|

|

|

|

|||||

|

|

|

Mastercard Incorporated MA has once again showcased a strong quarterly performance, continuing its impressive streak of mid- to high-teens revenue growth, thanks to resilient consumer spending and robust cross-border activity. In the third quarter of 2025, total net revenues rose 17% year over year. The company benefited from broad-based volume gains, with cross-border travel demand standing out as a key driver. Switched transactions have steadily increased as digital payments have become more prevalent worldwide.

Additionally, Mastercard’s Service segment — covering cybersecurity, data analytics and fraud solutions — has contributed to a significant layer of diversified, high-margin growth, enhancing overall profitability. In third-quarter 2025, value-added services and solutions reported net revenue growth of 25% year over year.

Even though things are looking positive, the road ahead might not be as straightforward as it seems. Regulatory scrutiny continues to be a significant concern, especially in the United States and Europe. Also, adjusted operating expenses have climbed steadily, up 14.5% year over year in the first nine months of 2025.

Despite the challenges, MA is in a great spot to seize long-term opportunities. It is pouring resources into tokenization, real-time payments, open banking and AI-driven fraud prevention areas that are set to surpass traditional card-based transactions. These efforts not only enhance the company’s significance in the global payments landscape but also broaden its influence in emerging areas like B2B payments, digital identity and modernizing financial infrastructure.

Though maintaining mid-teens revenue growth consistently could be challenging. MA’s wide range of business lines, technology-driven initiatives and strategic partnerships create a promising outlook for long-term success.

Some of MA’s competitors in the fintech space include Visa Inc. V and PayPal Holdings, Inc. PYPL.

Visa is making significant moves in the fintech space by expanding Visa Direct and strengthening its partnerships with fintech companies and banks. In fiscal 2025, Visa witnessed 11% year-over-year growth in net revenues, along with an 8% rise in payments volume.

PayPal is increasingly adopting AI to enhance its platform, leveraging real-time data analysis to strengthen security. PayPal reported 4.5% year-over-year growth in net revenues in the first nine months of 2025, along with a 6% rise in total payment volume.

In the year-to-date period, MA’s shares have gained 3.7% against the industry’s fall of 12.1%.

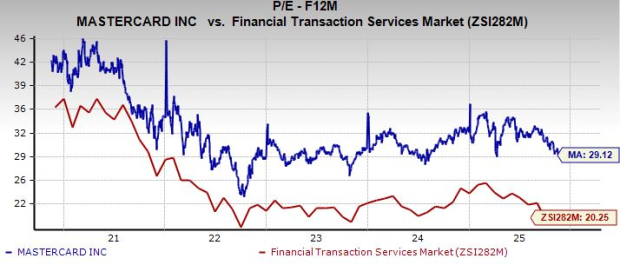

From a valuation standpoint, MA trades at a forward price-to-earnings ratio of 29.12, above the industry average of 20.25. MA carries a Value Score of D.

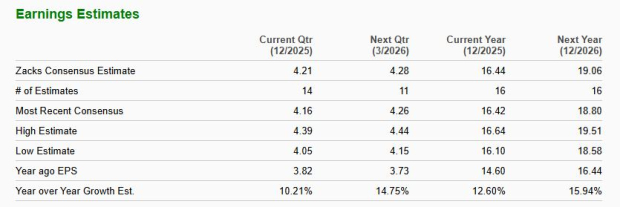

The Zacks Consensus Estimate for Mastercard’s 2025 earnings implies 12.6% growth from the year-ago period.

Mastercard currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 10 hours | |

| 11 hours | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite