|

|

|

|

|||||

|

|

|

Over the past six months, PennyMac Financial Services has been a great trade, beating the S&P 500 by 11.6%. Its stock price has climbed to $127.26, representing a healthy 28.5% increase. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Following the strength, is PFSI a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free for active Edge members.

Founded during the 2008 financial crisis to help address the mortgage market meltdown, PennyMac Financial Services (NYSE:PFSI) is a specialty financial services company that originates, services, and manages investments related to residential mortgage loans in the United States.

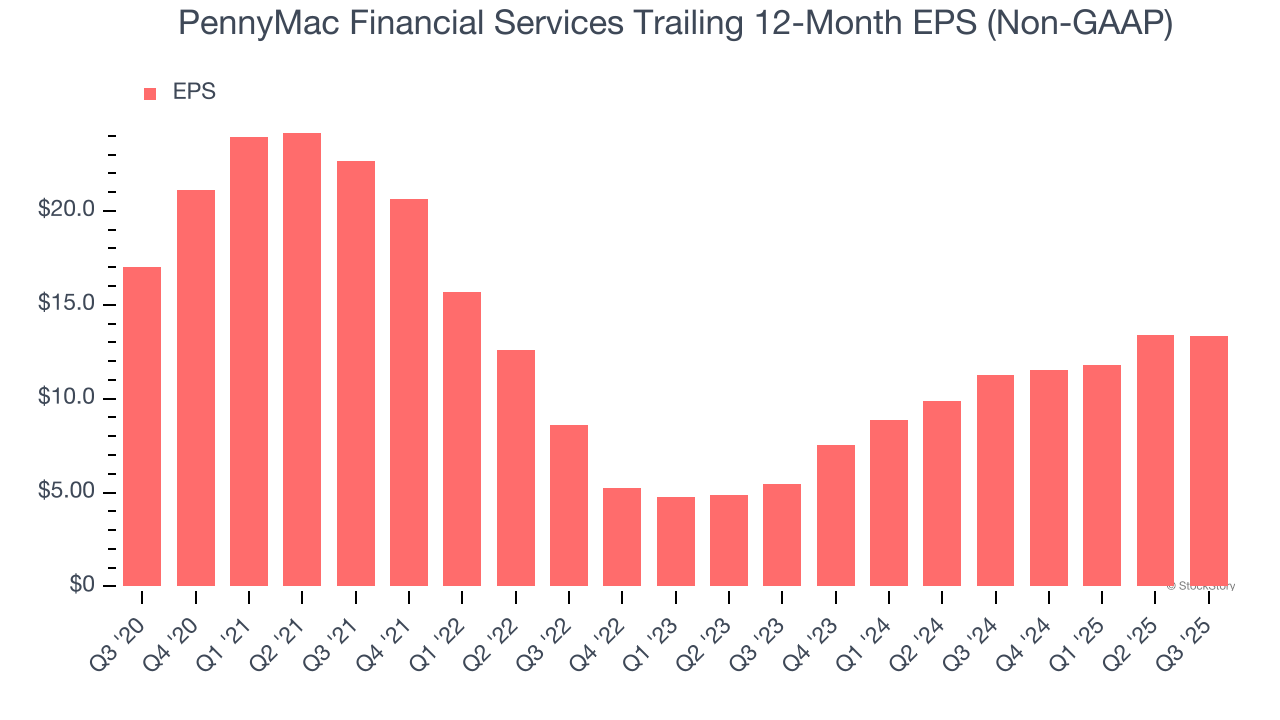

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

PennyMac Financial Services’s EPS grew at an astounding 56.3% compounded annual growth rate over the last two years, higher than its 20.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

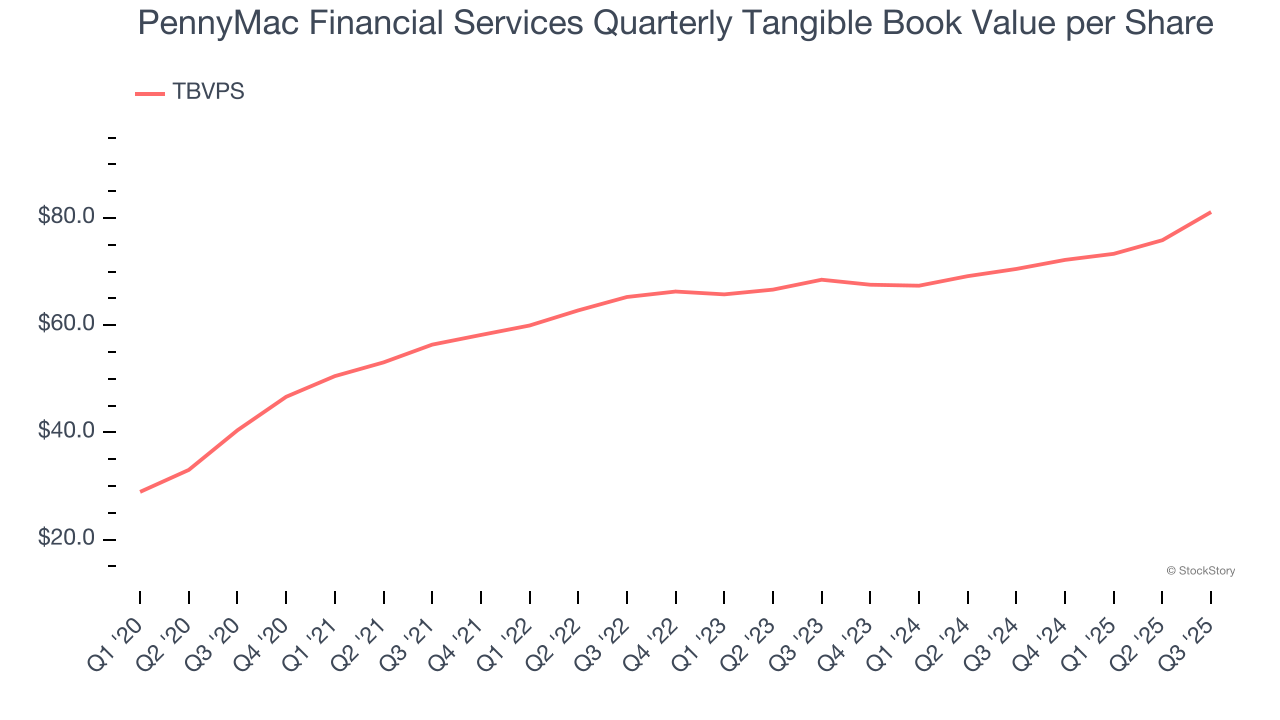

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

Although PennyMac Financial Services’s TBVPS increased by 15% annually over the last five years, growth has recently decelerated to a mediocre 8.8% over the past two years (from $68.49 to $81.12 per share).

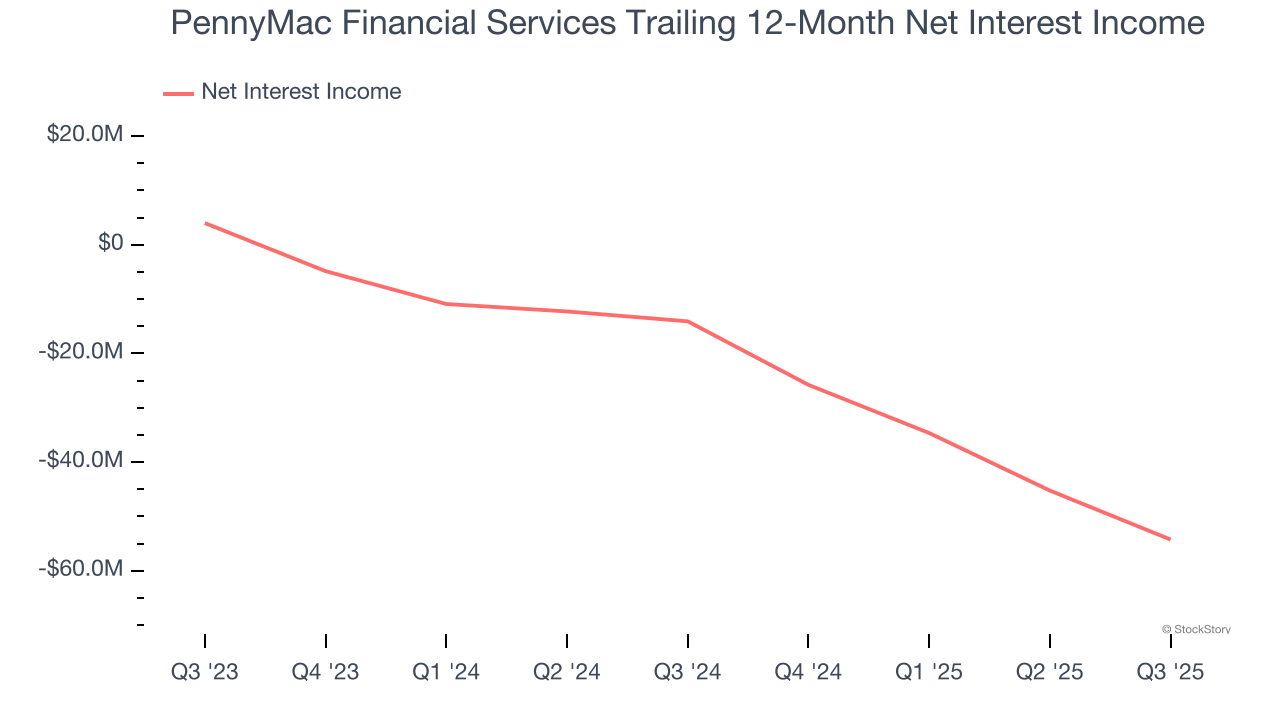

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

PennyMac Financial Services’s net interest income has grown at a 7.1% annualized rate over the last five years, slightly worse than the broader banking industry.

PennyMac Financial Services’s positive characteristics outweigh the negatives, and with its shares topping the market in recent months, the stock trades at 1.5× forward P/B (or $127.26 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free for active Edge members .

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jul-14 | |

| Jul-14 | |

| Jun-17 | |

| Jun-16 | |

| Jun-16 | |

| Jun-16 | |

| Jun-09 | |

| May-14 | |

| May-06 | |

| May-05 | |

| May-05 | |

| May-05 | |

| May-05 | |

| Apr-21 | |

| Apr-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite