|

|

|

|

|||||

|

|

|

DigitalOcean provides cloud computing services to small and mid-sized businesses, and it's aggressively entering the AI space.

The company's AI revenue has more than doubled for five consecutive quarters, fueled by a rapid increase in high-spending customers.

DigitalOcean stock looks like a bargain based on two valuation metrics, and a couple of top Wall Street firms just increased their price targets on it.

Less than two months remain in 2025, so now might be a good time for investors to think about which stocks they want to take into the new year. Artificial intelligence (AI) has been a key driver of returns for the last few years, and that's likely to be the case again in 2026, given that demand for things like data center infrastructure continues to significantly outstrip supply.

DigitalOcean (NYSE: DOCN) provides cloud computing services to small and mid-sized businesses (SMBs), and it also offers a growing portfolio of AI services that is attracting some very high-spending customers. In fact, DigitalOcean's revenue growth has accelerated this year.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Here's why it could be the ultimate stock to own heading into the new year.

Image source: Getty Images.

The cloud computing industry is dominated by multitrillion-dollar giants like Amazon and Microsoft, but those providers typically fight over the biggest enterprise customers with the highest spending potential. Startups and SMBs don't really move the needle for them from a revenue perspective, but DigitalOcean has built a lucrative business out of serving the needs of those very customers.

DigitalOcean offers inexpensive options, transparent pricing, highly personalized service, and a simple dashboard that makes deploying cloud tools easy. These features are ideal for smaller companies with limited financial and technical resources, and the company is now applying that successful blueprint to help its customers deploy AI.

It operates data centers fitted with advanced graphics processing units (GPUs) from leading chipmakers like Nvidia and Advanced Micro Devices. But unlike the larger cloud providers, which focus on deals that involve leasing each customer access to thousands of those chips, DigitalOcean offers fractional capacity, allowing a business to start with access to just one GPU and scale up as needed.

This is perfect for small AI workloads like deploying a customer service chatbot on a website, or extracting valuable insights from small data sets.

DigitalOcean also offers a cloud-based workspace called Gradient, where SMBs can tap into ready-made large language models (LLMs) from third-party developers like Anthropic in order to accelerate their AI software projects.

DigitalOcean generated $229.6 million in revenue during the third quarter, which was a 16% increase from the prior-year period. It marked an acceleration from the company's second-quarter growth of 14%, and that momentum was driven by AI revenue that more than doubled for the fifth-straight quarter.

DigitalOcean's platform is becoming a popular destination for businesses looking to build and scale their AI workloads, and they are spending significant amounts of money to do it. For example, it ended Q3 with $110 million in annual recurring revenue solely from customers who are spending at least $1 million per year with the company. That figure was up by 72% from the year-ago period.

Here's the most impressive part about DigitalOcean's Q3 momentum: It wasn't fueled by a significant increase in growth-oriented spending -- in fact, the company's total operating expenses were flat year over year.

With revenue growth accelerating and costs holding steady, DigitalOcean's net income surged by 381% to $158.3 million during the quarter on a generally accepted accounting principles (GAAP) basis. The bottom line was boosted by a couple of one-off tax and financing benefits that together contributed over $116 million, but even after stripping those out, the company still delivered an adjusted profit of $57.3 million, which was up 8% year over year.

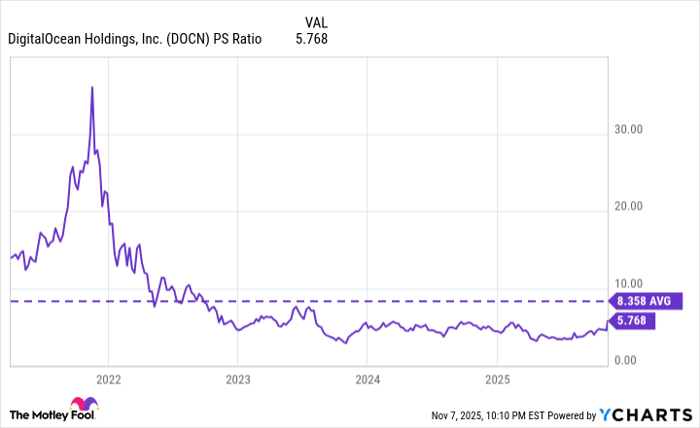

DigitalOcean stock has soared by 44% this year, but it's still trading at an attractive valuation. Based on the company's trailing 12-month revenue of $863.9 million, its price-to-sales (P/S) ratio is just 5.9, which is a 29% discount to its average P/S ratio of 8.3 since the company went public in 2021.

DOCN PS Ratio data by YCharts.

Based on DigitalOcean's trailing 12-month non-GAAP earnings of $2.18 per share, its stock also trades at a price-to-earnings (P/E) ratio of just 23.7. That's cheaper than both the technology-focused Nasdaq-100 index, which trades at a P/E ratio of 33.6, or the S&P 500, which trades at a P/E ratio of 25.7.

No matter how you slice it, DigitalOcean stock looks like a bargain right now, especially in light of the company's accelerating revenue growth with surging contributions from high-value AI customers. Plus, the company values its total addressable market at $140 billion this year alone. It has barely scratched the surface of that opportunity.

As of midday Monday, the stock was trading at around $51.67. But Bank of America recently increased its price target for DigitalOcean stock from $34 to $60, and Canaccord Genuity also upped its target to $60. With top Wall Street institutions starting to take notice of this stock, it could be poised for another great performance in 2026.

Before you buy stock in DigitalOcean, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and DigitalOcean wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $595,194!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,153,334!*

Now, it’s worth noting Stock Advisor’s total average return is 1,036% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 10, 2025

Bank of America is an advertising partner of Motley Fool Money. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, DigitalOcean, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| Jul-28 | |

| Jul-24 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-07 | |

| Jul-07 | |

| Jul-06 | |

| Jul-02 | |

| Jun-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite