|

|

|

|

|||||

|

|

|

Torrid’s stock price has taken a beating over the past six months, shedding 79.3% of its value and falling to $1.15 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Torrid, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons you should be careful with CURV and a stock we'd rather own.

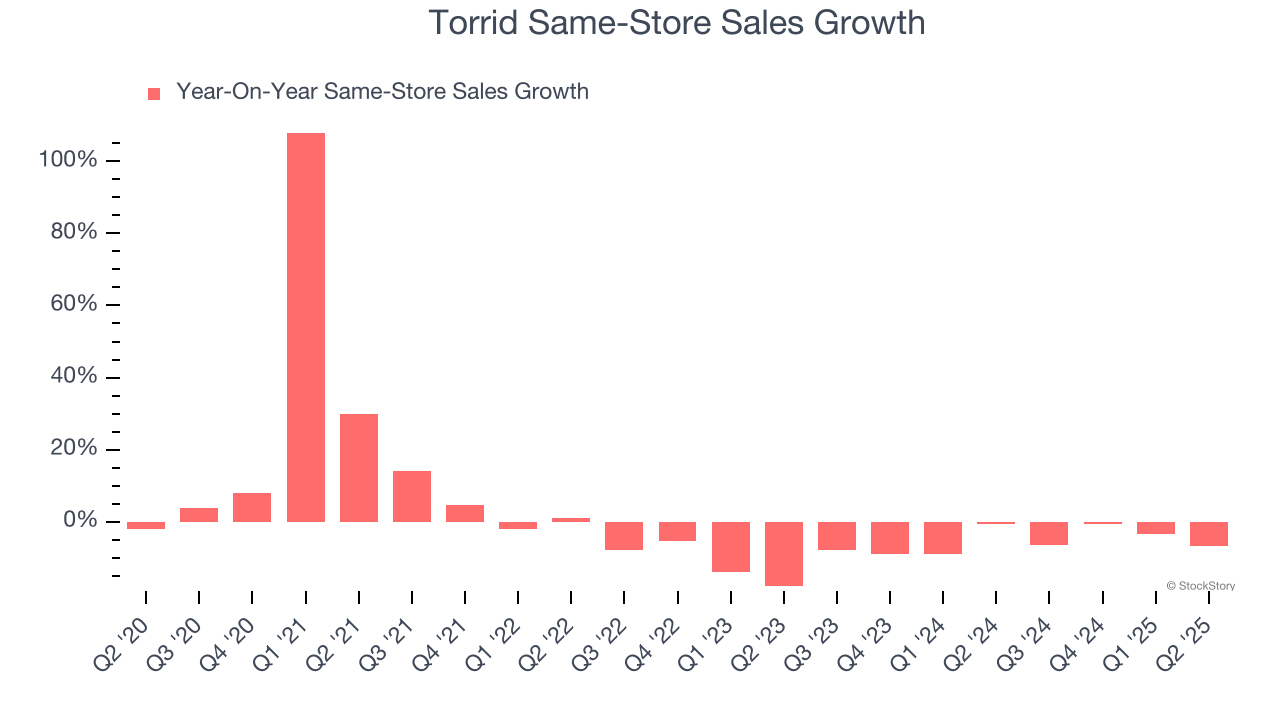

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Torrid’s demand has been shrinking over the last two years as its same-store sales have averaged 5.6% annual declines.

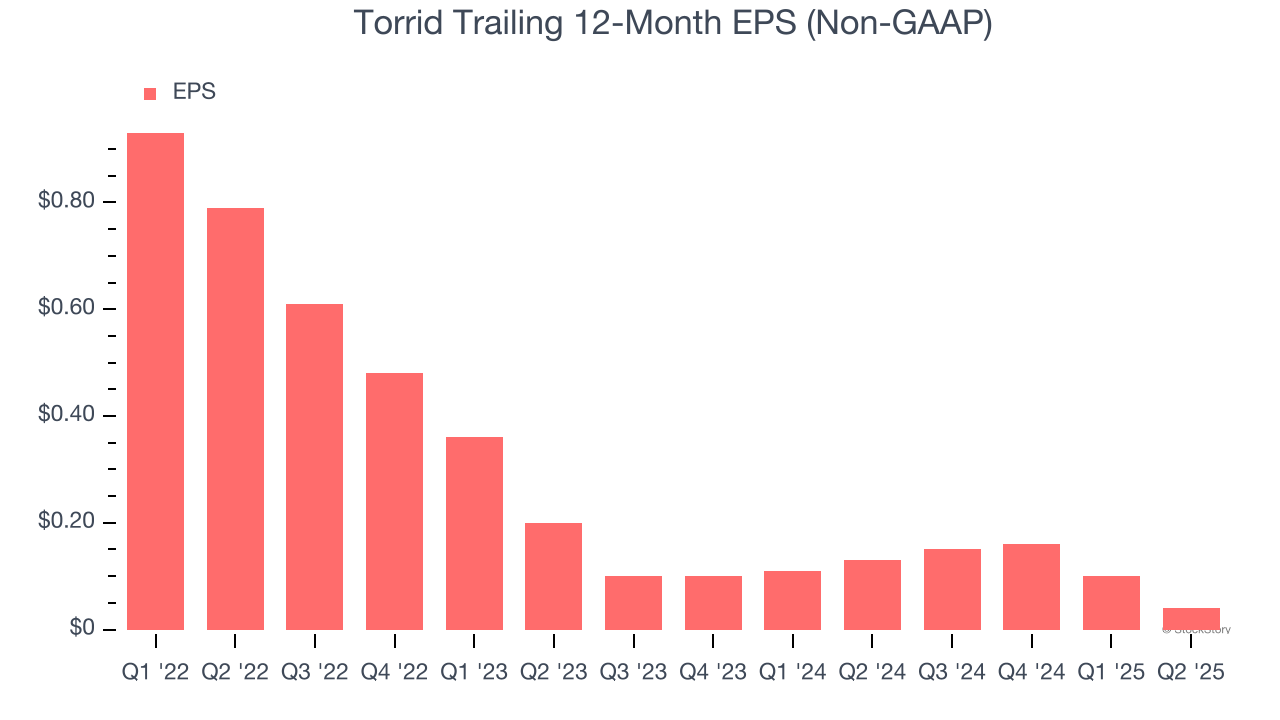

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Torrid’s full-year EPS dropped significantly over the last three years. In a mature sector such as consumer retail, we tend to steer our readers away from companies with falling EPS because it could imply changing secular trends and preferences. If the tide turns unexpectedly, Torrid’s low margin of safety could leave its stock price susceptible to large downswings.

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Torrid historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 2.2%, lower than the typical cost of capital (how much it costs to raise money) for consumer retail companies.

Torrid doesn’t pass our quality test. Following the recent decline, the stock trades at 20.6× forward P/E (or $1.15 per share). At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Fresh US-China trade tensions just tanked stocks—but strong bank earnings are fueling a sharp rebound. Don’t miss the bounce.

Don’t let fear keep you from great opportunities and take a look at Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Aug-05 | |

| Jun-05 | |

| Jun-04 | |

| Jun-04 | |

| May-21 | |

| Mar-24 | |

| Mar-20 | |

| Mar-19 | |

| Mar-19 | |

| Mar-19 | |

| Mar-19 | |

| Mar-18 | |

| Mar-05 | |

| Feb-26 | |

| Feb-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite