|

|

|

|

|||||

|

|

|

Shares of Citigroup, Inc. C have jumped 55.1% in the past year, outperforming the industry’s growth of 33.2%. Its peers, Wells Fargo WFC and Bank of America BAC, rose 21% and 20.6%, respectively, over the same time frame.

Price Performance

Given such a strong rally, investors are now wondering if the upside is largely behind it, or if there is still a compelling case to own Citigroup stock? Let us discuss factors at play and decide its investment worthiness.

The company continues to advance its multi-year strategy to streamline operations and focus on its core businesses. Since announcing plans in April 2021 to exit consumer banking in 14 markets across Asia and EMEA, the company has completed its exit in nine countries.

In September 2025, Citigroup announced an agreement to sell a 25% stake in Banamex to Mexican business leader Fernando Chico Pardo, reaching a milestone toward full divestiture and deconsolidation of Banamex. The bank is also progressing with the wind-down of its Korean consumer banking operations, the exit from Russia, and preparations for an IPO of its Mexican consumer, small business, and middle-market banking operations. These initiatives will free up capital and help the company pursue investments in wealth management and investment banking (IB) operations, which will stoke fee income growth.

CEO Jane Fraser highlighted during the third-quarter 2025 earnings call that the consistent execution of Citigroup’s transformation strategy has improved the business performance, boosted returns, and strengthened its competitive position. The company’s efforts are already paying off as both wealth management revenues and IB revenues rose 17% year over year in the first nine months of 2025.

Looking ahead, Citigroup expects total revenues to exceed $84 billion in 2025, with revenue growth projected at a 4–5% CAGR through 2026.

C has been emphasizing leaner, streamlined operations to reduce expenses. Pursuant to this, the company changed its operating model and the leadership structure. This resulted in a streamlined and straightforward management structure aligned with and supporting the bank's strategy of increased spans of control and significantly reduced bureaucracy and unnecessary complexity.

In January 2024, Citigroup announced plans to cut 20,000 jobs or 8% of its global staff by 2026. The bank had already made significant progress by reducing its headcount by more than 10,000 employees.

The company also continues to focus on streamlining processes and platforms and driving automation to reduce manual touchpoints. Citigroup is increasingly deploying artificial intelligence (AI) tools to support these efforts. During the third-quarter earnings call, management stated that its nearly 180,000 workforce across 83 countries now uses proprietary AI tools, reflecting broad adoption of technology that supports real-time, cross-border payment and settlement capabilities.

Given such efforts, the company expects to achieve $2-2.5 billion in annualized run rate savings by 2026. For 2026, expenses are expected to be below $53 billion, excluding FDIC fees, indicating a decline from the $56.4 billion reported in 2023.

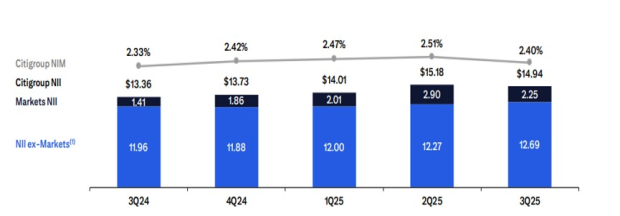

The Federal Reserve rates twice this year, following a 100-basis-point cut in 2024. Given this, the company’s net interest income (NII) has been improving since the third quarter of 2024. In the first nine months of 2025, Citigroup's NII rose 9% year over year.

Net Interest Income

Going forward, stabilizing funding costs and improving loan demand will continue to aid C’s NII expansion in the upcoming period.

Following the solid NII performance till September 2025, management raised its projection for NII (excluding Markets) for 2025. The metric is expected to increase 5.5%, up from the prior mentioned 4% rise.

C is broadening its presence in the lucrative private lending business through collaborations. In sync with this, in September 2025, Citigroup launched an $80-billion customized portfolio offering with BlackRock Inc., providing clients with tailored exposure across public and private markets. In June 2025, the company announced a partnership with Carlyle Group to expand asset-based private credit opportunities in the fintech specialty lending space. The collaboration combines Carlyle’s structuring expertise with Citigroup’s SPRINT (Spread Products Investment in Technologies) team and market reach to co-invest in tailored financing solutions.

In September 2024, it partnered with Apollo Global Management to launch a $25-billion private credit direct lending program, initially focused on North America, with potential global expansion. This program combines the company’s banking reach with Apollo’s capital strength to meet rising corporate financing demand. These collaborations aim to diversify Citigroup’s revenues and deepen client engagement.

C enjoys a strong liquidity position. As of Sept. 30, 2025, cash and due from banks and total investments aggregated to $474.3 billion, while its total debt (short-term and long-term borrowing) was $370.6 billion.

Post-clearing the 2025 Fed stress test, the company hiked its dividend 7.1% to 60 cents per share. In the past five years, it has raised its dividends three times. It has a payout ratio of 33%. It has a dividend yield of 2.1%. Wells Fargo has raised its dividend six times in the past five years, while Bank of America has increased its dividend five times in the past five years.

In January 2025, Citigroup's board of directors approved a $20-billion common stock repurchase program with no expiration date. As of Sept. 30, 2025, $11.3 billion worth of authorization remained available. Supported by a strong capital and liquidity position, its capital distribution activities seem sustainable.

Solid revenue growth, the acceleration of its transformation strategy, and an optimistic outlook indicate that Citigroup is well-positioned for sustainable long-term growth. With solid revenue momentum, disciplined cost control, and expanding partnerships in private lending, Citigroup is positioning itself for sustainable long-term growth.

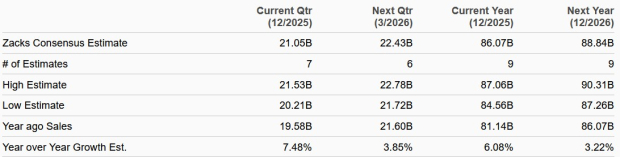

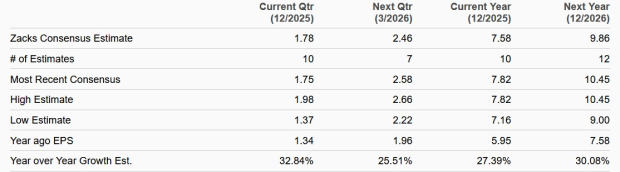

The Zacks Consensus Estimate for C’s 2025 and 2026 earnings implies year-over-year rallies of 27.4% and 30.1%, respectively. The Zacks Consensus Estimate for C’s 2025 and 2026 sales indicates year-over-year increases of 6.1% and 3.2%, respectively.

Sales Estimates

Earnings Estimates

While risks remain, including credit quality pressures and execution challenges related to large-scale restructuring, management reaffirmed its commitment to disciplined capital return via increased share repurchases and regular dividends, while improving returns over time. The company is aiming for a 10-11% return on tangible equity by 2026 amid ongoing regulatory and macroeconomic challenges.

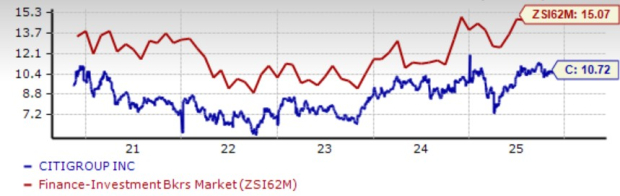

From a valuation standpoint, C appears inexpensive relative to the industry. It is currently trading at a discount with a forward 12-month price-to-earnings (P/E) of 10.72X, well below the industry average of 15.07X. Further, Bank of America is trading at a 12-month forward P/E of 12.69X, while Wells Fargo is trading at 12.6X.

Price-to-Earnings F12M

As such, investors can consider retaining the C stock for now to generate a healthy long-term return. Citigroup currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 41 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 9 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite