|

|

|

|

|||||

|

|

|

Primoris Services Corporation PRIM has been witnessing robust demand trends across power delivery, gas operations, communications, renewable energy and industrial markets. Continued favor from the increased public infrastructure spending is fueling this fire. These favorable fundamentals have not only boosted the firm’s top-line growth but also ensured bottom-line scale, despite existing inflationary pressures.

PRIM ended the third quarter of 2025 with adjusted earnings per share (EPS) of $1.88, which were up 54.1% from $1.22 per share reported in the year-ago quarter. This incremental growth was favored by increased leverage from revenue growth, alongside lower interest expense and selling, general and administrative (SG&A) expenses because of its cost control efforts. The consolidated revenues in the quarter grew year over year by 32.1%, while the interest and SG&A expenses decreased by 61.1% and 0.4%, respectively. (read more: Primoris Q3 Earnings & Revenues Beat Estimates, '25 View Up)

Notably, the passing of the One Big Beautiful Bill Act is currently acting as a catalyst for the ongoing market trends. The act highlights tax incentives like bonus depreciation across infrastructure investments and allocates about $150 billion of mandatory defense spending. This strategic move is in favor of Primoris Services as it has enabled its customers to have a substantial volume of projects lined up for the next few years. The prospective backlog growth trends are indeed favorable for PRIM’s bottom-line growth in the near and long term.

Thus, owing to the robust market trends and its effective cost control measures, PRIM moved up its 2025 adjusted EPS outlook to the range of $5.35-$5.55, up from the previously expected range of $4.90-$5.10. The revised estimated range compares favorably with the adjusted EPS of $3.87 reported in 2024.

Although the Zacks Consensus Estimate for 2025 and 2026 earnings has remained unchanged over the past 60 days, it indicates year-over-year growth of 31.3% and 9.3%, respectively.

The favorable year-over-year comparisons indicate that PRIM will be able to capitalize on its in-house business strategies and ensure incremental prospects amid favorable market fundamentals.

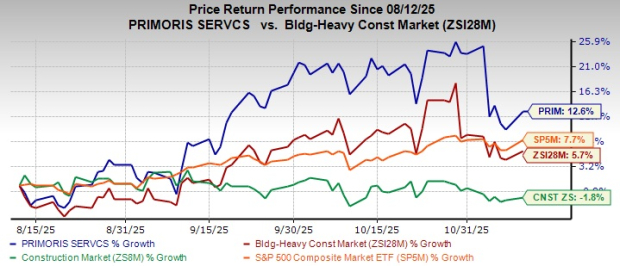

Shares of this Texas-based specialty construction and infrastructure company have moved up 12.6% in the past three months, outperforming the Zacks Building Products - Heavy Construction industry, the broader Zacks Construction sector and the S&P 500 index.

Moreover, firms like MasTec, Inc. MTZ and Jacobs Solutions Inc. J offer substantial competition to Primoris Services in the public infrastructure field, especially across pipelines, telecom, utility markets, and in engineering and construction services. In the past three months, shares of MasTec and Jacobs Solutions have gained 9.1% and 3%, respectively.

PRIM stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 23.51, as evidenced by the chart below.

Notably, MasTec and Jacobs Solutions are currently trading at a forward 12-month P/E ratio of 25.68 and 21.82, respectively.

Primoris stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite