|

|

|

|

|||||

|

|

|

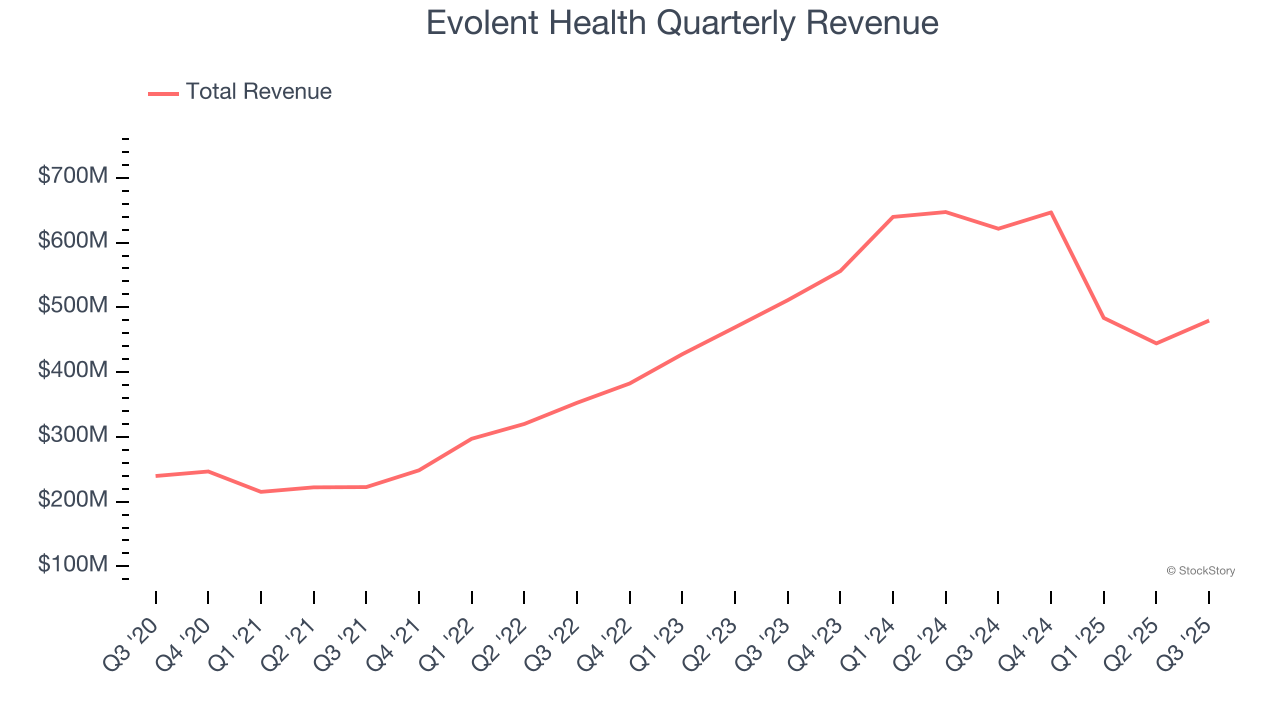

Healthcare solutions company Evolent Health (NYSE:EVH) beat Wall Street’s revenue expectations in Q3 CY2025, but sales fell by 22.8% year on year to $479.5 million. On the other hand, next quarter’s revenue guidance of $467 million was less impressive, coming in 1.2% below analysts’ estimates. Its non-GAAP profit of $0.05 per share was 52.5% below analysts’ consensus estimates.

Is now the time to buy Evolent Health? Find out by accessing our full research report, it’s free for active Edge members.

Seth Blackley, Co-Founder and Chief Executive Officer of Evolent stated, "We are happy to deliver a strong quarter, in the top half of our guidance for both Adjusted EBITDA and revenue, while reiterating our fourth quarter outlook. Further, we added another two customer agreements, bringing our total new contracts to thirteen for the year. We now have signed contracts that bring our preliminary 2026 revenue forecast to $2.5 billion. More importantly, we're winning in the marketplace with our Enhanced Performance Suite model that balances disciplined growth and margin. Finally, we continue to improve our product with our member navigation and Oncology Care Partners innovations. We expect to close the previously announced ECP transaction later this year and expect to use the proceeds to pay down our senior debt."

Founded in 2011 to transform how healthcare is delivered to patients with complex needs, Evolent Health (NYSE:EVH) provides specialty care management services and technology solutions that help health plans and providers deliver better care for patients with complex conditions.

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Evolent Health’s sales grew at an impressive 17.5% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Evolent Health’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 7.1% over the last two years was well below its five-year trend.

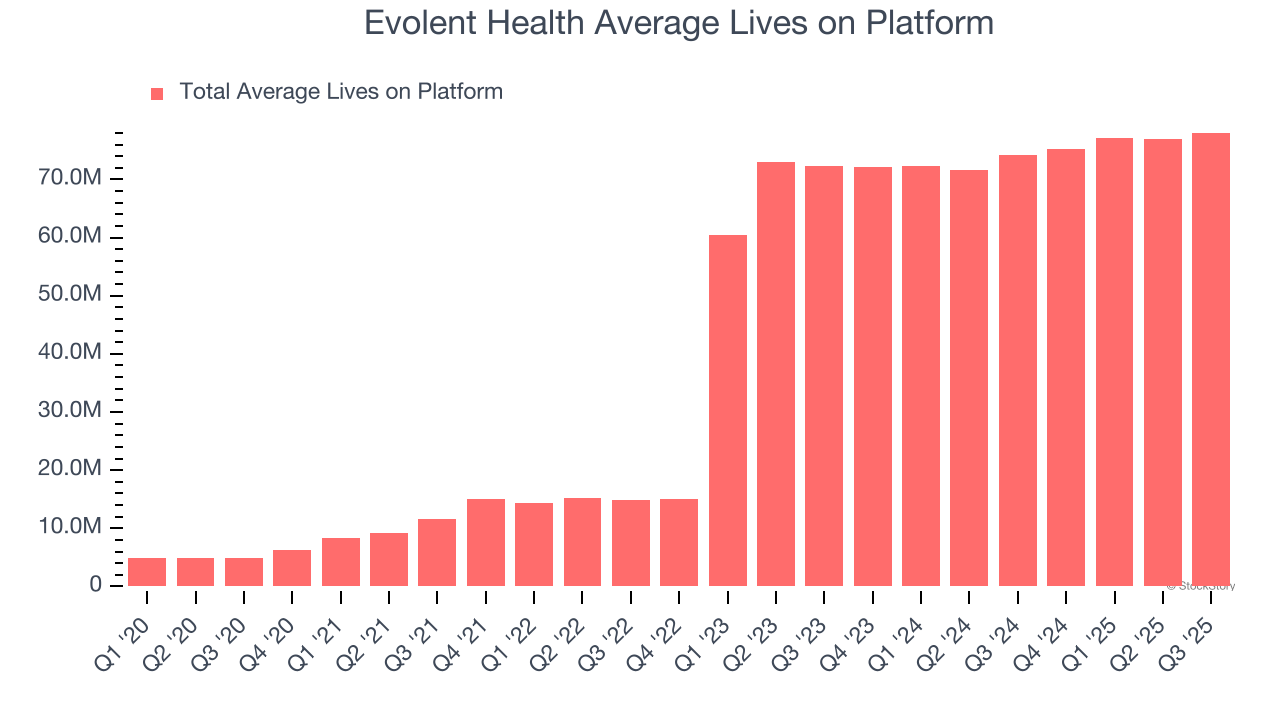

Evolent Health also reports its number of average lives on platform, which reached 78.05 million in the latest quarter. Over the last two years, Evolent Health’s average lives on platform averaged 53% year-on-year growth. Because this number is better than its revenue growth, we can see the company’s average selling price decreased.

This quarter, Evolent Health’s revenue fell by 22.8% year on year to $479.5 million but beat Wall Street’s estimates by 2.6%. Company management is currently guiding for a 27.8% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.7% over the next 12 months, an improvement versus the last two years. This projection is healthy and indicates its newer products and services will catalyze better top-line performance.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

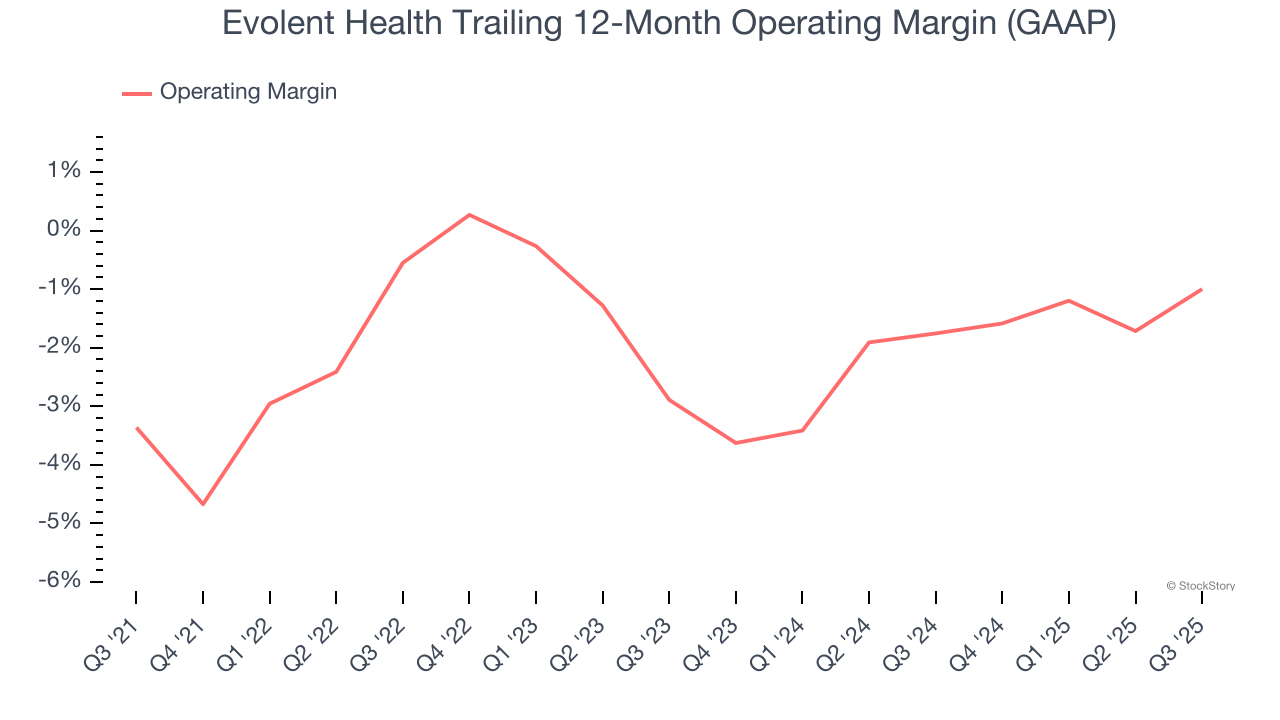

Although Evolent Health broke even this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 1.8% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Evolent Health’s operating margin rose by 2.4 percentage points over the last five years, as its sales growth gave it operating leverage. The company’s two-year trajectory shows its performance was mostly driven by its recent improvements.

This quarter, Evolent Health’s breakeven margin was up 2.8 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

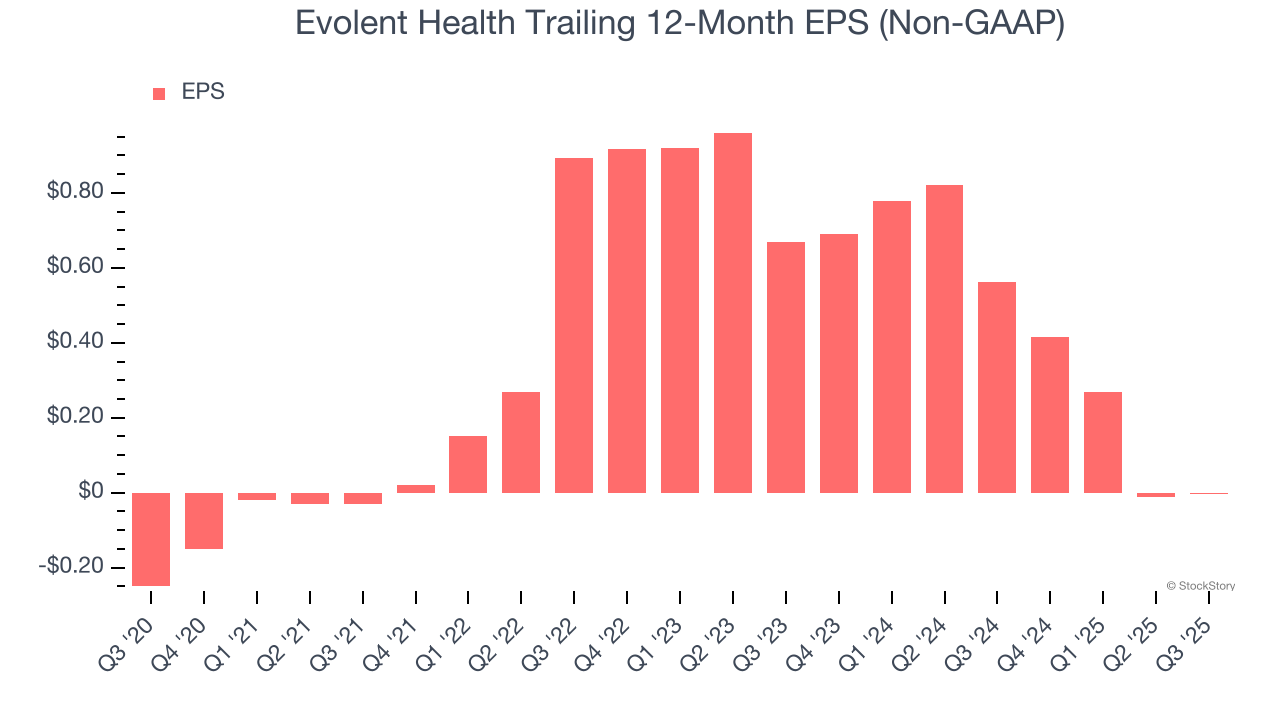

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Evolent Health’s full-year EPS flipped from negative to breakeven over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q3, Evolent Health reported adjusted EPS of $0.05, in line with the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Evolent Health’s full-year EPS of negative $0 will flip to positive $0.60.

Revenue and EBITDA beat Wall Street's expectations, which are big positives. On the other hand, guidance fell short of estimates. Overall, this was a mixed quarter. The stock traded up 15% to $6.90 immediately after reporting.

Is Evolent Health an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-20 | |

| Jul-08 | |

| May-12 | |

| May-12 | |

| May-08 | |

| May-07 | |

| May-07 | |

| Apr-07 | |

| Mar-19 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite