|

|

|

|

|||||

|

|

|

Solventum SOLV reported third-quarter 2025 adjusted earnings per share (EPS) of $1.50, which beat the Zacks Consensus Estimate of $1.43 by 4.9%. However, the bottom line declined 8.5% year over year.

GAAP EPS in the quarter was $7.22 compared with 70 cents in the year-ago quarter.

The company reported revenues of $2.1 billion, up 0.7% reportedly from the prior-year recorded number. Organically, sales were up 2.7%. The metric beat the Zacks Consensus Estimate by 0.3%. Organic sales growth was primarily driven by positive performance from all segments, primarily Dental Solutions and Health Information Systems (“HIS”).

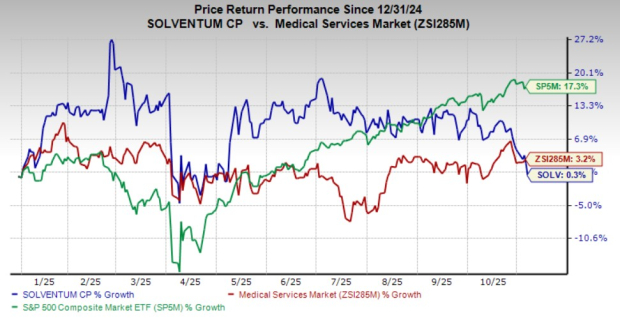

Shares of the company were up 2% during after-hours trading on Nov. 6, following mixed quarterly results. The stock has risen 0.3% so far this year compared with the industry’s gain of 3.2%. The S&P 500 Index has gained 17.3% in the same period.

MedSurg

Revenues from this segment totaled $1.21 billion, up 2.1% reportedly and up 1.1 % organically year over year. The sales growth was driven by double-digit growth of NPWT with single-use Prevena. Upselling and new product launches benefited IV site management and sterilization.

Dental Solutions

Revenues totaled $340 million, up 8.4% year over year reportedly and up 6.5% organically. The growth was driven by core restoratives led by Filtek, along with continued adoption of ClinPro Clear Fluoride Treatment.

HIS

Revenues from this segment amounted to $345 million, up 5.9% reportedly and 5.6% organically on a year-over-year basis. The growth was driven by Expanded adoption of 360 Encompass revenue cycle management and timing of consulting milestones, partially offset by a decline in Clinical Productivity Solutions.

Purification and Filtration

Revenues from this segment amounted to $128 million, down 28.7% year over year reportedly but up 6.4% organically. The company completed the divestment of this segment in September 2025.

Adjusted gross profit was $1.17 billion, down 1.9% year over year. As a percentage of revenues, the adjusted gross margin was 55.8%, down approximately 150 bps from the prior-year quarter’s figure.

Selling, general and administrative expenses totaled $780 million, up 11.3% year over year.

Research and development expenses totaled $183 million, down 3.2% on a year-over-year basis.

Adjusted operating income totaled $431 million, down 9.3% year over year. As a percentage of revenues, the adjusted operating margin was 20.6%, down approximately 220 bps from the prior-year quarter’s figure.

Solventum exited the third quarter with cash, cash equivalents and investments of $1.64 billion compared with $492 million in the previous quarter.

Total assets decreased to $13.97 billion from $15.07 billion in the previous quarter.

Cumulative net cash provided by operating activities during the third quarter was $274 million compared with $966 million in the year-ago period.

Solventum raised its sales guidance for 2025. The company now expects organic sales growth at the higher end of 2-3% (2.5-3.5% excluding ~50bps of SKU Exit impact). The Zacks Consensus Estimate is pegged at $8.29 billion.

SOLV now expects adjusted EPS to be in the band of $5.98-$6.08 (previously $5.88-$6.03). The Zacks Consensus Estimate for earnings is pinned at $5.95 per share.

Solventum Corporation price-consensus-eps-surprise-chart | Solventum Corporation Quote

Solventum exited the third quarter on a strong note, wherein earnings and sales beat the Zacks Consensus Estimate. Solid execution across MedSurg, Dental Solutions, and Health Information Systems, combined with a steady pipeline of product innovation, continues to lift organic growth and expand market share. Commercial restructuring is proving effective, with specialization, accountability metrics, and leadership changes translating into faster decision-making and stronger conversion across growth platforms like negative pressure wound therapy, antimicrobial IV site management, and restorative dental products.

Operational discipline remains a core theme. Supply-chain optimization, tariffs mitigation, and the recently announced “Transform for the Future” program are expected to drive substantial cost savings and offset inflationary and tariff pressures while freeing up capital for R&D and commercial acceleration. The successful sale of the Purification and Filtration business materially strengthened the balance sheet, reduced debt, and expanded flexibility for tuck-in M&A or potential capital returns.

Progress on separation from 3M is ahead of plan, with ERP transitions and manufacturing consolidation supporting improved service levels and enhanced operational control. With raised guidance, consistent volume-driven performance, and tangible progress toward long-range revenues and margin targets, Solventum enters 2026 well-positioned to accelerate profitable growth and expand value creation for shareholders, customers, and patients.

Solventum currently carries a Zacks Rank #2 (Buy).

Some other top-ranked stocks in the broader medical space are McKesson MCK, Boston Scientific Corporation BSX and Alcon ALC.

McKesson, sportinga Zacks Rank #1 (Strong Buy) at present, has an estimated long-term growth rate of 14.6%. MCK’s earnings surpassed estimates in three of the trailing four quarters and missed once, with the average surprise being 3.49%. You can see the complete list of today’s Zacks #1 Rank stocks here.

McKesson’s shares have gained 50.8% compared with the industry’s 9.1% growth so far this year.

Boston Scientific, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 16.4%. BSX’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 7.36%.

Boston Scientific’s shares have gained 10.7% compared with the industry’s 0.5% growth so far this year.

Alcon, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 10.3%. ALC’s earnings surpassed estimates in three of the trailing four quarters and missed once, with the average surprise being 4.61%.

Alcon’s shares have declined 12.5% against the industry's 0.4% gain so far this year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 11 hours | |

| Jun-23 | |

| Jun-18 | |

| Jun-18 | |

| Jun-17 | |

| Jun-14 | |

| Jun-12 | |

| Jun-12 | |

| Jun-11 | |

| Jun-08 | |

| Jun-04 | |

| Jun-03 | |

| Jun-03 | |

| Jun-02 | |

| Jun-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite