|

|

|

|

|||||

|

|

|

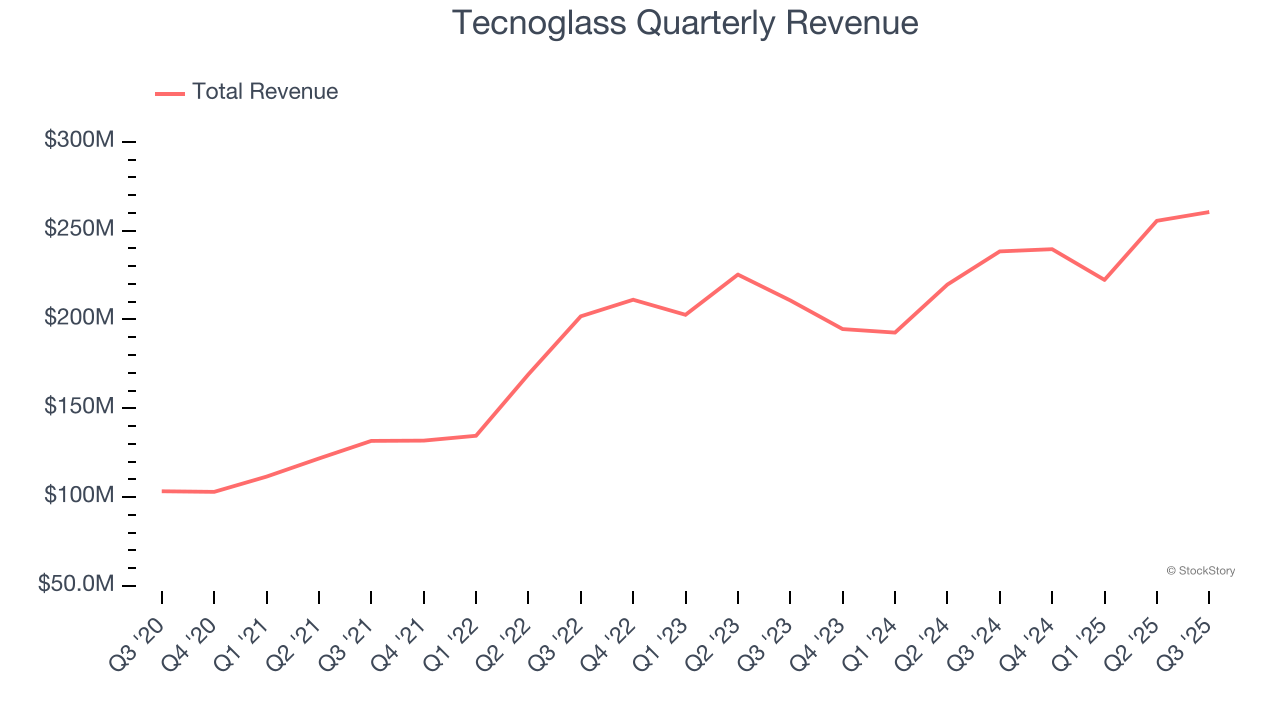

Glass and windows manufacturer Tecnoglass (NYSE:TGLS) fell short of the markets revenue expectations in Q3 CY2025, but sales rose 9.3% year on year to $260.5 million. The company’s full-year revenue guidance of $980 million at the midpoint came in 2.2% below analysts’ estimates. Its non-GAAP profit of $1 per share was 9.7% below analysts’ consensus estimates.

Is now the time to buy Tecnoglass? Find out by accessing our full research report, it’s free for active Edge members.

The first-ever Colombian company to trade on the NASDAQ, Tecnoglass (NYSE:TGLS) is a manufacturer of architectural glass, windows, and aluminum products.

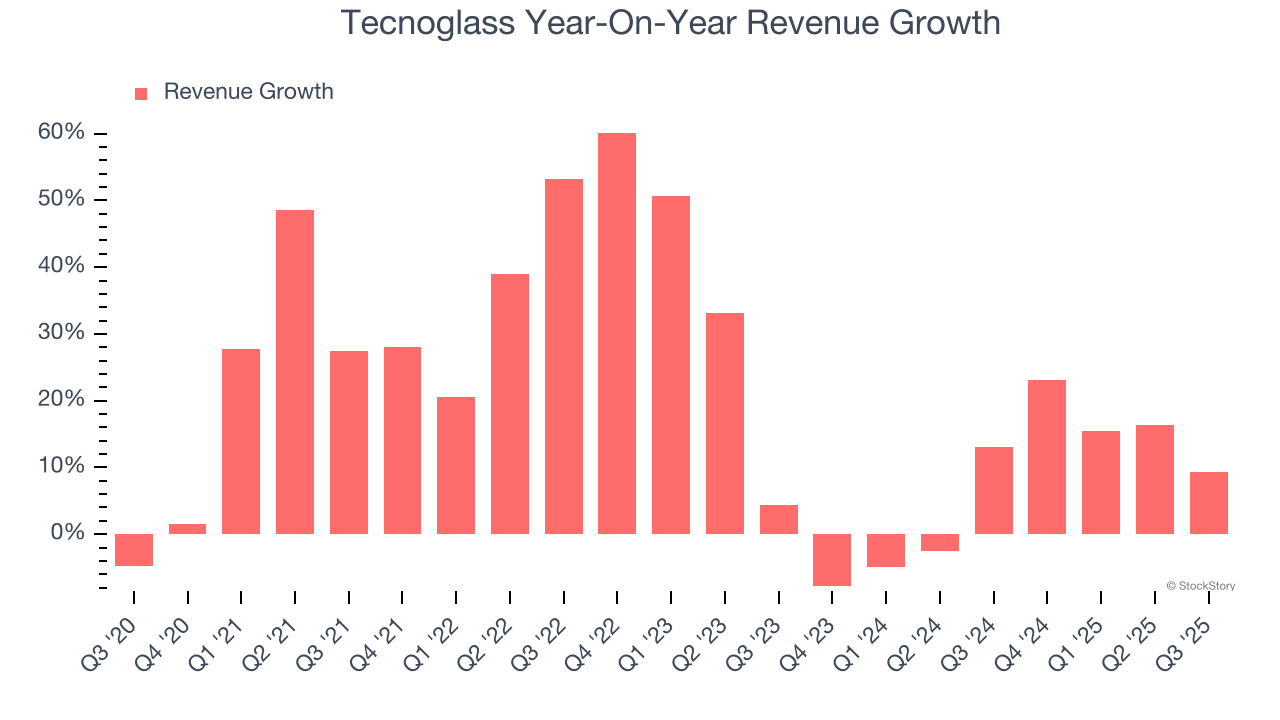

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Tecnoglass grew its sales at an incredible 21.2% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Tecnoglass’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 7.3% over the last two years was well below its five-year trend.

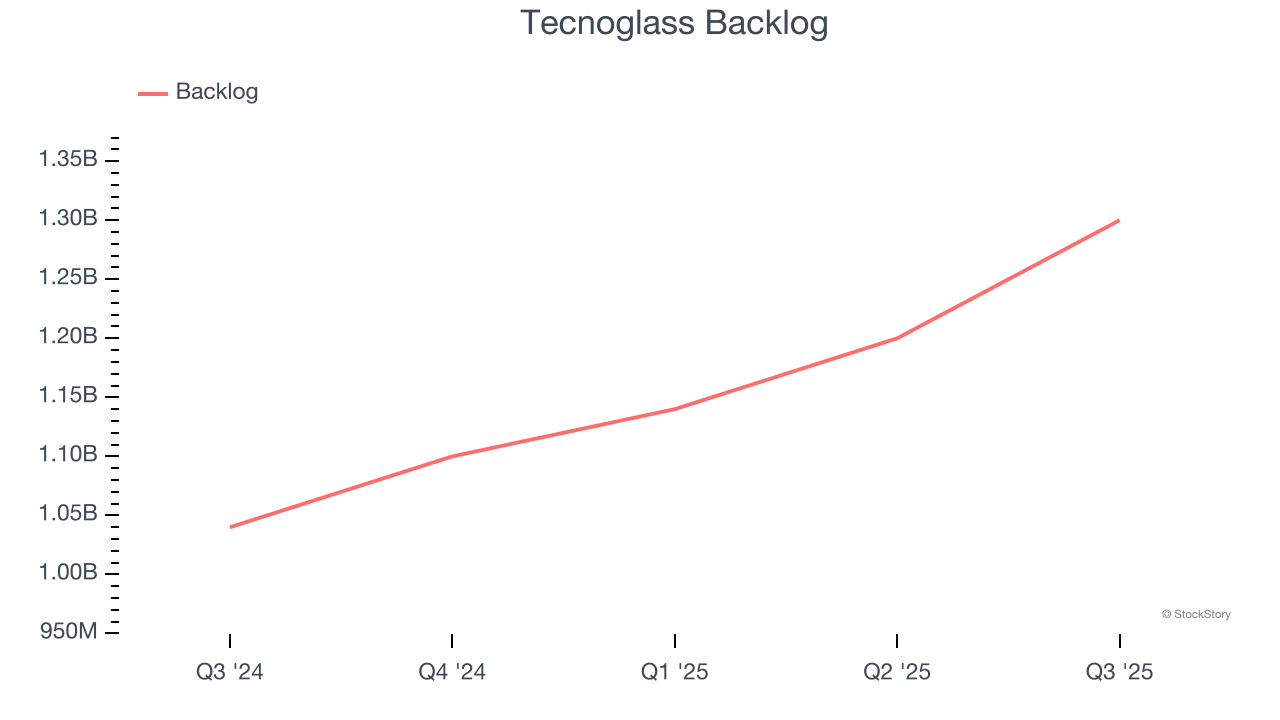

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Tecnoglass’s backlog reached $1.3 billion in the latest quarter and averaged 25% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Tecnoglass’s products and services but raises concerns about capacity constraints.

This quarter, Tecnoglass’s revenue grew by 9.3% year on year to $260.5 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.8% over the next 12 months, an improvement versus the last two years. This projection is admirable and implies its newer products and services will spur better top-line performance.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

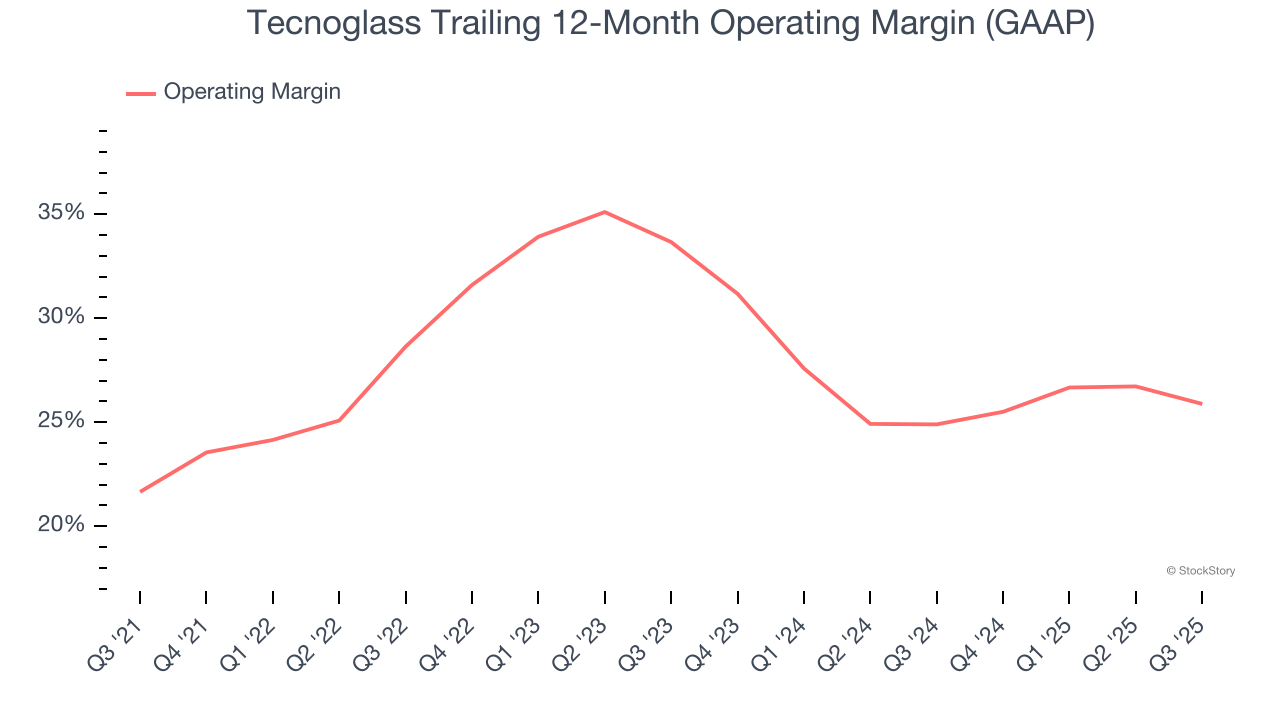

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Tecnoglass has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 27.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Tecnoglass’s operating margin rose by 4.2 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Tecnoglass generated an operating margin profit margin of 25.1%, down 3.3 percentage points year on year. Since Tecnoglass’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

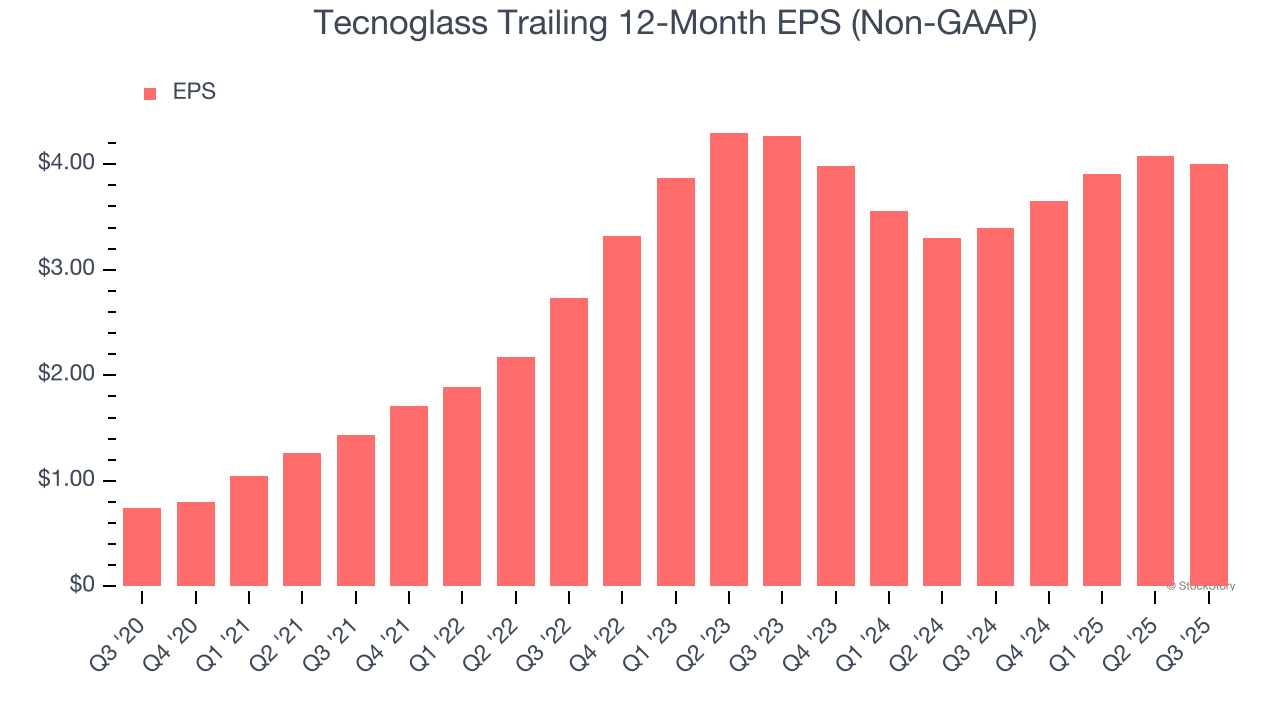

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Tecnoglass’s EPS grew at an astounding 40.1% compounded annual growth rate over the last five years, higher than its 21.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into Tecnoglass’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Tecnoglass’s operating margin declined this quarter but expanded by 4.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Tecnoglass, its two-year annual EPS declines of 3.2% mark a reversal from its (seemingly) healthy five-year trend. These shorter-term results weren’t ideal, but given it was successful in other measures of financial health, we’re hopeful Tecnoglass can return to earnings growth in the future.

In Q3, Tecnoglass reported adjusted EPS of $1, down from $1.08 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Tecnoglass’s full-year EPS of $4 to grow 14.6%.

We struggled to find many positives in these results. Its full-year EBITDA guidance missed and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.8% to $54.90 immediately following the results.

The latest quarter from Tecnoglass’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-21 | |

| Jun-10 | |

| May-19 | |

| May-07 | |

| Apr-21 | |

| Apr-09 | |

| Mar-18 | |

| Mar-02 | |

| Mar-02 | |

| Feb-28 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite