|

|

|

|

|||||

|

|

|

The Home Depot, Inc. HD is set to report third-quarter fiscal 2025 results on Nov. 18, before market open. The company’s top and bottom lines are expected to have increased year over year in the to-be-reported quarter. The Zacks Consensus Estimate for fiscal third-quarter revenues is pegged at $41.1 billion, indicating growth of 2.2% from that reported in the year-ago quarter.

The Zacks Consensus Estimate for quarterly earnings per share (EPS) of $3.82 suggests growth of 1.1% from the year-ago period’s reported figure. The consensus estimate for EPS has moved down 0.5% in the past seven days.

The Atlanta, GA-based leading home improvement retailer delivered a trailing four-quarter average earnings surprise of 1.3%. In the last reported quarter, the company delivered a negative earnings surprise of 0.6%.

Our proven model does not conclusively predict an earnings beat for Home Depot this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that is not the case here. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Home Depot has an Earnings ESP of -0.28% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Home Depot’s third-quarter fiscal 2025 results are expected to reflect top-line and comparable sales (comps) growth, driven by higher-value purchases and steady demand from both Pro and DIY customers. A greater mix of higher-value items, inflation in core commodities such as lumber and copper, and slightly lower promotional activity are expected to have aided ticket growth. The company is advancing its "One Home Depot" plan, focusing on supply-chain expansion, technology investments and digital enhancements. The interconnected retail strategy remains a key growth driver, ensuring a seamless shopping experience.

Our model predicts comps to increase 2.1% in the third quarter of fiscal 2025, with a 1.2% increase in customer transactions and a 0.9% rise in average ticket.

With a vast store network, a comprehensive product offering and a growing online presence, HD is well-positioned to meet evolving consumer demands. Its interconnected retail model and strong tech infrastructure have driven web traffic and supported the buildout of a scalable Pro ecosystem, solidifying its competitive advantage. On the last reported quarter’s earnings call, Home Depot predicted a resilient customer base, strong market position and ongoing investments to enable market share growth and sustain profitability.

However, the company continues to grapple with ongoing challenges, including softened demand and pressure in high-ticket discretionary categories, factors that have impacted both total and comparable sales. Macroeconomic pressures are also weighing on profitability. Elevated interest rates continue to influence consumer behavior and financing expenses. The company expects net interest expenses to increase year over year in the near term.

The Home Depot, Inc. price-eps-surprise | The Home Depot, Inc. Quote

Home Depot has been seeing soft engagement for big-ticket discretionary categories, such as kitchen and bath remodels, as higher interest rates discouraged financing-dependent projects. With no major improvement expected in interest rates or housing turnover in 2025, the company anticipates continued pressure on big-ticket renovations, such as kitchen and bath remodels.

While Pro sales have been strong, the shift in consumer spending toward smaller-scale repairs and maintenance projects suggests that larger project demand may not rebound meaningfully in the near term, limiting growth potential in high-margin categories. The integration of acquisitions, like SRS and GMS, is expected to add amortization and transition costs, temporarily depressing margins. In a competitive retail environment where price leadership is the key, Home Depot may face difficulty balancing cost pressures with the need to maintain value for customers.

Our model predicts a gross margin of 33.5% for the fiscal third quarter, up just 10 bps year over year. We expect adjusted operating income to increase 2% in the fiscal third quarter, with a flat operating margin of 13.8%.

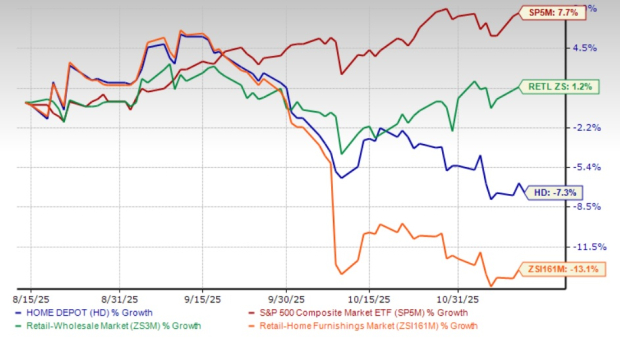

Home Depot’s shares have lost 7.3% in the past three months, but compared favorably with the industry’s 13.1% decline. However, the HD stock has lagged the S&P 500 and the Retail-Wholesale sector’s growth of 7.7% and 1.2%, respectively, in the same period.

The Home Depot stock has outpaced its arch-rival Lowe’s Companies Inc. LOW and Floor & Decor’s FND decline of 7.3% and 23.4%, respectively, in the past three months. Meanwhile, shares of competitor FGI Industries FGI recorded significant growth of 43.3% in the same period.

At the current price of $371.13, HD trades 15.5% below its 52-week high mark of $439.37, reflecting an upside potential.

Home Depot’s current valuation appears quite pricey. The company trades at a forward 12-month P/E multiple of 23.21X, exceeding the industry average of 21.14X and below the S&P 500’s average of 23.74X.

Given the premium valuation, investors may face significant risks if the company's future performance does not meet expectations. The retail market is becoming increasingly competitive and Home Depot’s initiatives may not suffice to drive significant growth. Macroeconomic challenges and heightened competition can impede the company's ability to sustain its current growth trajectory.

Home Depot continues to demonstrate solid revenue growth and profitability, driven by its dominant position in the home improvement industry and the effective execution of its “One Home Depot” strategy. Strategic investments in digital infrastructure, supply-chain optimization and in-store technology have strengthened its ability to serve both do-it-yourself consumers and professional contractors with speed and efficiency.

The company’s integrated model, seamlessly connecting physical stores with a powerful online platform, has enhanced customer experience and boosted digital engagement. Its expanding Pro ecosystem, bolstered by the acquisition of SRS Distribution, further reinforces Home Depot’s leadership in building materials and its appeal among trade professionals.

Although short-term headwinds such as softer discretionary spending and macroeconomic uncertainty may temper near-term growth, Home Depot’s market leadership, operational discipline and innovation-driven approach position it strongly for long-term value creation. The company remains well-equipped to capture opportunities as home improvement demand normalizes and professional project activity rebounds.

As Home Depot heads into its third-quarter fiscal 2025 earnings release, investors are keen to see if the retail giant can meet expectations amid a mixed consumer backdrop. The company’s strong market leadership, progress under the “One Home Depot” strategy, and consistent growth within its Pro customer segment are encouraging indicators, though potential macroeconomic and demand-related risks remain in focus. Assessing these dynamics will be crucial for gauging the stock’s near-term direction.

While the long-term story remains attractive, adopting a patient stance may be wise until post-earnings clarity emerges. For existing shareholders, holding positions seems reasonable, as the results are likely to reaffirm Home Depot’s operational strength and strategic discipline. In a shifting retail environment defined by changing consumer preferences and economic uncertainty, Home Depot’s reliable execution, expanding Pro ecosystem, and continued digital advancement make it a resilient and closely watched name for the quarters ahead.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 9 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite