|

|

|

|

|||||

|

|

|

The Boeing Company’s BA shares have rallied 9.9% in the year-to-date period, underperforming the Zacks Aerospace-Defense industry’s growth of 32.5%. The company faces risks related to the shortage of labor and lingering supply-chain challenges.

Other defense stocks, such as General Dynamics GD and Northrop Grumman NOC, have also underperformed the industry during the same period. Shares of GD have risen 31.4% while those of NOC have gained 21.2% during the same timeframe.

Let’s examine the factors that might have led to the stock’s underperformance.

While Boeing presents strong growth potential, it also faces several key challenges that investors should weigh carefully. Although global air travel demand continues to recover and expand, the aviation industry remains constrained by persistent supply-chain disruptions, including shortages of engines, castings, and other critical components.

These bottlenecks have delayed aircraft deliveries and increased production costs, limiting manufacturers’ ability to fully capitalize on rising demand. Additionally, geopolitical tensions and logistical challenges across supplier networks could prolong these constraints through the remainder of 2025.

According to International Air Transport Association (“IATA”), the supply-chain constraints will hinder airlines from reaching their full growth potential. As per IATA’s June 2025 outlook, aircraft deliveries are currently about 30% below their previous peak, pushing the global aircraft backlog to a record 17,000 units. Fewer jet deliveries imply lower demand for aircraft made by Boeing, thereby weakening its near-term revenue generation prospects.

Moreover, the persistent trade tensions between China and America continue to pose a threat for Boeing. As of Sept. 30, 2025, Boeing had about five 737-8 aircraft in inventory for Chinese customers, scheduled for delivery by year-end. Any escalation in trade disputes could delay these deliveries, hurt Boeing Commercial Airplanes’ (“BCA”) revenues, and increase inventory costs.

Boeing remains one of the largest aircraft manufacturers in the United States in terms of revenues, orders and deliveries, particularly in the commercial aerospace industry. Boeing, being a prominent jet manufacturer, has been witnessing solid delivery and order activities lately. Keeping up with this trend, the company’s BCA segment registered 38% year-over-year growth in its delivery count for the third quarter of 2025, which resulted in a 49% surge in this unit’s revenues.

During the third quarter, the company booked 161 net commercial airplane orders. Such solid order activities should continue to bolster revenue performance for Boeing’s commercial business over the long run.

The Defense Logistics Agency and Boeing assessed a new contract-and-delivery mechanism in November 2025, called Rapid Delivery Release ("RDR"), which reduces the typical proposal-to-award cycle. According to early trial results, RDR parts can be delivered to military customers several months sooner. Boeing is expected to benefit from the RDR model as an operational lever. The company's service offering and revenue mechanics are also expected to improve.

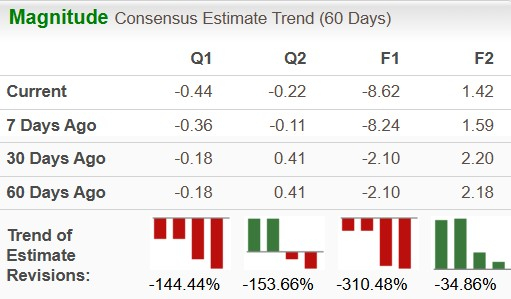

The Zacks Consensus Estimate for 2025 and 2026 earnings per share (EPS) indicates a decrease of 310.48% and 34.86%, respectively, over the past 60 days.

The Zacks Consensus Estimate for General Dynamics’s 2025 and 2026 EPS indicates an increase of 0.85% and 0.76%, respectively, over the past 60 days. The consensus estimate for Northrop Grumman’s 2025 EPS indicates an increase of 2.44% and that for 2026 implies a decline of 0.10% in the past 60 days.

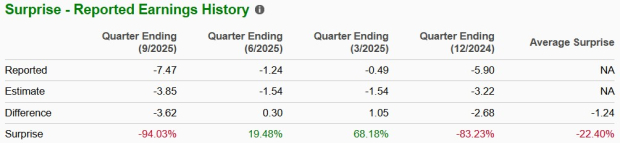

The company beat on earnings in two of the trailing four quarters and missed in two, delivering a negative average surprise of 22.4%.

The image below shows that BA stock’s trailing 12-month return on invested capital (ROIC) not only lags the peer group’s average return but also reflects a negative figure. This suggests that the company's investments are not yielding sufficient returns to cover its expenses.

In terms of valuation, Boeing’s forward 12-month price-to-sales (P/S) is 1.57X, a discount to the industry’s average of 2.35X. This suggests that investors will be paying a lower price than the company's expected sales growth compared to that of its peer group.

Its industry peers are also trading at a discount compared to the industry’s forward 12-month P/S. While General Dynamics is trading at forward 12-month sales of 1.74, Northrop Grumman is trading at 1.85.

Boeing’s growth prospects remain strong amid recovering global air travel demand, but persistent supply-chain disruptions and trade tensions continue to constrain aircraft deliveries and raise production costs. With global jet deliveries about 30% below peak levels and a record backlog, these challenges could weigh on Boeing’s near-term revenues and delay its recovery.

Considering its price underperformance, low ROIC and declining earnings estimates, it is advisable for investors to avoid this Zacks Rank #4 (Sell) stock at present.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite