|

|

|

|

|||||

|

|

|

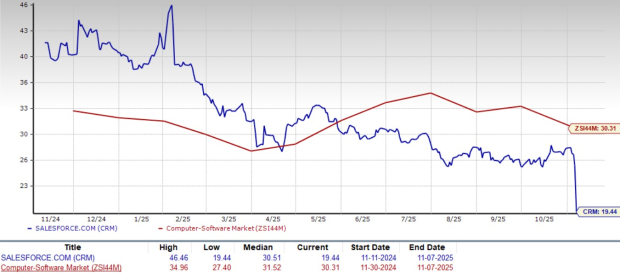

Salesforce, Inc. CRM stock looks attractive from a valuation perspective. CRM is currently trading at a forward 12-month price-to-earnings (P/E) multiple of 19.44, significantly lower than the Zacks Computer – Software industry’s average of 30.31.

Compared to major competitors like Microsoft MSFT, Oracle ORCL and SAP SAP, Salesforce’s stock is cheaper on a P/E basis. At present, Microsoft, Oracle and SAP trade at P/E multiples of 29.97, 32.56 and 31.72, respectively.

Given Salesforce’s attractive valuation, investors might be wondering: Is this an opportunity to buy, or are there deeper challenges that could keep the stock in check?

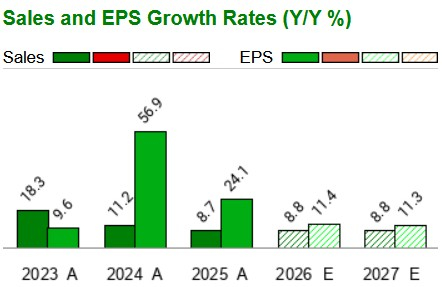

Salesforce’s biggest challenge right now is slowing sales growth. For years, it delivered strong double-digit revenue increases. However, that pace has now cooled to single digits. In the first half of fiscal 2026, revenues rose just 8.7% year over year, and non-GAAP earnings per share (EPS) grew by only 9.4%.

This slowdown reflects cautious enterprise spending amid economic uncertainty and geopolitical pressures. Analysts’ revenue projections indicate no significant improvements in the years ahead. The Zacks Consensus Estimate for both fiscal 2026 and 2027 revenues indicates year-over-year growth in the high single-digit percentage.

The impact is also visible in profit forecasts. Salesforce’s EPS is now expected to witness a CAGR of 13.9% over the next five years, which is a big drop from the 27.8% CAGR it posted over the previous five years. Fiscal 2026 and 2027 EPS forecasts indicate a year-over-year improvement of around 11%.

This changing growth profile shows how businesses are adjusting their IT budgets. Instead of large digital transformation projects, many are opting for smaller, lower-risk investments. For Salesforce, this means it has to adapt its strategy to stay competitive and relevant.

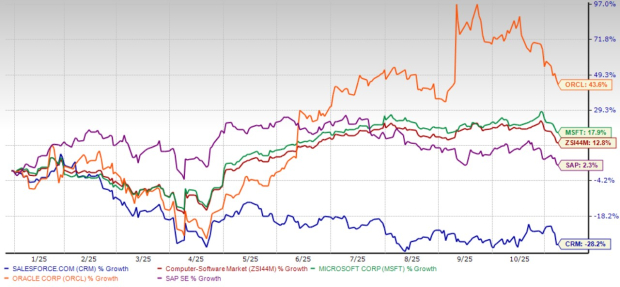

Slower growth has also hurt investor sentiment. Salesforce shares have plunged 28.2% year to date, while the industry has risen 12.8%. The stock is also lagging behind key rivals like Oracle, Microsoft and SAP. Year to date, shares of Microsoft, Oracle and SAP have risen 43.6%, 17.9% and 2.3%, respectively.

Nonetheless, Salesforce’s sustained focus on expanding in the enterprise software space could provide a solid base to return to its robust growth trajectory.

Salesforce has long held the top position in the customer relationship management market, according to Gartner. The company’s vision now goes beyond customer management, and it is building a broader ecosystem focused on artificial intelligence (AI), data and collaboration. Acquisitions like Waii, Bluebirds, Informatica and Slack show Salesforce’s push to evolve into a more complete enterprise platform.

AI is now central to Salesforce’s growth story. Since the 2023 rollout of Einstein GPT, Salesforce has been embedding generative AI across its offerings to help companies automate processes, improve decision-making and strengthen customer relationships.

Its latest innovation, Agentforce, is gaining momentum. Combined with Data Cloud, these AI-driven offerings brought in $1.2 billion in recurring revenues in the second quarter of fiscal 2026, up 120% year over year. More than 40% of Agentforce deals came from existing clients, showing Salesforce’s success in cross-selling AI features to its user base.

Another long-term tailwind is rising global spending on generative AI. Gartner estimates that worldwide generative AI spending will hit $644 billion in 2025, implying a 76.4% year-over-year increase.

Enterprise software, a key segment for Salesforce, is expected to grow even faster, with a projected increase of 93.9% to $37.16 billion. Even if economic conditions slow down spending in the short term, digital transformation remains a top priority for businesses, ensuring steady demand for Salesforce’s solutions.

Salesforce’s slowing growth is real and has weighed on its stock price. However, its leadership in the CRM software space, focus on AI, strategic acquisitions and reasonable valuations provide reasons to hold the stock for long-term gains.

Salesforce carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 35 min | |

| Jul-29 | |

| Jul-29 |

Even $64 Billion in Quarterly Profit Is a Disappointment for Chip Investors

MSFT MSFT +8.83% AH

The Wall Street Journal

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite