|

|

|

|

|||||

|

|

|

What a time it’s been for Lemonade. In the past six months alone, the company’s stock price has increased by a massive 108%, reaching $67.02 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Lemonade, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

We’re happy investors have made money, but we're swiping left on Lemonade for now. Here are three reasons you should be careful with LMND and a stock we'd rather own.

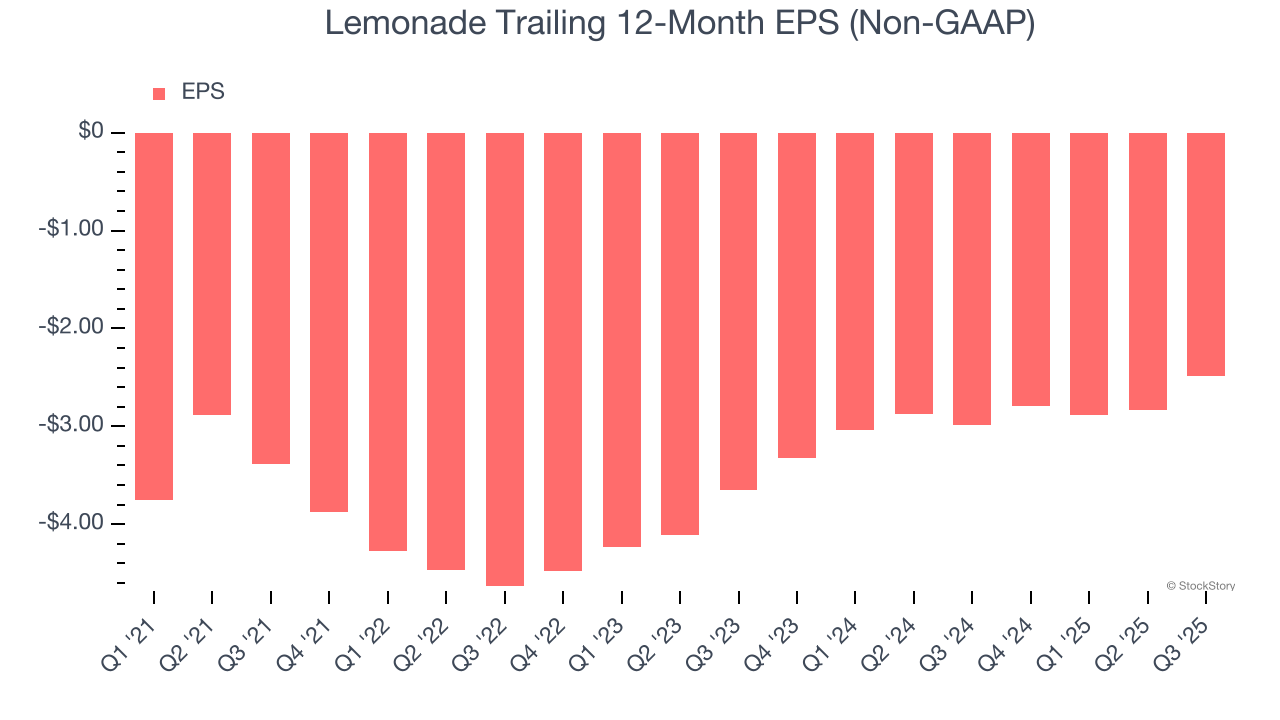

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

For Lemonade, its two-year annual EPS growth of 17.4% was higher than its five-year trend. Its improving earnings is an encouraging data point, but a caveat is that its EPS is still in the red.

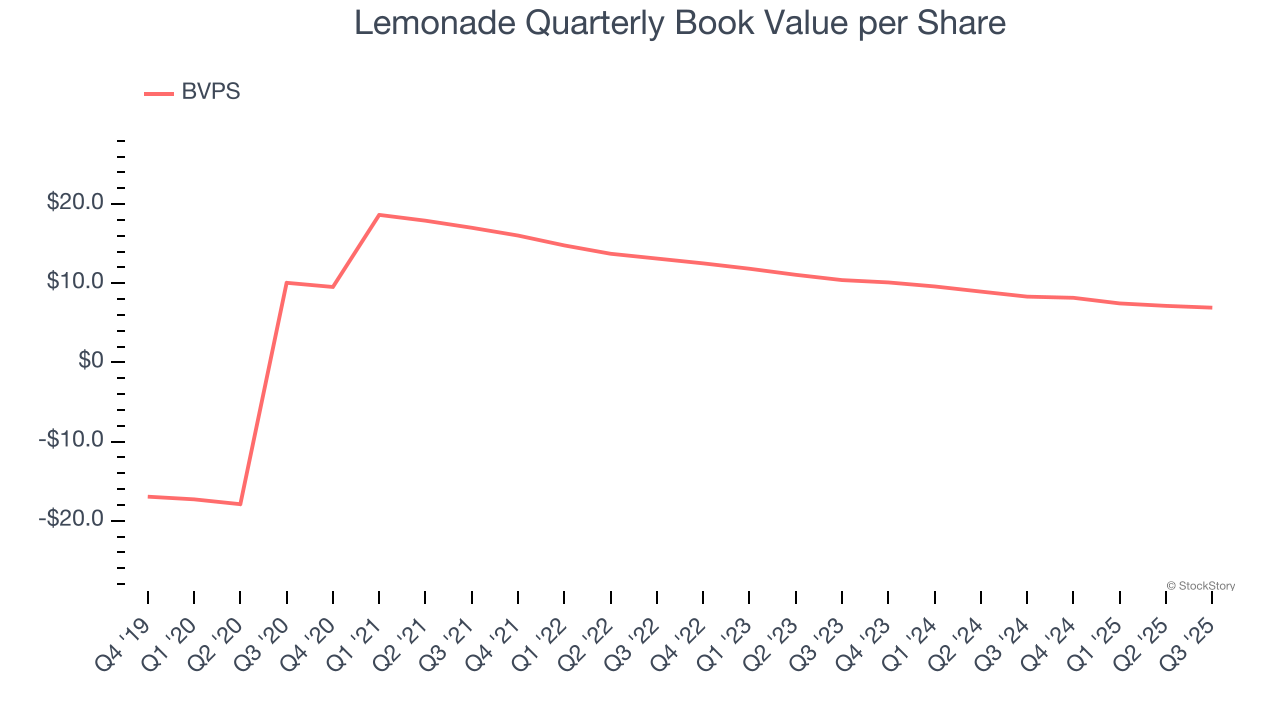

For insurers, book value per share (BVPS) is a vital measure of financial health, representing the total assets available to shareholders after accounting for all liabilities, including policyholder reserves and claims obligations.

To the detriment of investors, Lemonade’s BVPS continued freefalling over the past two years as BVPS declined at a -18.5% annual clip (from $10.40 to $6.91 per share).

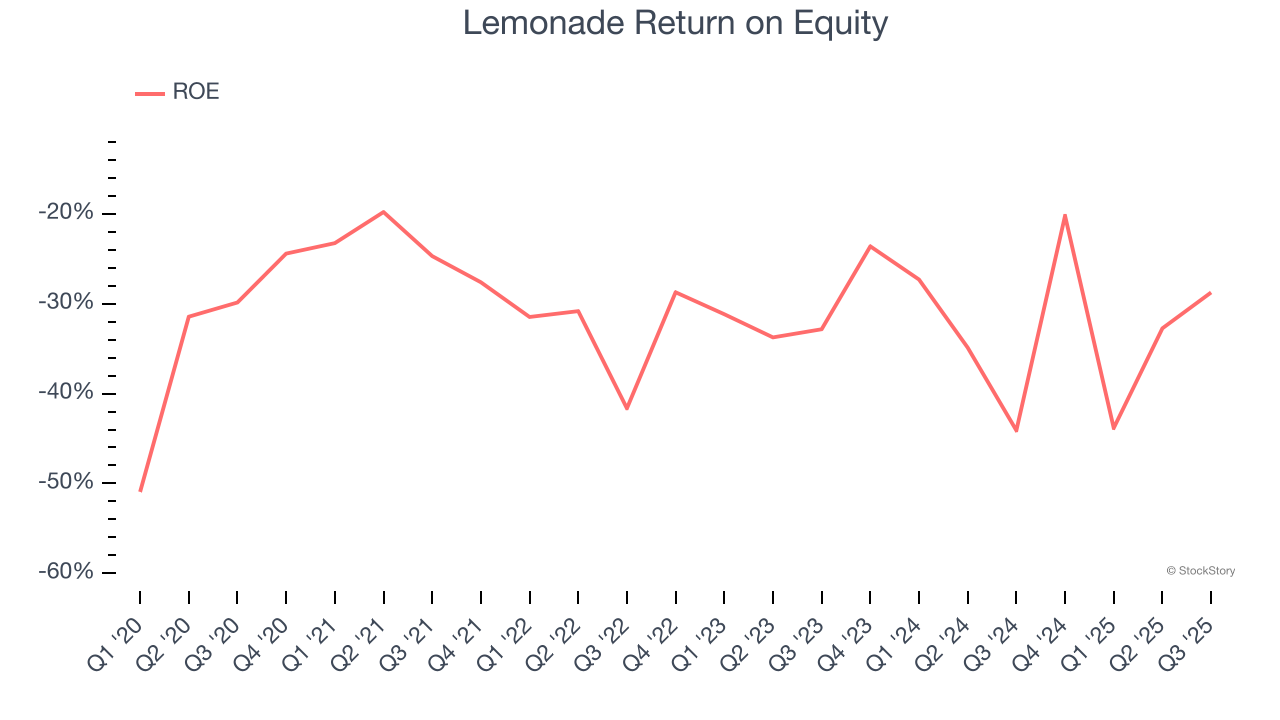

Return on equity, or ROE, represents the ultimate measure of an insurer's effectiveness, quantifying how well it transforms shareholder investments into profits. Over the long term, insurance companies with robust ROE metrics typically deliver superior shareholder returns through a balanced approach to capital management.

Over the last five years, Lemonade has averaged an ROE of negative 30.3%, a bad result not only in absolute terms but also relative to the majority of insurers putting up 20%+. It also shows that Lemonade has little to no competitive moat.

Lemonade isn’t a terrible business, but it doesn’t pass our bar. After the recent rally, the stock trades at 10.4× forward P/B (or $67.02 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward the most dominant software business in the world.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Apr-02 | |

| Mar-23 | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-17 | |

| Mar-05 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-23 | |

| Feb-23 | |

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite