|

|

|

|

|||||

|

|

|

Cisco Systems CSCO shares appreciated 34.6% in the trailing 12-month period, benefiting from an aggressive AI push and growing security dominance. Shares outperformed the broader Zacks Computer & Technology sector, as well as close peers Hewlett Packard Enterprise HPE and Arista Networks ANET. While the broader sector and shares of Arista Networks have appreciated 23% and 29.4%, respectively, shares of Hewlett Packard Enterprise dropped 1.3% over the same time frame.

So, is there more room for Cisco stock to rise? Let’s find out.

AI Infrastructure orders from webscale customers hit $2 billion in fiscal 2025, double the management’s original expectation. In the first quarter of fiscal 2026, product orders from service providers and cloud customers jumped 45% year over year, driven by high double-digit order growth in hyperscalers despite tough comparisons. AI infrastructure orders from hyperscalers hit $1.3 billion, and Cisco expects $3 billion in AI infrastructure revenues from hyperscalers in fiscal 2026. The company also sees a growing pipeline of more than $2 billion in orders for its high-performance networking products across sovereign, Neocloud and enterprise customers.

The first-quarter fiscal 2026 results benefited from robust demand for AI infrastructure and campus networking solutions. The company’s networking portfolio, powered by Silicon One, AI-native security solutions and operating systems, is expanding CSCO’s AI footprint. Networking product orders grew in the high teens, which marked the fifth consecutive quarter of double-digit growth driven by hyperscale infrastructure, enterprise routing, campus switching, wireless, industrial IoT and servers. This bodes well for Networking revenues in fiscal 2026.

Increasing AI workloads at the network edge and the emergence of physical AI are benefiting the industrial IoT portfolio. Orders in the first quarter of fiscal 2026 grew more than 25% year over year. Campus networking is benefiting from strong demand for next-gen solutions, including smart switches, secure routers and Wi-Fi 7 wireless products, which CSCO expects to be the start of a multi-year, multibillion-dollar refresh opportunity as 4K and 6K switches support ends.

Rapid acceleration in the capacity requirements of the network due to unprecedented levels of network traffic and an ever-evolving threat landscape bodes well for Cisco’s prospects. In October, Cisco introduced the Cisco 8223, the industry's most optimized routing system for efficiently and securely connecting data centers and powering the next generation of AI workloads. The company also announced the P200 chip, which powers 8223.

The company recently introduced new agentic capabilities in Cisco AI Assistant, RoomOS 26 for Cisco Devices, and purpose-built integrations across Cisco devices and the Webex Suite. These capabilities will help organizations easily manage and work seamlessly with digital agents. Cisco announced enhancements to the Webex Customer Experience portfolio, including a new AI-powered tool for supervisors. Expected to be available in early 2026, the enhancements will unify quality management across the contact center. The company is also expanding the Webex ecosystem in India and the Kingdom of Saudi Arabia.

The AI opportunity further gets a boost from Cisco’s partnership with NVIDIA NVDA. Integration of Cisco Nexus switches with NVIDIA’s Spectrum-X architecture is offering low-latency, high-speed networking for AI clusters, driving enterprise AI orders. The Cisco Secure AI factory with NVIDIA provides a trusted blueprint for building secure AI-ready data centers for enterprises, sovereign cloud providers and newly emerging Neocloud providers.

For fiscal 2026, CSCO expects revenues to be in $60.2-$61 billion range compared with $56.7 billion reported in fiscal 2025. Non-GAAP earnings are expected between $4.08 per share and $4.14 per share compared with $3.81 per share reported in fiscal 2025.

Cisco Systems, Inc. price-consensus-chart | Cisco Systems, Inc. Quote

The Zacks Consensus Estimate for CSCO’s fiscal 2026 revenues is pegged at $60.81 billion, indicating growth of 7.34% on a year-over-year basis. The consensus mark for CSCO’s fiscal 2026 earnings is currently pegged at $4.05 per share, up by a penny over the past 30 days, indicating year-over-year growth of 6.3%.

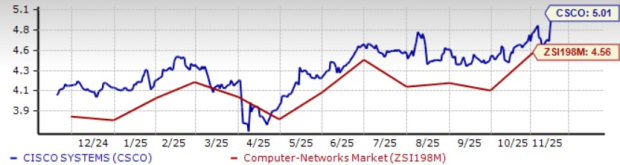

Meanwhile, Cisco shares are overvalued, as suggested by the Value Score of D. In terms of the forward 12-month price/sales, CSCO is trading at a premium of 5.01X, higher than the Zacks Computer Networking industry’s 4.56X and Hewlett Packard Enterprise’s 0.68X.

An expanding portfolio makes Cisco well-positioned for sustained growth in an evolving tech landscape. AI push is noteworthy, along with a growing footprint in the security space. These trends bode well for CSCO’s long-term prospects. However, stiff competition in the networking space and stretched valuation make the stock risky for investors in the near term.

CSCO currently carries a Zacks Rank #3 (Hold), suggesting that it may be wise for investors to wait for a more favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 5 hours | |

| 5 hours | |

| May-12 | |

| May-12 | |

| May-12 | |

| May-12 | |

| May-12 | |

| May-12 | |

| May-11 | |

| May-11 | |

| May-11 | |

| May-11 | |

| May-11 | |

| May-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite