|

|

|

|

|||||

|

|

|

JD.com JD is slated to report third-quarter 2025 results on Nov. 13.

For the third quarter, the Zacks Consensus Estimate for revenues is pegged at $41.33 billion, indicating growth of 11.4% from the year-ago quarter’s reported figure.

The consensus mark for earnings is pinned at 46 cents per share, suggesting a 62.9% decline from the prior-year quarter’s reported number. The estimates have increased by two cents over the past 30 days.

In the last reported quarter, the company delivered an earnings surprise of 13.76%. The company’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 18.89%.

JD.com, Inc. price-consensus-eps-surprise-chart | JD.com, Inc. Quote

Our proven model does not conclusively predict an earnings beat for JD.com this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

JD has an Earnings ESP of -3.30% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

JD.com entered the third quarter of 2025 with accelerating momentum following second-quarter results that showed 22% year-over-year revenue growth. JD's quarterly active customer base and user shopping frequency both increased over 40%, indicating strengthening engagement across core retail operations and newer initiatives.

The third quarter is expected to have reflected continued strength in JD Retail, which recorded 21% revenue growth and an operating margin of 4.5% in the prior period. Electronics and home appliance categories likely benefited from government trade-in incentives, while general merchandise maintained a growth trajectory, supported by steady supermarket performance. Marketplace and marketing revenues are anticipated to have continued their recent growth trend, though at a slower pace amid a more cautious consumer environment.

JD Food Delivery, launched in February, likely remained an area of focus during the quarter. The segment expanded its logistics reach and merchant base following strong activity during the June 618 promotion, but high operating and promotional costs may have constrained profitability. The rollout of 7Fresh Kitchen, aimed at developing proprietary offerings through supply-chain partnerships, may have added differentiation but also increased operating complexity.

During the quarter, JD announced a voluntary public takeover offer for CECONOMY AG, the parent company of MediaMarkt and Saturn, in a proposed EUR 2.2 billion transaction. The deal underscores JD’s push toward international diversification but introduces regulatory and integration challenges. Competitive intensity in the domestic food delivery market remained elevated, likely weighing on near-term margins despite ongoing efforts to strengthen logistics efficiency and ecosystem integration.

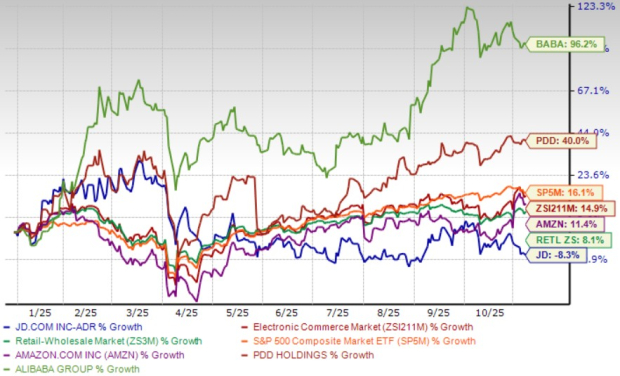

JD.com shares have plunged 8.3% in the year-to-date period (YTD) compared with the Internet-Commerce industry, the Zacks Retail-Wholesale sector and the S&P 500 index’s jump of 14.9%, 8.1% and 16.1%, respectively.

JD has also underperformed its industry peers, Amazon AMZN, Alibaba BABA and PDD Holdings PDD. Shares of Amazon and PDD Holdings have appreciated 11.4%, 96.2% and 40%, respectively, in the same period.

From a valuation perspective, JD currently trades at a forward 12-month P/E ratio of 9.06X, which is well below the Zacks Internet - Commerce industry’s 25.33X. This suggests that investors may be paying a lower price relative to the company's expected earnings growth.

JD.com enters the third quarter of 2025 with encouraging year-over-year growth expectations, supported by consistent performance in its core retail operations and measured expansion across new business lines. However, the company’s ongoing investments in food delivery, logistics infrastructure and international ventures are likely to weigh on near-term profitability. While government trade-in incentives and promotional activity have supported demand in electronics and general merchandise, operating leverage may remain limited as JD continues scaling recently launched initiatives such as JD Food Delivery and 7Fresh Kitchen.

The proposed acquisition of CECONOMY offers a long-term opportunity to expand into the European market, though it introduces regulatory and integration challenges. Competitive intensity in China’s food delivery and e-commerce landscape also remains high, which could constrain margin recovery in newer segments. JD’s forward P/E of 9.06X, notably below the broader industry average, indicates reasonable valuation but also reflects investor caution surrounding earnings quality and execution risks.

JD.com maintains a stable growth profile supported by resilient retail demand and strategic diversification efforts. However, elevated spending on logistics, new business expansion and international ventures may keep operating margins under pressure in the short term. Compared with peers such as Amazon, Alibaba and PDD Holdings, JD remains in an investment-driven phase focused on long-term ecosystem development rather than immediate profit recovery. The company’s valuation presents potential upside for long-term investors, but a patient approach could be prudent, with potential re-entry once margin stability and earnings visibility improve.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 36 min | |

| 57 min | |

| 4 hours | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN

Investor's Business Daily

|

| Jul-25 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite