts’ consensus estimates.

Is now the time to buy American Superconductor? Find out by accessing our full research report, it’s free for active Edge members.

"AMSC grew second quarter revenue by over 20% year-over-year, generated net income of nearly $5 million marking our fifth consecutive quarter of profitability and achieved expanded gross margins surpassing 30%,” said Daniel P. McGahn, Chairman, President and CEO, AMSC.

Founded in 1987, American Superconductor (NASDAQ:AMSC) has shifted from superconductor research to developing power systems, adapting to changing energy grid needs and naval technology requirements.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, American Superconductor grew its sales at an incredible 27.7% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. American Superconductor’s annualized revenue growth of 49% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, American Superconductor generated an excellent 20.9% year-on-year revenue growth rate, but its $65.86 million of revenue fell short of Wall Street’s high expectations. Company management is currently guiding for a 9.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8% over the next 12 months, a deceleration versus the last two years. Still, this projection is above the sector average and implies the market is forecasting some success for its newer products and services.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

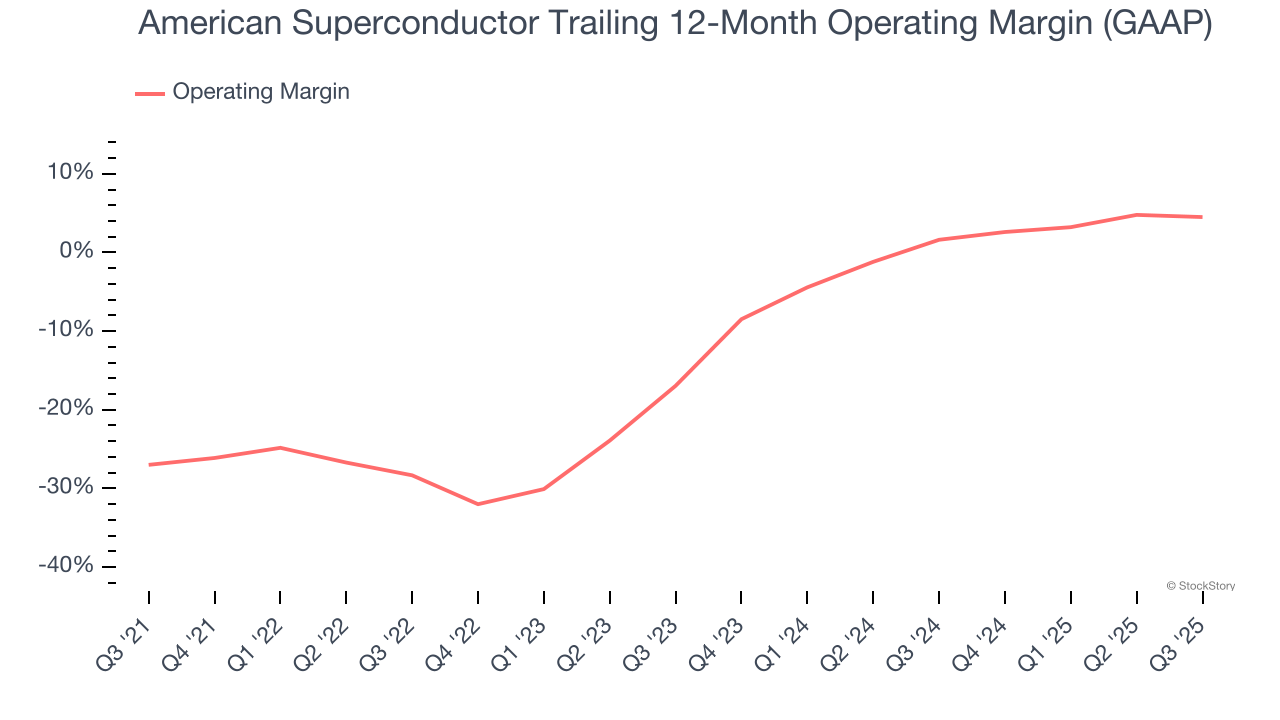

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Although American Superconductor was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 8.1% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, American Superconductor’s operating margin rose by 31.5 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

In Q3, American Superconductor generated an operating margin profit margin of 4.5%, down 1.3 percentage points year on year. Conversely, its revenue and gross margin actually rose, so we can assume it was less efficient because its operating expenses like marketing, R&D, and administrative overhead grew faster than its revenue.

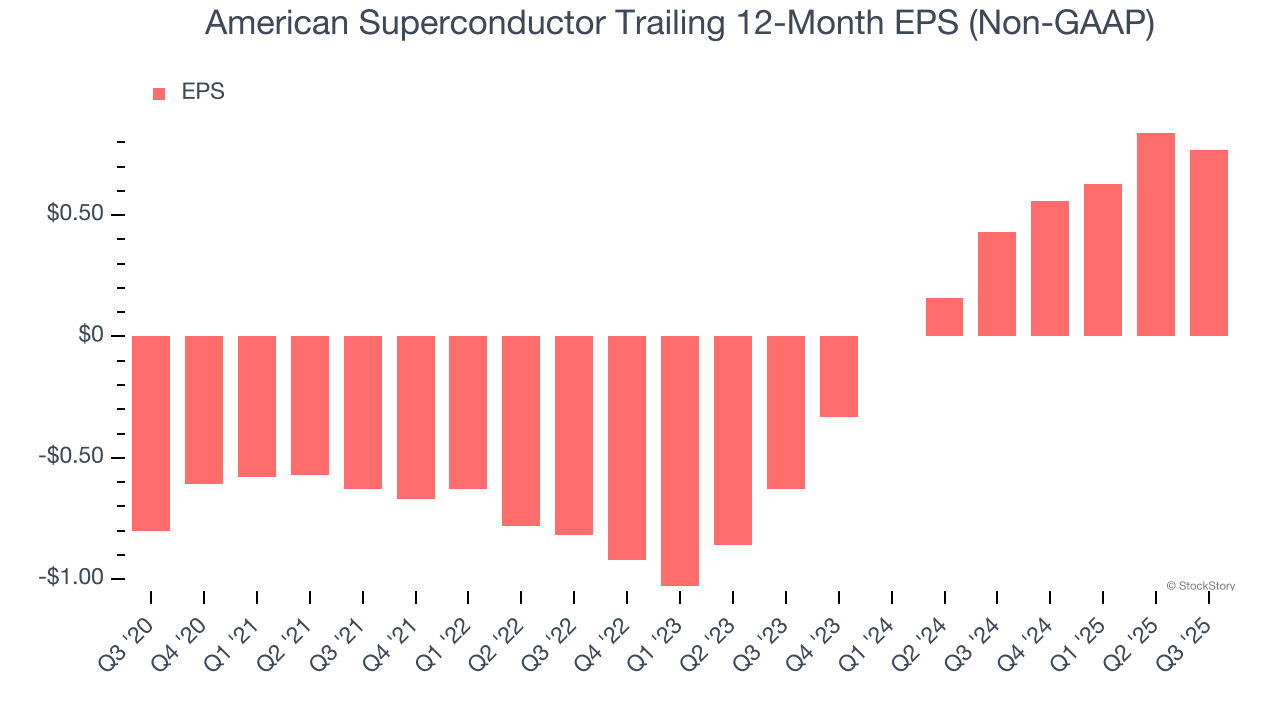

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

American Superconductor’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For American Superconductor, its two-year annual EPS growth of 79.5% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q3, American Superconductor reported adjusted EPS of $0.20, down from $0.27 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects American Superconductor’s full-year EPS of $0.77 to shrink by 8.2%.

It was good to see American Superconductor beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 16.9% to $49.20 immediately after reporting.

American Superconductor underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jun-04 |

American Superconductor CEO Puts AI Data-Center Growth In Perspective

AMSC

Investor's Business Daily

|

| May-28 | |

| May-28 | |

| May-27 | |

| May-27 | |

| May-21 | |

| May-01 | |

| Mar-04 | |

| Mar-03 | |

| Feb-13 |

American Superconductor CEO addresses challenges in grid reliability

AMSC +7.23%

Yahoo Finance Video

|

| Feb-12 | |

| Feb-11 | |

| Feb-08 | |

| Feb-06 | |

| Feb-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite