|

|

|

|

|||||

|

|

|

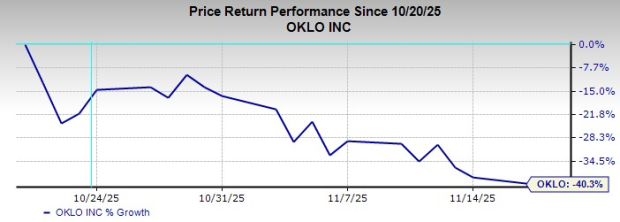

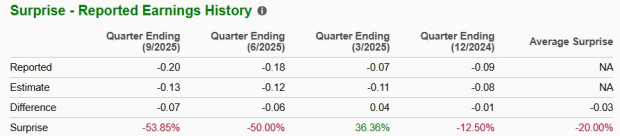

Last week, Oklo Inc. OKLO delivered another disappointing quarter, marking its third miss in the last four reporting periods, and forcing investors to re-evaluate whether the hype-driven rally still makes sense. The stock has also pulled back sharply — down 40% in a month and more than 50% below its 52-week high of $193.84 — a reminder that valuation-driven narratives can unwind quickly when execution lags. With sentiment turning cautious, the key question is straightforward: what should investors do with OKLO after another lackluster earnings report?

OKLO became a market favorite during the AI-energy boom, jumping from a tiny company to one of the most talked-about nuclear stocks. And while the long-term potential of microreactors is still exciting, the current financial picture doesn’t fully support the optimism. This latest miss makes the risk–reward outlook more complicated. Yes, progress with regulators and early customer interest are positives, but they don’t completely ease concerns around estimates, valuation and near-term performance. Add increasing competition from NANO Nuclear Energy NNE and the relative stability investors see in GE Vernova GEV, and OKLO is now at a more challenging turning point.

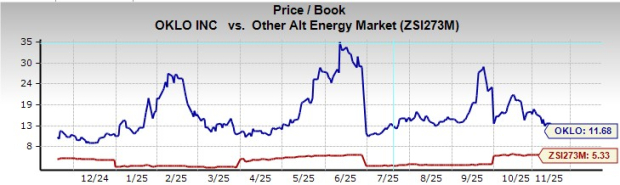

OKLO’s story has always been more about future potential than current fundamentals. The company is still pre-revenue, and its latest quarter reinforced that reality. Loss once again came in broader than expectations, reflecting the operational and developmental hurdles that continue to weigh on near-term performance. The company’s valuation remains elevated relative to any measurable financial metric, and with no commercial revenues expected for years, earnings misses carry an outsized psychological impact.

This dynamic stands in sharp contrast to diversified players like GE Vernova, which has become a favorite among AI-infrastructure investors thanks to its broad energy portfolio and growing earnings base. Meanwhile, NANO Nuclear continues to advance its microreactor ecosystem with a healthy balance sheet, allowing it to pursue development without the same near-term capital strain. As these peers build credibility, OKLO’s execution risks become more visible — particularly with investors now more sensitive to misses and estimate cuts across the sector.

To OKLO’s credit, its regulatory progress with the NRC has been constructive. The company flagged alignment on early-phase review topics and ongoing work on methodology agreements, hazard analyses, and site diligence for its first Aurora powerhouse. These steps matter — and in earlier market conditions, they might have been enough to refresh bullish momentum.

But nuclear licensing is slow, iterative, and unforgiving. Even slight delays in safety-case review can cascade into longer deployment timelines. The company is managing licensing, design engineering, manufacturing planning, and siting all at once, an ambitious approach that brings compounded execution risk. The gap between regulatory traction and commercial readiness remains meaningful, especially when compared with GE Vernova, which has decades of nuclear experience and is already advancing SMR deployment partnerships. For OKLO, the long regulatory runway continues to influence sentiment, particularly after a weak earnings print.

Management emphasized positive inbound interest from AI data-center operators, suggesting strong market appetite for microreactor solutions. While encouraging, OKLO still lacks binding commercial agreements or revenue-backed contracts — a critical missing piece for a capital-intensive nuclear platform. Letters of intent (or LOIs) help build narrative momentum, but they do not create cash flow visibility.

This is an area where NANO Nuclear has positioned itself more strategically, with a broader set of research partnerships and a strong cash position supporting diversified development. Meanwhile, GE Vernova’s involvement across natural gas, nuclear, electrification, and grid technology gives it multiple commercial pathways that OKLO does not yet possess. Investors increasingly want proof of commitment from customers, and the absence of hard agreements keeps OKLO firmly in speculative territory.

Even with nearly $1.2 billion in cash, cash equivalents, and marketable debt securities, OKLO remains exposed to material dilution risk. Large-scale capital projects, including its planned fuel-refinery buildout, will likely require additional equity raises. After raising $460 million through a midyear equity sale and recently filing a $3.5 billion shelf registration, the company is signaling continued reliance on issuing stock to fund its plans. Meanwhile, OKLO’s valuation still trades far above fundamentals, making the stock vulnerable if the sentiment cools.

The latest earnings miss has already pushed estimates lower — a trend that tends to weigh heavily on stocks without revenues. Competition from NANO Nuclear, which boasts a stronger balance sheet, and GE Vernova, which enjoys steady profitability, further highlights the valuation disconnect.

OKLO remains one of the most ambitious players in the next-gen nuclear landscape, but operating losses are deepening. This underscores how challenging the road ahead still is. While regulatory traction and early customer interest create long-term optionality, falling estimates, continued losses and elevated valuation limit near-term upside. The company’s Zacks Rank #4 (Sell) reflects this shift, due to negative estimate revisions and execution uncertainty. For now, OKLO looks like a high-risk, sentiment-ridden stock where volatility is likely to persist, making it appropriate only for investors comfortable with substantial downside alongside the long-term potential.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| Apr-15 | |

| Apr-15 | |

| Apr-14 | |

| Apr-14 | |

| Apr-14 | |

| Apr-13 | |

| Apr-13 | |

| Apr-13 | |

| Apr-13 | |

| Apr-10 | |

| Apr-09 | |

| Apr-09 | |

| Apr-08 | |

| Apr-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite