|

|

|

|

|||||

|

|

|

Plug Power is a leader in the hydrogen fuel cell market.

While revenue has grown substantially, the company has incurred massive operational losses.

Plug is building an end-to-end green hydrogen ecosystem, but mainstream adoption could be a decade or two away.

Plug Power (NASDAQ: PLUG) is a pioneer in the commercialization of hydrogen fuel cell technology. The company has deployed more than 72,000 fuel cell systems and 275 fueling stations. Plug Power claims it operates the largest green hydrogen plant in the United States, which supplies corporate giants such as Walmart, Amazon, and Home Depot. The company's vision is to build the world's first vertically integrated hydrogen ecosystem, with the overarching goal of making green hydrogen a mainstream energy source.

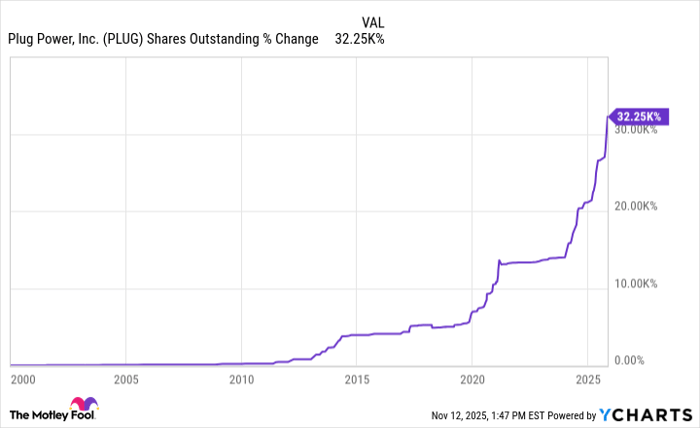

If that's all you knew about Plug Power, you'd probably wonder why it's a penny stock. The short answer is the company has been losing money hand over fist while leading the "green hydrogen revolution," which may or may not ever come to fruition. Meanwhile, Plug Power's outstanding share count has ballooned by 32,000% since it became a publicly traded company in October 1999, diluting shares into oblivion.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

PLUG Shares Outstanding data by YCharts

Despite Plug Power's staggering losses, management is targeting positive operating income by 2027 and overall profitability by 2028. Although top-line growth has been choppy, annual revenue is up 879% over the past decade. Also, the company recently announced plans to pursue more business in the booming artificial intelligence (AI) data center market, which could turbocharge Plug Power's growth. With the share price under $3 as of this writing, should you consider starting a position?

Image source: Getty Images.

Hydrogen is the most abundant element in the universe, and it's long been touted as a next-generation clean energy source. When hydrogen is consumed in a fuel cell, its only byproduct is water vapor. Hydrogen can be used to power fuel cell electric vehicles, store excess renewable energy, and generate electricity and heat. But today it's mainly used in petroleum refining, fertilizer production, and other industrial processes.

To be converted to an energy source, hydrogen must be purified and extracted. While there are several ways to do that, the vast majority of hydrogen is produced using natural gas or coal. In the U.S., 95% of hydrogen is produced from steam reforming of natural gas. When Plug Power talks about green hydrogen, it's referring to a process called electrolysis, in which water is split into hydrogen and oxygen using electricity generated from renewable sources like wind or solar power.

While green hydrogen sounds great in theory, it has one massive barrier to adoption: cost. A 2024 Columbia Business School report found that "gray" hydrogen -- hydrogen made from natural gas steam methane reforming -- costs between $1 and $3 per kilogram to produce, while green hydrogen costs between $4 and $12 per kilogram to produce.

Even with global production of green hydrogen increasing 10% in 2024, it still accounted for less than 1% of total hydrogen output. Given the "current emphasis on affordability," widespread adoption of green hydrogen and other alternative fuels likely won't happen until after 2040, according to a new McKinsey & Company report. That puts Plug Power in a tough spot.

Plug Power reported 2024 net revenue of $628.8 million, a 29% year-over-year decline. Meanwhile, the company's net loss increased 54% to $2.1 billion.

As bad as those numbers look on paper, management called 2024 a "a year of strong execution and meaningful strategic progress," touting a 34% decrease in operating-cash-flow burn. As part of Project Quantum Leap, the company is targeting $150 million to $200 million in annual cost savings through job cuts, facility consolidations, capital expenditure restrictions, supply chain efficiencies, and other measures.

While third-quarter revenue growth fell short of analysts' expectations, Plug made progress on other fronts. Net cash used in operating activities was down 49% compared to the year-ago quarter. Management said the company is on track to achieve positive earnings before interest, taxes, depreciation, and amortization (EBITDA) by the second half of 2026, en route to overall profitability by 2028.

Going forward, Plug Power plans to focus production on three key areas: fuel cells for material handling applications, electrolyzers, and hydrogen fuel. Electrolyzers, which enable businesses to produce their own hydrogen, have been a bright spot. Through Sept. 30, year-over-year sales of the GenEco electrolyzer were up 33%, and management expects a record $200 million in full-year sales.

While there are plenty of reasons to be wary of Plug Power as an investment, there is something you might want to keep your eye on. On Nov. 10, the company said it signed a non-binding letter of intent with a major U.S. data center developer to monetize its electricity rights in New York and another location. The deal will generate more than $275 million in much-needed liquidity for Plug Power, but the bigger news for investors is that Plug is exploring opportunities to provide auxiliary and backup power for data centers via its fuel cell technology.

Given the slow adoption of green hydrogen and the uncertainty surrounding that market, I can't recommend investing in Plug Power now. But if the company can carve a niche in the booming AI data center market, Plug Power might merit another look.

Before you buy stock in Plug Power, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Plug Power wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $599,784!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,165,716!*

Now, it’s worth noting Stock Advisor’s total average return is 1,035% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 10, 2025

Josh Cable has positions in Amazon. The Motley Fool has positions in and recommends Amazon, Home Depot, and Walmart. The Motley Fool has a disclosure policy.

| 31 min | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 11 hours | |

| Jul-19 | |

| Jul-19 | |

| Jul-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite